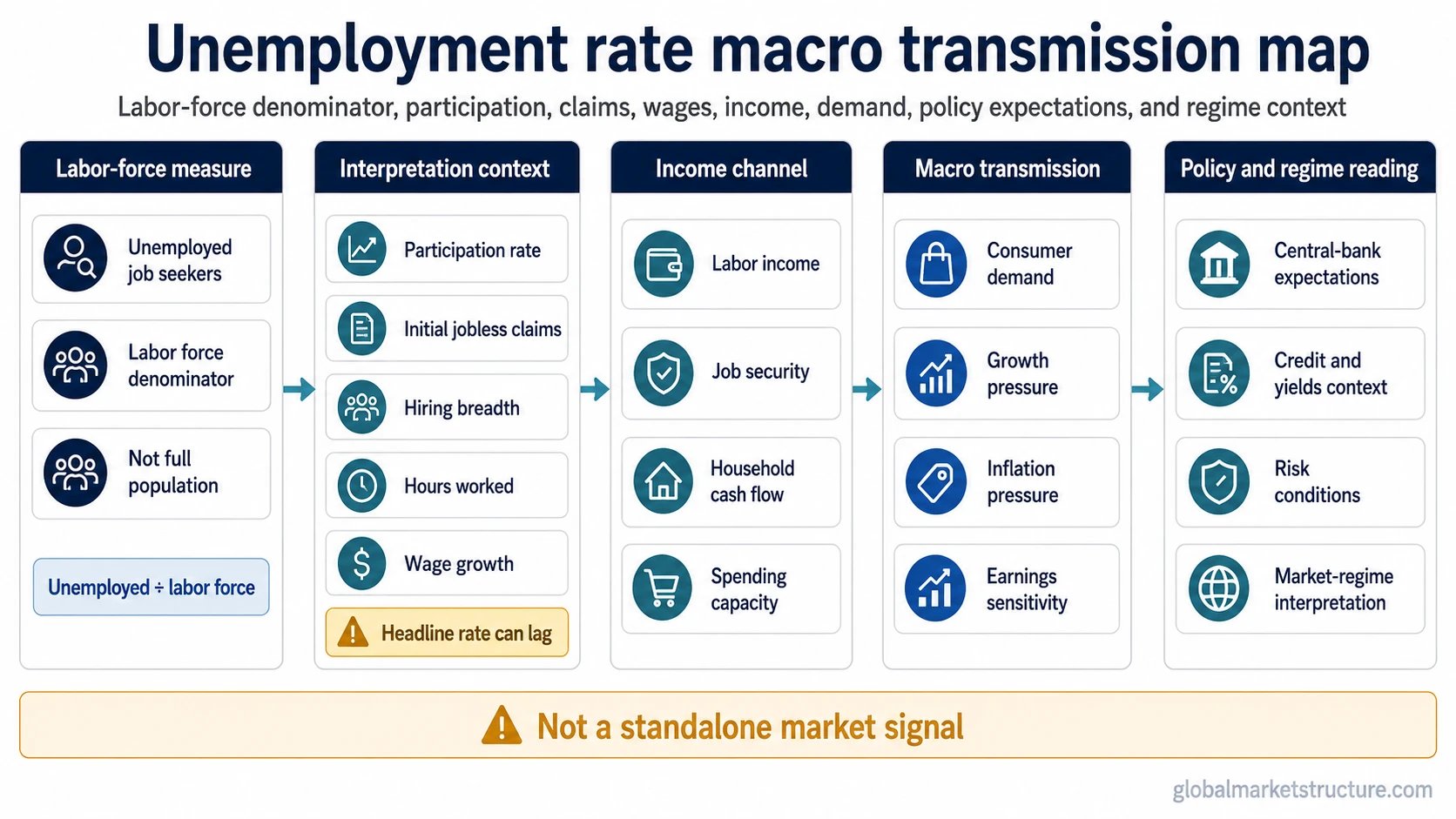

The unemployment rate measures the share of the labor force that is unemployed and actively looking for work. It is not the share of the entire population without a job. Because the denominator is the labor force, changes in participation, job-search behavior, hours worked, wages, and claims can change how the headline rate should be interpreted.

