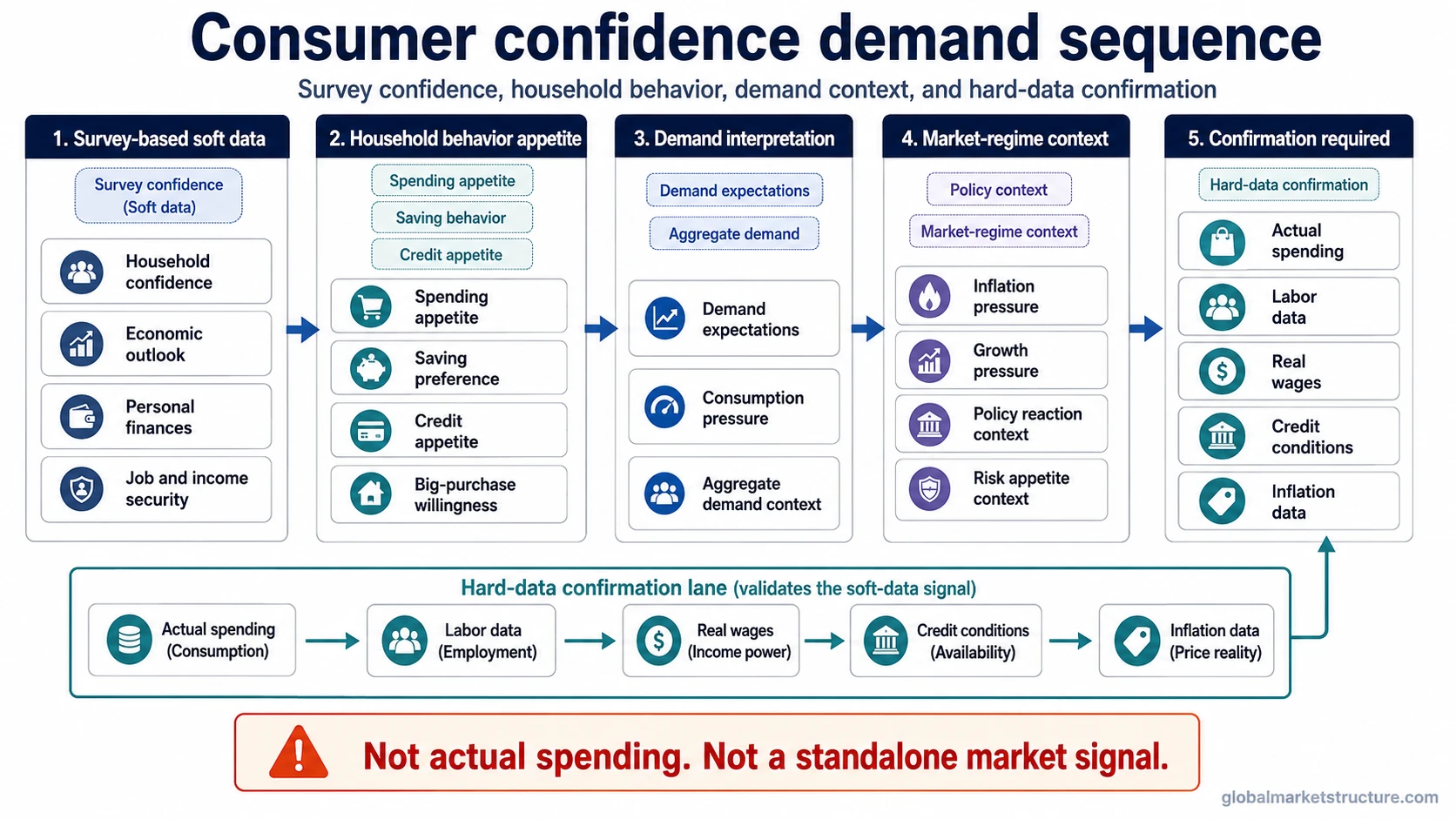

Consumer confidence is a survey-based soft indicator of how households view economic conditions, personal finances, and the outlook ahead. In market-structure analysis, it can help frame spending appetite and demand expectations, but it is not actual consumer spending and should not be treated as a standalone market signal. Its meaning depends on labor conditions, real income, inflation, credit access, and hard spending data.

What consumer confidence means

Consumer confidence measures how households feel about the economy and their own financial situation. It is usually discussed through survey-based indexes that summarize whether consumers feel more optimistic or more cautious about current conditions and the future outlook.

Consumer confidence is soft data. It captures perceptions, expectations, and reported attitudes. It does not measure how much households actually spent, how much income they received, or whether credit conditions are easy enough to support future purchases.

That makes consumer confidence useful, but easy to overread. It can show how households perceive the economic environment, yet it still needs confirmation from harder data before it becomes meaningful for demand or market-regime interpretation.

What consumer confidence measures

Consumer confidence usually reflects a mix of household views about current economic conditions, future expectations, personal finances, employment prospects, income security, and willingness to make spending-related decisions.

The exact structure depends on the survey provider, so the safest interpretation is conceptual unless a specific provider methodology is being cited. At a broad level, the reading is trying to capture whether households feel secure enough to spend, borrow, save less, or make larger financial commitments.

That connection should stay qualified. A confident household may be more willing to spend, but confidence alone does not prove spending will rise. Actual behavior can still be constrained by inflation, debt service, job insecurity, falling real income, or tighter credit access.

