An oil shock is a disruptive oil-related supply, demand, or price shock that can transmit into inflation, growth, policy expectations, and cross-asset conditions. It is not the same as every oil-price move, and it is not a standalone signal for recession, inflation regime, or market direction.

Oil shock meaning: an oil shock becomes macro-relevant when the oil move is large enough, persistent enough, or disruptive enough to affect energy costs, real income, business margins, inflation expectations, policy expectations, or broader market risk conditions.

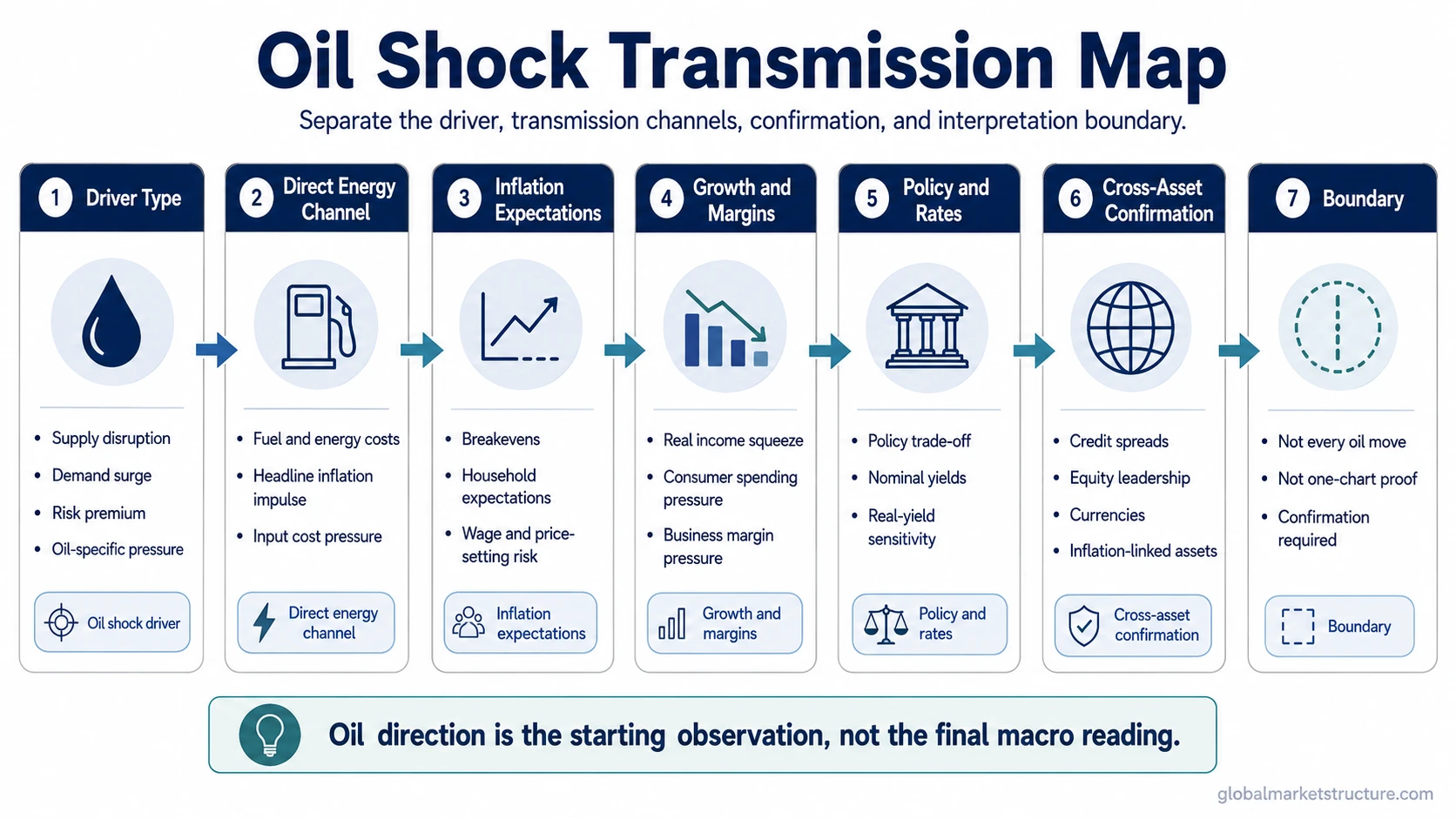

The useful reading starts with the driver. A supply disruption, a demand surge, and a precautionary risk premium can all lift oil prices, but they do not carry the same message for growth, inflation, rates, credit, or risk appetite.