Key points

- The unemployment rate compares unemployed job seekers with the labor force, not with the full population.

- A lower rate can reflect stronger employment conditions, but it can also be affected by people leaving the labor force.

- A stable headline rate can hide weaker hours, slower hiring, rising claims, or falling participation.

- The indicator helps frame labor slack, income pressure, demand, inflation pressure, and policy expectations.

- It is a macro context indicator, not a standalone market signal or forecast tool.

What the unemployment rate measures

The unemployment rate measures joblessness among people who are part of the labor force. In plain terms, it asks how many people who are working or actively seeking work are currently unemployed.

That labor-force framing matters. Someone who does not have a job but is not counted as actively looking for work is not treated the same way as an unemployed job seeker in the headline unemployment rate. This is why the rate is useful, but also why it can be misread if participation and job-search behavior are ignored.

For macro interpretation, the unemployment rate is mainly a labor-slack measure. It helps show whether employment conditions are tight or loose, whether household income pressure may be building, and whether the labor market is reinforcing or weakening the broader demand cycle.

How the unemployment rate is calculated

The basic calculation compares unemployed people with the total labor force.

| Part of the calculation | Meaning | Why it matters |

|---|---|---|

| Unemployed people | People without a job who are counted as actively looking for work. | This is the numerator of the headline unemployment rate. |

| Labor force | People who are employed plus people who are unemployed and actively seeking work. | This is the denominator, so participation changes can affect the rate. |

| Unemployment rate | Unemployed people divided by the labor force. | The result is a percentage that summarizes joblessness within the active labor force. |

The rate is therefore not a complete count of everyone without a job. It is a labor-force measure, which makes it more precise than a broad population statement but less complete than a full labor-market health dashboard.

What the unemployment rate shows

The unemployment rate can show how much labor slack exists in the economy. When the rate is low, employers may face tighter labor supply, wage pressure may become more relevant, and household income conditions may be firmer. When the rate rises, labor income can weaken, job security can deteriorate, and consumer demand may become more vulnerable.

The rate is also useful because it sits close to the income side of the macro cycle. Jobs support wages. Wages support household spending. Household spending feeds demand. Demand conditions influence growth, inflation pressure, earnings sensitivity, and the way markets interpret policy expectations.

The unemployment rate is usually interpreted alongside other labor indicators rather than alone. The surrounding context decides whether the rate is confirming a healthy labor market, lagging behind a turning point, or masking weakness beneath the headline.

What the unemployment rate does not show

The unemployment rate does not show every form of labor-market weakness. It does not fully capture people who have stopped looking for work, workers who want more hours, shifts in labor-force participation, changes in wage quality, or the difference between full-time and part-time employment pressure.

Main limitation: the unemployment rate can look stable even when labor conditions are weakening under the surface. If participation falls, hours worked decline, job openings soften, or initial claims rise, the headline rate may not fully reflect the change in labor momentum.

This is why the unemployment rate should not be treated as a complete labor-market dashboard. It is one important measure inside a broader labor, income, and demand sequence.

Why participation changes the interpretation

Participation is one of the most important reasons the unemployment rate can be misunderstood. If people leave the labor force, the unemployment rate can fall or remain stable even though the underlying employment picture is not necessarily improving.

A stronger labor-market reading usually comes from a combination of low unemployment, healthy participation, solid hiring, stable hours, and wage growth that supports income without creating excessive inflation pressure. A weaker reading can appear when the unemployment rate looks calm while participation, hiring breadth, hours worked, or claims move in the wrong direction.

Illustrative scenario: unemployment stays steady for several months, but labor-force participation edges lower, weekly claims rise, and average hours soften. The headline rate alone may suggest stability, while the surrounding indicators suggest that labor demand is cooling before the unemployment rate fully reflects it.