How consumer confidence connects to demand

Consumer confidence matters because household perception can influence spending appetite. When households feel secure about jobs, income, and future conditions, they may be more willing to spend or borrow. When they feel uncertain, they may delay purchases, increase savings, or become more cautious about credit.

Consumer confidence sequence: household perception → spending, saving, and credit appetite → demand expectations → aggregate demand context → policy and market-regime interpretation → hard-data confirmation.

This is why consumer confidence is best read as a demand-context indicator, not as a final answer. It can help explain whether household behavior may become more supportive or more cautious, but the interpretation becomes stronger only when spending, labor, income, inflation, and credit data point in the same direction.

Consumer confidence vs consumer sentiment vs consumer spending

Consumer confidence, consumer sentiment, and consumer spending are closely related, but they are not interchangeable. The main difference is whether the measure captures perception or realized behavior.

| Concept | What it captures | Data type | Common mistake |

|---|---|---|---|

| Consumer confidence | Household confidence about economic conditions, personal finances, and the outlook | Soft survey data | Treating it as actual spending |

| Consumer sentiment | A related household sentiment and expectations survey family | Soft survey data | Treating every survey family as identical |

| Consumer spending | Actual expenditure behavior by households | Harder realized data | Ignoring that spending can diverge from confidence |

Consumer confidence and consumer sentiment both belong to the soft-data family because they measure household attitudes rather than actual purchases. Consumer spending is different because it records what households did. A strong macro read separates those categories instead of collapsing them into one broad consumer-demand signal.

When consumer confidence can mislead

Consumer confidence can mislead when survey responses and hard behavior move in different directions. Households may feel pessimistic because prices are high, but still spend because employment is stable. They may also report confidence while cutting discretionary purchases because debt costs, rent, food, or energy absorb more income.

The reading can also be distorted by labor stress. If confidence weakens while initial jobless claims, hiring conditions, or wage income are also deteriorating, the signal becomes more concerning than a survey decline by itself.

Common false read: A falling confidence reading does not automatically mean recession. A rising reading does not automatically mean stronger markets. The useful question is whether the survey is confirmed by income, employment, credit, inflation, and realized spending data.

A simple interpretation sequence

A cleaner way to use consumer confidence is to separate the reading from the confirmation stack. The survey can suggest a direction of household mood, but hard data decides whether that mood is becoming economic behavior.

| Reading | What it can suggest | What must confirm it | Common mistake |

|---|---|---|---|

| Rising confidence | Households may feel more willing to spend, borrow, or make larger purchases | Actual spending, wage income, credit conditions, and labor data | Assuming markets must rise |

| Falling confidence | Households may become more cautious about spending and borrowing | Spending slowdown, labor stress, credit pressure, and income weakness | Assuming recession is automatic |

| Confidence-spending divergence | Survey perception and actual behavior are not aligned | Consumption data, wage income, savings buffers, and credit access | Treating surveys as hard data |

| Confidence with labor stress | Household outlook may be weakening for more structural reasons | Claims, hiring, wages, income, and broader labor-market evidence | Reading confidence alone |

Practical scenario: confidence falls but spending holds up

A common scenario is that consumer confidence falls because households feel pressure from prices, uncertainty, or negative economic headlines. At the same time, actual spending can remain firm if employment is still stable, wage income is holding up, and households still have access to credit or savings buffers.

In that situation, the survey is not useless. It may show that households are becoming more cautious. But the macro interpretation stays incomplete until hard data shows whether that caution is changing behavior. If spending remains firm and labor income is stable, weak confidence may be an early warning rather than a confirmed demand slowdown.

The opposite can also happen. Confidence may improve before spending meaningfully accelerates. If credit is expensive, real income is weak, or households are already stretched, better survey responses may not quickly turn into stronger demand.

How to use consumer confidence in market-structure analysis

Consumer confidence is most useful as one input in the labor-consumption-demand sequence. It helps frame how households feel, but it should not replace the data that shows what households are actually doing.

A stronger interpretation checks consumer confidence alongside labor conditions, real income, inflation pressure, credit access, savings behavior, and actual spending. When those pieces align, confidence can add useful context to demand pressure. When they conflict, the conflict is often more important than the confidence reading itself.

For market-structure analysis, the key is not whether confidence is good or bad in isolation. The key is whether household perception is beginning to affect spending behavior, demand expectations, policy sensitivity, margins, credit conditions, and the broader risk environment.

Is consumer confidence a market signal?

Consumer confidence is not a standalone market signal. It can influence the way analysts think about household demand, but it does not provide a direct buy or sell message, and it does not prove that a market regime has changed.

The same confidence reading can have different meanings in different environments. Weak confidence with strong jobs and stable income is different from weak confidence with rising labor stress and falling spending. Strong confidence with easing inflation is different from strong confidence that is offset by tighter credit or weaker real income.

The safest use is conditional: consumer confidence can suggest where household perception is moving, but its macro value depends on confirmation from harder economic data.

FAQ

Is consumer confidence the same as consumer sentiment?

No. They are related soft-data concepts, but they are not identical. Consumer confidence usually refers to confidence survey or index readings, while consumer sentiment is a related survey family focused on household sentiment and expectations. The exact distinction should be handled carefully when naming a specific provider.

Does consumer confidence predict consumer spending?

Consumer confidence can help frame spending appetite, but it does not mechanically predict spending. Actual spending can diverge from survey responses because of labor income, inflation, savings, credit conditions, and debt costs.

Is consumer confidence a market signal?

No. Consumer confidence can be part of a macro interpretation process, but it is not a standalone trading signal, market forecast, or policy prediction tool.