Earnings revisions are changes to previously published earnings estimates. They update the market’s expectation baseline for future profits, especially when analysts change EPS, revenue, growth, or margin assumptions across more than one company or sector.

Definition: Earnings revisions are estimate updates, not reported earnings results. They help classify how forward earnings expectations are changing inside the earnings cycle, but they do not confirm market direction, recession timing, or a direct investment signal.

The useful distinction is simple: revisions happen when expectations change; actual earnings happen when companies report results. A revision can occur before, during, or after a reporting period as analysts update models in response to guidance, demand trends, cost pressure, macro conditions, or new company information.

Key Points

- Earnings revisions track changes in estimates, not the final reported numbers.

- Upward revisions raise the expectation baseline, while downward revisions lower it.

- Broad revision patterns are usually more informative than one isolated analyst change.

- Revision breadth, analyst coverage, estimate freshness, and dispersion affect interpretation quality.

- Earnings revisions can help interpret profit-cycle pressure, but they are not timing tools.

What Earnings Revisions Are and Are Not

Earnings revisions are often confused with nearby earnings-cycle concepts. The differences matter because each concept answers a different market question.

| Concept | What it means | What it does not mean |

|---|---|---|

| Earnings revisions | Changes to previous estimates for future earnings, revenue, margins, or growth. | They are not the reported earnings result itself. |

| Actual earnings | The results companies report for a completed period. | They are not the same as prior estimate changes. |

| Earnings surprises | The gap between reported results and the expectations that existed before the report. | They are not simply upward or downward estimate updates. |

| Earnings season | The reporting window when companies release results, guidance, and management commentary. | It is not a revision by itself, although it can trigger estimate resets. |

| Profit margins | The relationship between revenue, costs, and profit after expenses. | They are not revisions, although margin assumptions can drive revisions. |

| Earnings recession | A broad contraction in aggregate earnings over a period. | It is not confirmed by estimate cuts alone. |