Unemployment rate vs initial jobless claims

The unemployment rate and initial jobless claims both relate to labor-market stress, but they measure different things. The unemployment rate is a broader labor-force stock measure. Initial jobless claims are a weekly labor-flow indicator that tracks new filings for unemployment insurance.

| Indicator | What it measures | Typical interpretation role |

|---|---|---|

| Unemployment rate | The share of the labor force that is unemployed and actively seeking work. | Broad labor slack and employment stress inside the labor force. |

| Initial jobless claims | New weekly filings for unemployment insurance. | Timelier signal of layoffs or labor-flow deterioration. |

| Labor force participation rate | The share of the population that is working or actively looking for work. | Denominator context for interpreting unemployment changes. |

A common mistake is treating claims and the unemployment rate as interchangeable. Claims may turn before the unemployment rate changes meaningfully, while the unemployment rate may give a broader but slower view of labor slack.

How unemployment connects to macro conditions

The unemployment rate matters for macro analysis because labor conditions transmit into household income, spending capacity, demand, inflation pressure, and policy expectations.

- Unemployment rate: shows labor slack inside the active labor force.

- Labor income: employment conditions influence wages, hours, and household cash flow.

- Household demand: income and job security affect spending capacity and confidence in future spending.

- Inflation and growth pressure: strong labor markets can support demand, while weaker labor markets can reduce growth pressure.

- Policy expectations: labor weakness or tightness can affect how markets interpret central-bank reaction functions.

- Market-regime context: unemployment is read with wages, claims, participation, credit, yields, and broader risk conditions.

The unemployment rate does not determine a market regime by itself. It becomes more useful when it confirms or conflicts with other indicators such as wage growth, initial jobless claims, labor-force participation, credit spreads, yields, and consumer spending.

Common mistake: treating unemployment as a market signal

The unemployment rate can influence market expectations, but it should not be read as a direct buy or sell signal. A low unemployment rate can reflect strong income and demand, but it can also support tighter policy expectations if inflation pressure is still a concern. A rising unemployment rate can signal economic cooling, but it can also shift expectations toward easier policy if inflation is falling.

Safer interpretation: read unemployment as part of a macro sequence, not as a standalone market call. The signal becomes stronger when it aligns with participation, claims, wages, income, consumer demand, inflation data, credit conditions, and policy expectations.

Related indicators to read with unemployment

The unemployment rate is strongest when it is interpreted with indicators that show labor flow, wage pressure, participation, and demand transmission.

| Related indicator | What it adds | Why it changes the unemployment reading |

|---|---|---|

| Labor market | Broader employment, hiring, income, and labor-demand context. | Prevents the unemployment rate from being treated as the whole labor picture. |

| Wage growth | Income pressure and compensation trend. | Shows whether low unemployment is translating into wage pressure or household income support. |

| Initial jobless claims | Timely weekly labor-flow stress. | Can show layoffs or labor deterioration before the unemployment rate fully moves. |

| Labor force participation rate | Labor-force denominator context. | Helps identify whether unemployment changes reflect jobs improvement or participation shifts. |

Current-data note: current unemployment readings and historical time series should be checked through official data endpoints. The unemployment rate still needs interpretation around participation, claims, wages, income, and demand before it is used as macro context.

FAQ

What is the unemployment rate?

The unemployment rate is the percentage of the labor force that is unemployed and actively looking for work. It is not the percentage of the entire population without a job.

Why can the unemployment rate be misleading?

It can be misleading when participation changes, people stop looking for work, hours weaken, underemployment rises, or jobless claims move before the headline unemployment rate changes.

Is a low unemployment rate always good for markets?

No. A low unemployment rate can support income and demand, but it can also affect inflation pressure and policy expectations. Market interpretation depends on the wider macro context.

How is unemployment different from initial jobless claims?

The unemployment rate is a broader labor-force measure, while initial jobless claims track new weekly unemployment insurance filings. Claims are usually more timely, while the unemployment rate gives a broader but slower labor-slack reading.

Does the unemployment rate predict recessions?

The unemployment rate can help identify labor-market deterioration, but it should not be used as a standalone recession predictor. It is usually read with participation, claims, wages, spending, credit, inflation, and policy expectations.