Oil shock vs normal oil-price movement

A normal oil-price movement can reflect routine changes in inventories, seasonal demand, currency effects, positioning, or short-term market noise. An oil shock is different because the move begins to affect the wider economy or the way markets price inflation, growth, and policy risk.

| Concept | Meaning | Macro reading |

|---|---|---|

| Normal oil-price movement | A routine change in crude oil prices caused by supply, demand, inventories, currency effects, or positioning. | Usually needs confirmation before it becomes a macro signal. |

| Oil shock | A disruptive oil-related move that affects energy costs, confidence, inflation expectations, income, margins, policy expectations, or cross-asset risk pricing. | Can matter for inflation and growth, but the interpretation depends on the driver and surrounding conditions. |

The distinction prevents a common mistake: treating every oil rally as an inflation shock or every oil drop as a growth warning. Oil direction is only the first observation. The macro reading depends on what caused the move and whether other markets confirm the same pressure.

Main types of oil shocks

Oil shocks are easier to interpret when they are separated by driver. The same price move can mean different things depending on whether it comes from constrained supply, stronger demand, or uncertainty about future supply.

| Driver type | Typical source | Main macro channel | Interpretation boundary |

|---|---|---|---|

| Supply shock | Production disruption, embargo, conflict, sanctions, transport interruption, or unexpected supply constraint. | Higher input costs, weaker real income, margin pressure, and headline inflation pressure. | May hurt growth even while lifting headline inflation, so it should not be read as simple demand strength. |

| Demand shock | Stronger global activity, faster industrial demand, travel demand, or broad commodity demand. | Growth-sensitive demand, inflation pressure, and possible policy repricing. | Can look inflationary, but may also reflect stronger activity rather than pure supply stress. |

| Precautionary or risk-premium shock | Fear of future supply disruption, geopolitical risk, shipping risk, or inventory hoarding. | Risk pricing, expectations, volatility, and cross-asset uncertainty. | May fade if the expected disruption does not become real or persistent. |

An oil supply shock is usually the most stagflationary version because it can push energy prices higher while reducing purchasing power and raising business costs.

How an oil shock affects inflation and growth

The inflation effect usually begins with direct energy prices. Gasoline, diesel, heating fuel, transport costs, and energy-intensive production can affect headline inflation more quickly than core inflation. The growth effect comes from the opposite side of the same pressure: households and firms may have less real income left for other spending.

| Transmission channel | Inflation effect | Growth effect | What to confirm |

|---|---|---|---|

| Direct energy costs | Raises headline inflation through fuel and utility categories. | Reduces disposable income if wages and revenue do not keep pace. | Energy share, persistence, and whether the shock spreads beyond energy. |

| Input costs | Can raise goods and service prices if firms pass costs through. | Can compress margins if firms cannot pass costs through. | Corporate margins, producer prices, and pricing power. |

| Inflation expectations | Can matter if households, firms, or markets extrapolate higher energy prices. | Can pressure confidence if higher expected inflation reduces real purchasing power. | Breakevens, surveys, wage behavior, and central-bank credibility. |

| Policy reaction | Can raise the perceived need for tighter policy if inflation expectations become unstable. | Can increase slowdown risk if policy tightens into weaker real income. | Real yields, rate expectations, credit conditions, and growth data. |

This is why oil prices and inflation should be interpreted through transmission rather than price direction alone. A short energy spike and a persistent broad pass-through are not the same macro condition.

Oil shock and policy expectations

An oil shock can create a policy trade-off. If energy pressure lifts headline inflation while growth weakens, central banks may face inflation risk and slowdown risk at the same time. Markets then have to judge whether policy makers will focus more on inflation credibility, growth protection, or financial conditions.

Policy interpretation boundary: an oil shock does not automatically mean higher policy rates. The policy reading depends on inflation expectations, the starting inflation regime, growth momentum, labor-market conditions, financial stress, and whether the shock is temporary or persistent.

Rates markets may react differently depending on the mix. Nominal yields can rise if inflation compensation increases. Real yields can behave differently if growth fears dominate. Credit spreads can widen if the shock looks like a margin and demand problem rather than a clean reflation impulse.

