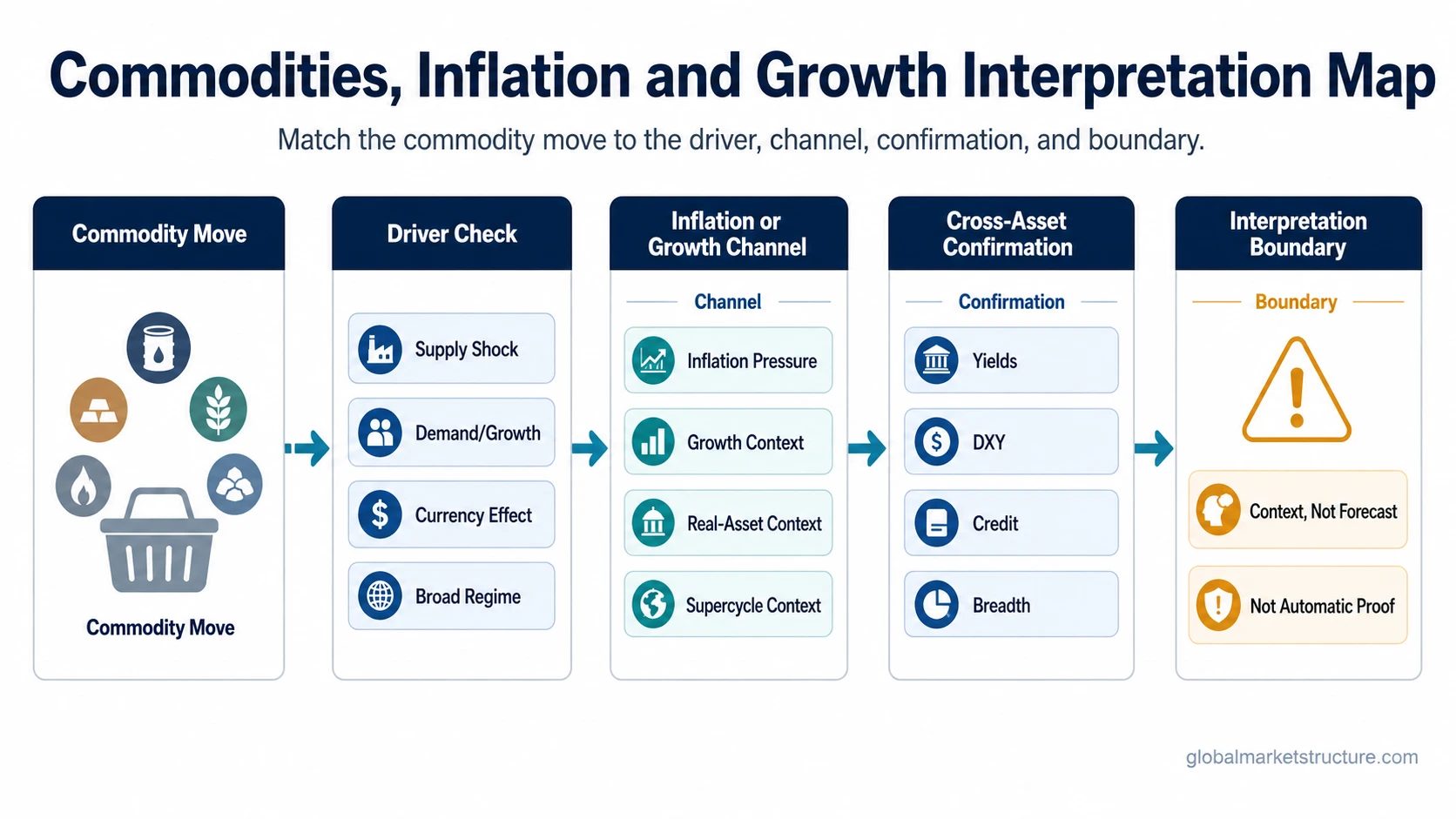

Commodities, inflation, and growth are connected, but a commodity move is not automatically an inflation signal, a growth signal, or a supercycle signal. The useful reading depends on the commodity group, the driver of the move, the inflation channel, the time horizon, and whether related cross-asset evidence confirms the interpretation.

Start by matching the commodity move to the market question. Energy-led stress, broad commodity regimes, copper versus gold behavior, real-asset context, and oil-to-inflation pass-through are related questions, but they do not answer the same market-structure problem.

Current inflation releases, commodity index levels, and official methodology details belong to official data sources. This overview is for choosing the right interpretation path, not for replacing current data.

Which Commodity, Inflation, or Growth Question Are You Trying to Answer?

| Reader question | Best next topic | Why it fits |

|---|---|---|

| Is the move energy-led macro stress? | oil shock | Use this topic for supply disruption, energy price shock, and macro stress framing. |

| Is this part of a long commodity regime? | commodity supercycle | Use this topic for multi-year supply, demand, investment, and real-asset cycle context. |

| Is the question about growth-sensitive intermarket behavior? | copper-gold ratio | Use this topic for copper versus gold as growth-sensitive context, not as a trading signal. |

| Is the question about hard assets in an inflation regime? | real assets | Use this topic for real-asset framing with limitations, not automatic hedge claims. |

| Is the question specifically about oil feeding inflation? | oil prices and inflation | Use this topic for direct oil pass-through context and headline inflation pressure. |

How Commodity Moves Connect to Inflation and Growth

Commodity moves can affect inflation through energy, food, transportation, and input-cost channels. The inflation reading is usually more direct when the move affects widely used inputs, but it still depends on pass-through, duration, currency effects, and whether the price change reaches consumer prices.

Commodity moves can also reflect growth conditions. Demand-sensitive commodities may strengthen when industrial activity improves, while defensive or monetary assets may behave differently when growth expectations weaken or policy stress rises. That does not make any single commodity a complete growth gauge.

Practical scenario: An energy price spike can pressure headline inflation while saying less about broad growth if the move is mainly supply-driven. Copper strength may carry a different message if it appears alongside improving industrial demand, but that reading weakens without confirmation from gold, yields, credit spreads, or equity breadth.

False-Reading Boundary

A commodity move is not enough by itself. Rising commodities do not automatically prove inflation acceleration, stronger growth, a recession shock, a real-asset regime, or a commodity supercycle.

The interpretation weakens when the move is narrow, short-lived, supply-driven, currency-driven, or disconnected from related macro signals. A cleaner reading usually requires matching the commodity group to the driver of the move and checking whether inflation data, growth-sensitive assets, credit conditions, real yields, or market breadth support the same interpretation.

Match the Driver Before Interpreting the Move

The same commodity move can belong to different market-structure questions. Oil-led stress belongs in an oil shock reading. A broad, multi-year supply and investment imbalance belongs in a commodity supercycle reading. Copper versus gold belongs in growth-sensitive intermarket context. Hard-asset behavior belongs in real-asset regime context. Oil pass-through belongs in the oil prices and inflation topic.

The safer sequence is to identify the driver first, then choose the more specific reading. Broad commodity direction alone is not enough to classify inflation pressure, growth strength, real-asset demand, or macro stress.