Monetary transmission mechanism is the process through which monetary policy decisions pass through financial conditions, credit, expectations, spending, demand, output, inflation pressure, exchange rates, asset prices, and balance-sheet conditions over time, with lags and uncertainty.

Core role: the mechanism connects a policy decision to the channels that may change financing costs, risk appetite, borrowing behavior, income expectations, and inflation pressure.

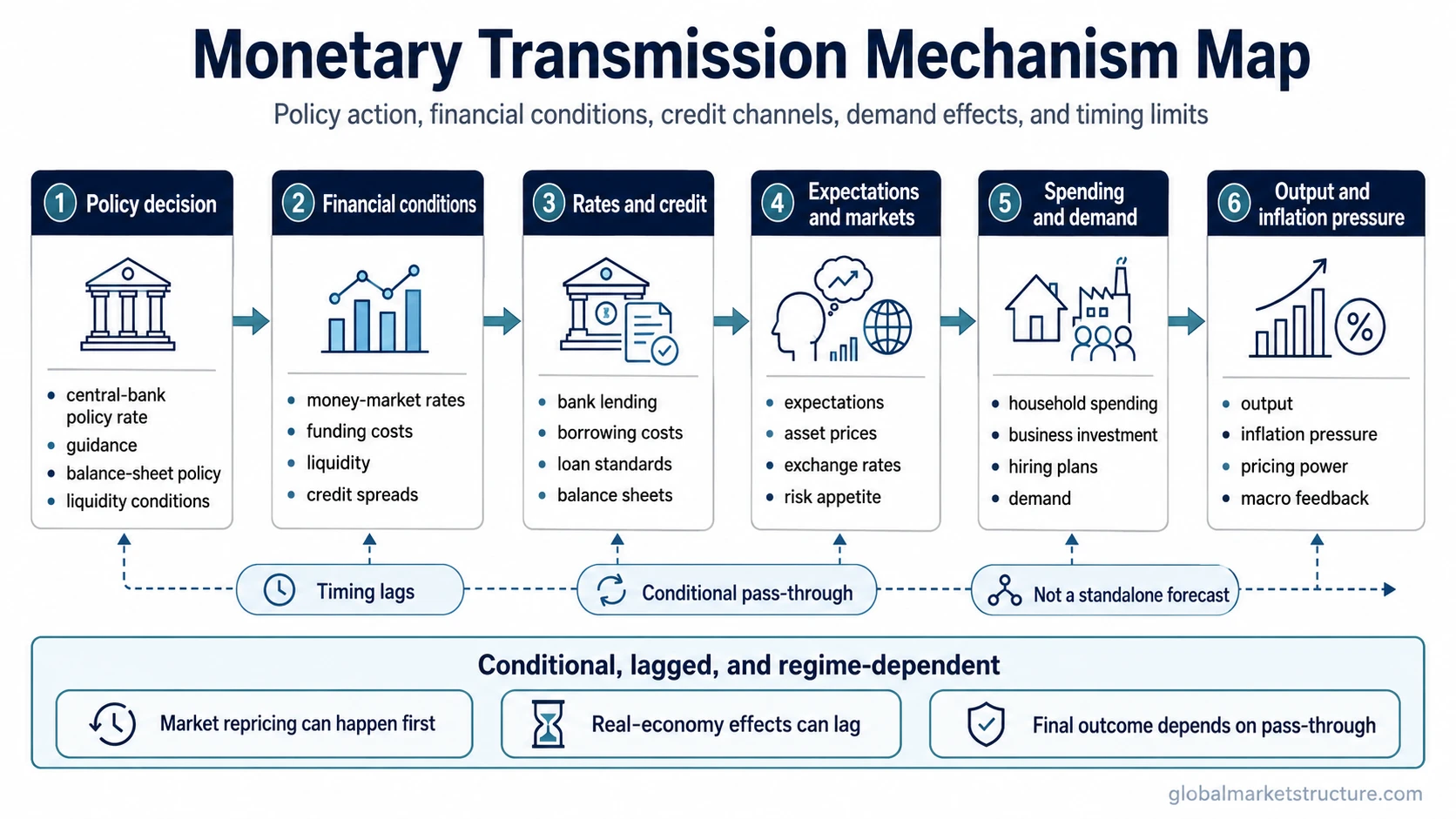

Main limitation: it is a conditional macro mechanism, not a standalone forecast for recession, yields, equities, currencies, credit spreads, or risk assets.

