Policy lag is the delay between an economic change, the recognition of that change, a policy decision, implementation, and the later effect on credit, demand, prices, employment, or output. The lag matters because policy and markets do not move on one timeline. Expectations and financial conditions can adjust before the real economy confirms the effect. Policy lag is a timing limitation, not a fixed market forecast.

What policy lag means

A policy lag is the time gap between a policy problem and the measurable effect of the response. The problem may be rising inflation, weakening demand, tightening credit, unemployment pressure, or another macro condition. Policymakers first need to recognize the condition, decide what to do, put the decision into effect, and wait for the response to move through households, firms, lenders, investors, and official data.

The point is not that policy works after a known number of months. Instead, each stage of the policy process has its own timing. Recognition can be late, implementation can be slow, and economic effects can arrive unevenly across credit, spending, prices, employment, and output.

Main types of policy lag

Policy lag is usually easier to understand when the delay is separated into stages. Different sources use slightly different labels, but the core idea is the same: a policy response is not instant from diagnosis to economic effect.

| Lag type | What is delayed | Why it matters | Market-structure boundary |

|---|---|---|---|

| Recognition lag | The time needed to identify that an economic condition has changed. | Data can arrive late, be revised, or send mixed signals. | Markets may react to expected conditions before official data fully confirms them. |

| Decision / implementation lag | The time between recognizing the issue, choosing a response, and putting it into effect. | Fiscal decisions can require political approval, while central-bank actions follow meeting cycles and policy frameworks. | The announced stance can move expectations before the full policy effect appears. |

| Impact / response lag | The time between policy implementation and the later effect on credit, spending, prices, employment, or output. | Households, firms, lenders, and investors adjust at different speeds. | Financial conditions can move earlier than real-economy confirmation. |

| Inside lag | The delay before a policy action is taken. | It includes recognition, debate, decision, and administrative steps. | Inside lag helps separate policy discussion from actual policy delivery. |

| Outside lag | The delay after policy is implemented but before it affects the economy. | Transmission through borrowing, income, confidence, and spending takes time. | Outside lag helps separate policy action from later macro results. |