How Earnings Revisions Change Expectations

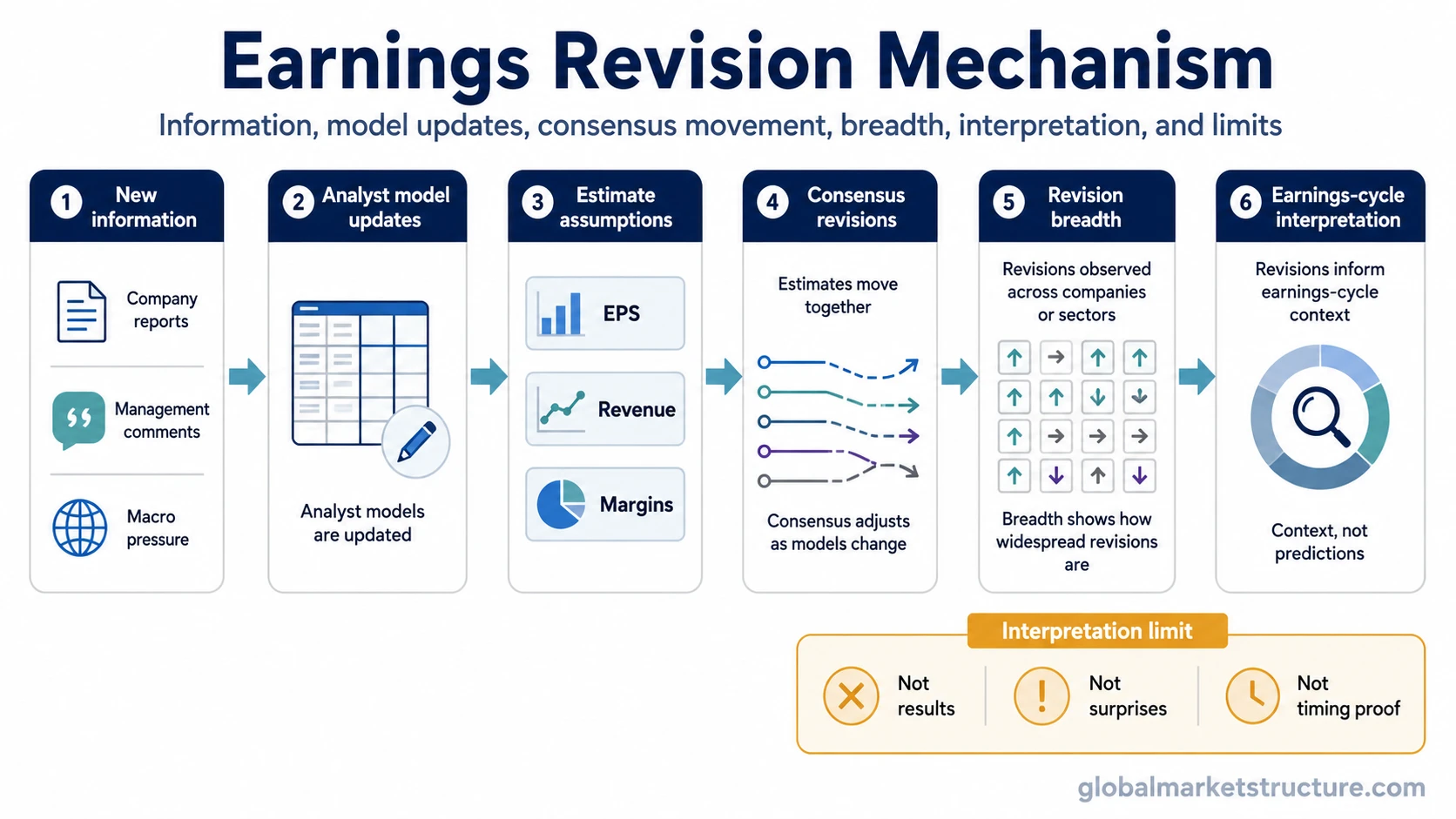

Estimate revisions begin with new information entering analyst models. That information can come from company guidance, reported demand, input-cost pressure, currency effects, financing costs, industry data, or broader macro conditions.

| Stage | What changes | Market-structure interpretation |

|---|---|---|

| New information | Guidance, demand, costs, rates, currency, or sector conditions change. | The earnings baseline may need to be adjusted. |

| Analyst model update | EPS, revenue, margin, or growth assumptions are revised. | The change begins at the estimate level, not at the reported-result level. |

| Consensus movement | Multiple estimates shift enough to move the aggregate expectation. | The revision becomes more useful when it reflects more than one isolated update. |

| Revision breadth | More companies, sectors, or analyst models move in the same direction. | Broader revisions can point to wider earnings-cycle pressure or improvement. |

| Interpretation limit | Prices may have already adjusted, or liquidity and positioning may dominate near-term reactions. | The revision helps frame expectations, not guarantee timing or direction. |

For market interpretation, the key question is not whether one estimate changed. The stronger question is whether the aggregate expectation baseline is moving in a broad, fresh, and consistent way.

Upward and Downward Earnings Revisions

An upward earnings revision means an estimate has been raised from an earlier forecast. A downward earnings revision means an estimate has been reduced from an earlier forecast.

Upward revisions can indicate improving expectations for future earnings, stronger revenue assumptions, better margin assumptions, or less pressure than analysts previously expected. Downward revisions can indicate weaker forward earnings expectations, demand pressure, cost pressure, margin risk, or lower confidence in the previous estimate base.

Limitation: Direction alone is not enough. A small upward revision from one analyst is different from a broad upward shift across many estimates. A large downward revision after a major price adjustment may also carry a different interpretation from early estimate cuts that have not yet been absorbed by markets.

Revision Breadth and Consensus Quality

Revision breadth describes how widely estimate changes are spreading. A narrow revision affects one company, one analyst model, or one small set of assumptions. A broader revision pattern affects many companies, multiple sectors, or a larger share of the analyst base.

Breadth is not the same as magnitude. A few large cuts may change the headline number, while many smaller cuts may show that earnings pressure is spreading. Both details matter, but they answer different questions.