Markets may react quickly to a policy decision because investors discount expected future effects. The real economy usually responds more slowly because borrowing, lending, wages, investment, household spending, and pricing decisions adjust with lags.

What Is the Monetary Transmission Mechanism?

The monetary transmission mechanism describes how central-bank policy can pass into the economy and financial markets. A change in policy rates, balance-sheet policy, forward guidance, or liquidity conditions can influence money-market rates, bank funding costs, credit supply, asset prices, exchange rates, expectations, aggregate demand, and inflation pressure.

The useful point is sequence. Policy action comes first, but the final outcome depends on whether households, firms, banks, investors, and global capital flows actually transmit that policy impulse into spending, financing, risk-taking, and price-setting behavior.

Simple sequence: policy decision → financial conditions → credit and expectations → spending and investment → demand and output → inflation pressure.

That sequence can strengthen, weaken, or break at different points. Bank lending may stay cautious after rates fall. Households may keep spending even after rates rise. Asset prices may reprice before economic data confirms the change. The mechanism is therefore best read as a conditional transmission map.

Monetary Policy vs Monetary Transmission Mechanism

Monetary policy is the decision or tool used by a central bank. The monetary transmission mechanism is the path through which that decision may affect financial conditions, credit, expectations, demand, and inflation pressure.

A rate hike, rate cut, forward-guidance shift, or balance-sheet operation is not the same as its final economic effect. The policy action changes incentives and constraints. Transmission depends on pass-through.

| Concept | Main question | Boundary |

|---|---|---|

| Monetary policy | What did the central bank decide or signal? | Decision, tool, stance, or communication. |

| Monetary transmission mechanism | How can that decision move through markets and the economy? | Transmission path across rates, credit, expectations, assets, demand, and inflation pressure. |

| Policy lag | How long can the effect take to appear? | Timing problem, not the full mechanism. |

| Fiscal policy | How do spending, taxation, transfers, and borrowing affect demand? | A separate policy channel from government budgets, not central-bank transmission. |

Fiscal policy can interact with monetary transmission, but it works through government spending, taxation, transfers, borrowing, and fiscal stance rather than central-bank policy tools.

Main Monetary Transmission Channels

The mechanism usually works through several channels at the same time. No single channel is always dominant, and the same policy action can transmit differently across cycles, banking systems, inflation regimes, and global liquidity conditions.

| Channel | What changes first | How it can transmit | Main limitation |

|---|---|---|---|

| Policy-rate / money-market rate channel | Short-term rates and funding benchmarks | Borrowing costs, discount rates, savings incentives, and financing choices may adjust. | Pass-through can be slow if contracts, banks, or borrowers do not reprice quickly. |

| Bank lending and credit channel | Loan pricing, lending standards, and credit availability | Firms and households may change borrowing, investment, hiring, and spending plans. | Banks may tighten or loosen credit for reasons beyond the policy rate alone. |

| Expectations channel | Expected inflation, growth, and future policy path | Households, firms, and investors may adjust decisions before realized data changes. | Credibility matters; guidance can fail if markets doubt the policy path. |

| Asset-price channel | Bond yields, equity valuations, credit spreads, and risk appetite | Wealth effects, financing conditions, and portfolio allocation can shift. | Asset prices can move on expectations without confirming final macro outcomes. |

| Exchange-rate channel | Currency pricing and cross-border capital flows | Import prices, export competitiveness, and external financial conditions may change. | Currency response depends on relative policy, growth, risk appetite, and global funding pressure. |

| Balance-sheet / collateral channel | Asset values, collateral quality, leverage capacity, and net worth | Stronger or weaker balance sheets can affect borrowing capacity and risk tolerance. | Balance-sheet strength can cushion transmission or amplify stress. |

| Aggregate-demand and inflation-pressure channel | Spending, investment, output gaps, and pricing behavior | Demand conditions may eventually influence employment, output, and inflation pressure. | Inflation and output respond with uncertainty and can be offset by supply shocks or fiscal support. |

How Markets Can Price Transmission Before the Economy Changes

Financial markets often respond before households, firms, and banks complete the real-economy adjustment. Bond yields, equity valuations, credit spreads, exchange rates, and liquidity-sensitive assets can move when investors revise expectations about the future policy path.