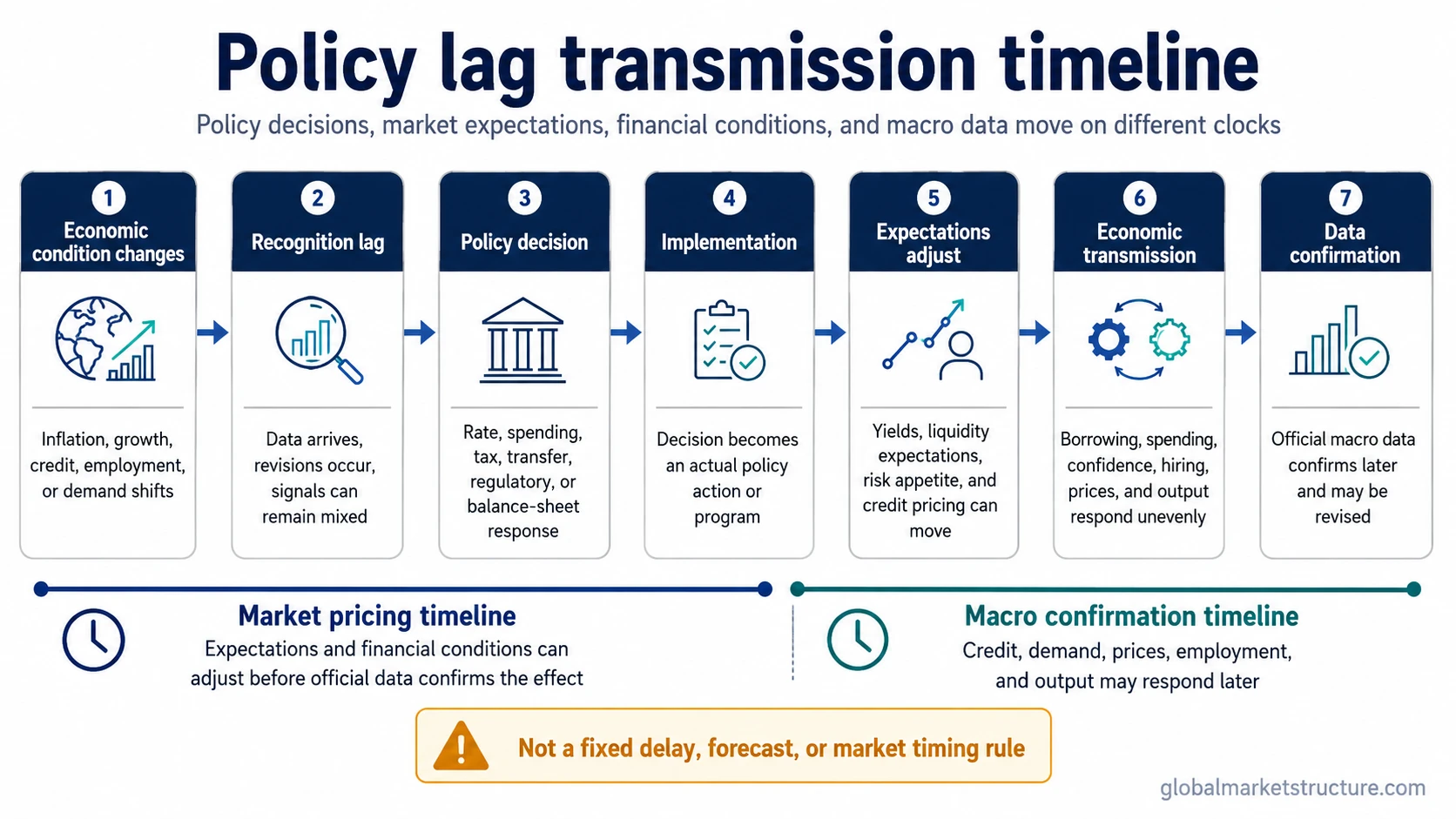

How policy lag moves through the policy sequence

Policy lag is not one single pause. It is a sequence of delays across the policy process and the economy.

- Economic condition changes. Inflation, growth, employment, credit, or demand begins to shift.

- Policymakers identify the issue. The change must be observed, interpreted, and separated from noise.

- A policy decision is made. The response may involve interest rates, spending, taxes, transfers, regulation, or balance-sheet tools.

- Policy is implemented. The decision becomes an actual policy action or program.

- Expectations and financial conditions adjust. Yields, credit conditions, risk appetite, and liquidity expectations may shift before the real economy responds.

- Credit, demand, prices, output, or employment respond over time. The policy effect moves unevenly through households, firms, and markets.

- Official macro data confirms later. The measured effect may appear only after reporting delays and revisions.

This sequence is why policy lag is central to monetary policy and fiscal decisions. The announcement, the implementation, the financial-condition response, and the macro outcome can all happen on different clocks.

Why policy lag matters for market interpretation

Policy lag helps separate policy action from policy transmission. A rate change, spending bill, tax change, or transfer program is not the same thing as the later effect on inflation, growth, credit creation, or employment. The policy action may be visible immediately, while the economic effect may remain uncertain for months or longer.

For market interpretation, the important boundary is between four different layers: the policy action, the policy stance, market expectations, and later macro confirmation. A central bank can change its rate stance, but the broader monetary transmission mechanism still depends on how borrowing costs, credit supply, asset prices, confidence, and spending respond.

This is also why markets can appear to move before the policy effect is visible in official data. Investors may reprice expected policy, expected liquidity, or expected growth before the later economic response is measured. That does not remove policy lag. It shows that market pricing and macro transmission are related but not identical timelines.

Common false reading

False reading: policy lag means markets react after a predictable delay.

Better reading: policy lag means the policy process and economic transmission work through staged and uncertain timing. Markets can price expected policy before the later macro effect is visible, and official data can confirm conditions after financial markets have already adjusted.

Safety boundary: policy lag is not a buy signal, sell signal, forecast, or timing rule. It is a way to avoid confusing policy action with immediate economic impact.

Illustrative scenario

Imagine inflation pressure has started to weaken, but official data still looks mixed. Policymakers may wait for confirmation before changing their stance. Financial markets may begin pricing a softer future policy path before the policy action happens, while households and firms may not feel easier credit conditions until later. The policy lag is the staged delay across recognition, action, expectations, financial conditions, and real-economy effects.

The same logic can work in the opposite direction. If policymakers are expected to tighten, yields and risk appetite may adjust before borrowing, spending, hiring, or output data fully reflect the tighter stance. The scenario remains only illustrative because actual timing depends on the policy tool, the macro environment, the credit system, and expectations.

Policy lag in fiscal and monetary context

Policy lag can appear in both fiscal and monetary policy, but the source of delay can differ. A fiscal program may be slowed by budget approval, administrative rollout, and the timing of payments or tax changes. A change in fiscal impulse may then affect income, demand, and growth pressure with its own delay.

Monetary policy can have a clearer formal decision point once a central bank acts, but its transmission through borrowing costs, credit appetite, asset prices, exchange rates, confidence, and spending can still be long and variable. The broader policy mix matters because fiscal and monetary actions can reinforce, offset, or complicate each other over different time horizons.

What policy lag does not tell you

Policy lag does not reveal the exact date when inflation, growth, employment, credit, or asset prices will respond. It does not prove that a policy action will work, and it does not show whether markets have already priced the expected outcome. It only warns that policy recognition, implementation, financial-condition adjustment, and macro confirmation can be separated by meaningful time gaps.

Related concepts

Policy lag connects most directly to policy mix, fiscal impulse, monetary policy, and the monetary transmission mechanism. These related concepts help separate the policy tool, the policy stance, the transmission channel, and the later macro effect without turning the timing delay into a market forecast.