How markets confirm or reject an oil shock reading

Oil is only one input. A stronger macro reading usually needs confirmation across inflation-linked assets, rates, currencies, credit, equities, and other commodities. Without that confirmation, the oil move may be an isolated commodity move rather than a broader regime shift.

| Market area | Possible confirmation | False-reading risk |

|---|---|---|

| Inflation markets | Breakevens or inflation-linked assets reflect broader inflation concern. | Energy-only pressure may not translate into persistent inflation expectations. |

| Rates | Nominal yields, real yields, or policy-rate expectations reprice in a consistent direction. | Rates may instead price growth weakness or safe-haven demand. |

| Credit | Credit spreads widen if margin pressure and growth risk become more important. | Calm credit can weaken the case for systemic stress. |

| Equities | Leadership shifts toward energy or defensive areas depending on the driver. | Index moves can be dominated by unrelated earnings, positioning, or valuation effects. |

| Currencies | Oil importers and exporters may diverge if the shock affects terms of trade. | Currency moves can also reflect rates, risk appetite, or dollar liquidity. |

The strongest readings are usually multi-market. A single crude oil chart can show pressure, but it cannot by itself prove an inflation regime, recession outcome, or risk-asset direction.

Common false readings

Oil shocks are often misread because they touch several macro narratives at once. The same move can be described as inflationary, recessionary, geopolitical, or reflationary, but those labels are not interchangeable.

| False reading | Why it is incomplete | Better check |

|---|---|---|

| Higher oil always means stronger inflation regime. | Energy can lift headline inflation without creating durable broad inflation. | Check core pass-through, expectations, wages, and policy credibility. |

| Higher oil always means stronger growth. | A supply shock can raise oil while hurting real income and margins. | Separate demand-driven oil strength from supply-driven cost pressure. |

| Higher oil always means recession. | Recession risk depends on shock size, persistence, policy response, and starting conditions. | Check credit, labor, real income, confidence, and breadth of slowdown. |

| Lower oil always means weak demand. | Lower oil can also come from supply increases, positioning, currency moves, or inventory changes. | Check whether other growth-sensitive markets confirm demand weakness. |

The practical boundary is simple: oil direction starts the question, but it does not finish the interpretation.

Historical oil shocks and why history is not enough

Oil shocks are often discussed through historical episodes because past supply disruptions and energy-price spikes affected inflation, growth, and policy debates. Historical context can help show why oil matters, but it can also create overconfidence if the current driver, starting inflation regime, policy backdrop, and cross-asset confirmation are different.

History use: historical oil shocks are useful for understanding possible channels, not for mechanically predicting the next inflation, recession, or market outcome.

A better approach is to treat history as a channel map. First identify the driver, then check inflation pass-through, real-income pressure, policy expectations, credit stress, currency effects, and broader market confirmation.

Oil shock vs inflation shock

An oil shock can contribute to an inflation shock, but the two ideas are not identical. An oil shock starts from oil-related pressure. An inflation shock can come from wages, fiscal stimulus, supply chains, currency weakness, housing, broad demand, or expectations.

The overlap matters most when energy pressure spreads into broader prices or expectations. If the pressure remains narrow and temporary, the inflation reading is weaker. If it spreads through wages, pricing behavior, and policy expectations, the macro signal becomes broader than oil alone.

Related oil shock concepts

Oil prices and inflation explains the pass-through from energy prices into headline inflation, expectations, and policy interpretation.

Supply shock covers the broader macro category that includes oil-specific supply disruptions.

Inflation shock separates a broad inflation disturbance from an oil-specific shock.

Inflation expectations helps explain why temporary energy pressure can matter more if households, firms, or markets extrapolate it.

Commodity supercycle covers the structural version of commodity pressure rather than a discrete shock.

FAQ

Is every oil-price increase an oil shock?

No. Oil prices can rise for routine market reasons. The move becomes an oil shock when it is large, persistent, disruptive, or important enough to affect inflation, income, margins, confidence, policy expectations, or broader market pricing.

Does an oil shock always cause inflation?

No. An oil shock can lift headline inflation, especially through energy prices, but persistent inflation depends on pass-through, expectations, wages, currency effects, policy credibility, and the duration of the shock.

Does an oil shock always cause a recession?

No. Oil shocks can weaken growth by pressuring real income and business costs, but recession risk depends on the size of the shock, the starting economy, policy response, credit conditions, and broader confirmation.

Why does the driver of an oil shock matter?

The driver determines the macro meaning. A supply disruption can raise costs while hurting growth, a demand shock can reflect stronger activity, and a precautionary shock can reflect uncertainty before actual supply is affected.