That early repricing is not the same as completed transmission. A drop in equity valuations may reflect a higher discount-rate assumption, not an already-realized collapse in demand. A stronger currency may reflect relative policy expectations, not a finished inflation outcome. A credit-spread move may reflect tighter risk pricing, not a confirmed recession.

Interpretation boundary: market repricing can reveal expected transmission, but it does not prove that the full macro effect has already occurred.

This distinction matters for Global market-structure analysis because policy transmission can appear first in financial conditions, then later in credit behavior, spending, output, and inflation pressure.

Why Transmission Is Conditional

Monetary transmission depends on the starting point. A highly leveraged economy may react differently from an economy with strong household balance sheets. A banking system under stress may restrict credit even after rates fall. A strong fiscal backdrop can offset part of monetary tightening. Global capital flows can change exchange-rate transmission.

A separate fiscal impulse can also change the interpretation. Monetary policy may be trying to cool demand while fiscal support keeps income and spending resilient, or monetary easing may have a weaker effect if fiscal policy is withdrawing support at the same time.

Inflation structure also matters. Demand-driven inflation may respond differently from supply-shock inflation, import-price pressure, wage pressure, or energy-driven inflation. The mechanism is strongest when the policy impulse reaches the channels that actually control the pressure being targeted.

Common False Reading

False reading: a rate hike automatically predicts recession, lower equities, stronger currency, wider credit spreads, or durable disinflation.

Better reading: a policy change can alter financial conditions and incentives, but the final outcome depends on pass-through, timing, credibility, credit behavior, balance sheets, fiscal offset, and global liquidity.

The same policy move can transmit differently in different regimes. A tightening cycle may weigh on demand if credit is sensitive and balance sheets are stretched. It may transmit more slowly if consumers and firms have locked in low financing costs, fiscal support remains strong, or inflation expectations require a longer adjustment.

How Monetary Transmission Fits Market Structure

For market-structure interpretation, monetary transmission connects central-bank policy to the wider regime. It helps explain why rates, yield curves, credit spreads, currencies, equity valuation, liquidity-sensitive assets, and risk appetite may change together or diverge.

Transmission is most useful when it is compared with financial conditions, credit behavior, real yields, inflation expectations, earnings sensitivity, and cross-asset confirmation. A policy change alone is not enough. The stronger signal comes from whether multiple channels begin confirming the same direction of pressure.

| Market area | Transmission question | Useful caution |

|---|---|---|

| Rates | Are money-market rates, bond yields, and real yields reflecting the policy path? | Yields also reflect growth expectations, inflation risk, term premium, and safe-haven demand. |

| Credit | Are borrowing costs, spreads, and lending standards changing? | Credit can tighten from risk aversion even without a new policy shock. |

| Equities | Are valuations, margins, earnings expectations, or risk appetite adjusting? | Equity moves can reflect discount rates, growth expectations, liquidity, or positioning. |

| FX | Are relative policy expectations and capital flows moving the currency? | Exchange rates depend on relative growth, risk appetite, funding pressure, and external balances. |

| Inflation pressure | Is demand cooling or strengthening enough to affect pricing behavior? | Inflation can remain sticky if supply, wages, rents, or expectations offset weaker demand. |

The clean boundary is that monetary transmission mechanism explains the pass-through path. It should not replace separate analysis of policy stance, fiscal support, financial conditions, real yields, credit risk, or the broader market regime.

FAQ

What is the monetary transmission mechanism?

Monetary transmission mechanism is the process through which monetary policy decisions move through financial conditions, credit, expectations, demand, output, inflation pressure, exchange rates, asset prices, and balance-sheet conditions over time.

What are the main channels of monetary transmission?

The main channels include policy-rate and money-market rates, bank lending and credit, expectations, asset prices, exchange rates, balance sheets, aggregate demand, and inflation pressure.

How is monetary transmission different from monetary policy?

Monetary policy is the central-bank decision or tool. Monetary transmission is the path through which that decision may affect financing costs, credit behavior, expectations, demand, inflation pressure, and markets.

Why does monetary transmission work with lags?

Transmission works with lags because contracts, lending decisions, refinancing schedules, household behavior, business investment, wage setting, and price setting do not all adjust at the same speed.

Does the monetary transmission mechanism predict asset prices?

No. It can help explain why markets may reprice after policy changes, but it does not mechanically predict equities, bonds, currencies, credit spreads, commodities, or risk assets.