Consensus quality also matters. A consensus estimate is more useful when analyst coverage is fresh, the analyst count is meaningful, and dispersion is not extreme. If many estimates are stale or analysts disagree widely, the headline consensus can hide uncertainty rather than clarify it.

Better revision context: broad participation, fresh estimates, consistent direction, visible magnitude, and a clear reason for the change.

Weaker revision context: one isolated analyst update, narrow coverage, stale estimates, high dispersion, or revisions that follow information already priced into markets.

Revisions, Profit Margins, and Earnings Season

Earnings revisions often connect to margin assumptions. If revenue expectations hold steady but cost assumptions rise, analysts may cut EPS because profit margins are expected to narrow. If pricing power improves or input-cost pressure eases, margin assumptions may support upward revisions.

Reporting periods can also reset expectations. During earnings season, reported results, guidance, and management commentary can force analysts to update forward models. The revision is the estimate change that follows the new information, not the reporting window itself.

This distinction keeps the earnings-cycle view clean: margins describe profitability pressure, earnings season delivers new information, and revisions show how forward expectations adjust.

Earnings Revisions Scenario

Several analysts begin reducing forward EPS assumptions while margin assumptions weaken across multiple sectors. The immediate read is not that an earnings recession has already started. The cleaner conclusion is that forward profit expectations are deteriorating.

The case becomes more meaningful if the cuts are broad, recent, and linked to visible pressure such as weaker demand, rising costs, or lower guidance. It remains incomplete if the cuts are narrow, stale, already reflected in prices, or contradicted by stronger reported results and resilient margins.

The practical value is diagnostic. Earnings revisions help organize the direction and quality of expectation changes, but broader market interpretation still needs context from reported earnings, margins, valuation, liquidity, rates, positioning, and risk appetite.

Where Earnings Revisions Can Mislead

Earnings revisions become less reliable when they are treated as direct market signals. Markets may move before the revision appears, ignore a revision that was already expected, or react differently because liquidity, valuation, positioning, or macro regime has changed the risk environment.

| Risk | Why it matters | Safer interpretation |

|---|---|---|

| Lag | Analyst estimates may adjust after the market has already repriced new information. | Treat revisions as expectation updates, not early proof of direction. |

| Herding | Analysts may cluster around consensus, especially when uncertainty is high. | Check dispersion, magnitude, and whether estimates are fresh. |

| Stale estimates | Old estimates can make consensus look more stable than it really is. | Freshness matters as much as the headline revision direction. |

| Narrow coverage | One analyst change can look important when coverage is thin. | Separate isolated updates from broad revision breadth. |

| Already-priced expectations | Markets can discount likely revisions before they appear in consensus data. | Compare revisions with prior price behavior, valuation, and risk appetite. |

| Regime override | Liquidity, rates, credit stress, or risk appetite can dominate near-term reactions. | Use revisions as one earnings-cycle input within a broader regime view. |

Related Earnings-Cycle Concepts

Earnings revisions sit between expectations and results. They are most useful when they are compared with nearby concepts rather than read in isolation.

- Earnings results: the actual reported numbers for a completed period.

- Earnings surprises: the gap between reported results and prior expectations.

- Margin pressure: the profitability channel that can push analysts to revise EPS assumptions.

- Revision breadth: the spread of estimate changes across analysts, companies, or sectors.

- Earnings recession: a broader aggregate profit contraction, not something confirmed by estimate cuts alone.

FAQ

What are earnings revisions?

Earnings revisions are changes to previous earnings estimates. They usually reflect updated assumptions about EPS, revenue, margins, growth, or company guidance.

Are earnings revisions the same as earnings surprises?

No. Earnings revisions change estimates before or around a reporting period. Earnings surprises compare reported results with the expectations that existed before the report.

Do downward earnings revisions prove that a recession is coming?

No. Downward revisions can indicate weaker forward earnings expectations, but they do not by themselves confirm an earnings recession, market direction, or timing.

Why does revision breadth matter?

Revision breadth helps separate isolated analyst changes from broader expectation shifts. A wider pattern is usually more informative than a single estimate update.