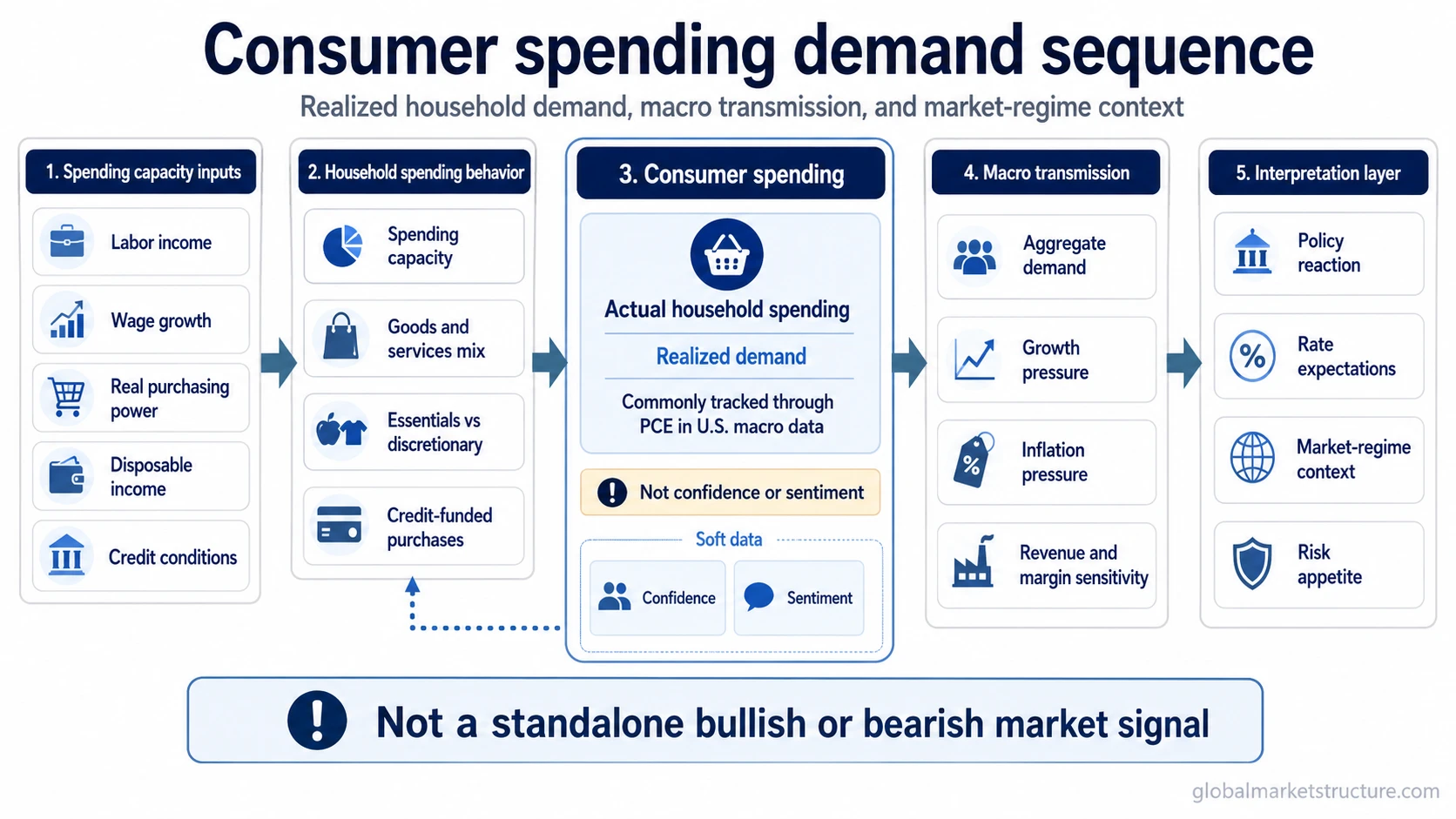

Consumer spending is actual household spending on goods and services. In U.S. macro data, it is commonly tracked through personal consumption expenditures, or PCE. Realized household demand can influence growth, inflation pressure, corporate revenue, and policy expectations. Its market meaning still depends on income, prices, credit, margins, and policy reaction, so it is not a standalone bullish or bearish signal.

For market-regime interpretation, consumer spending is most useful when it is read as part of a demand sequence. Households need income, purchasing power, and credit access before spending can support broader demand. The same spending number can mean different things depending on whether inflation is easing, wages are rising, credit is tightening, or policymakers are responding to persistent demand.

What consumer spending means

Consumer spending refers to money households spend on final goods and services. It includes everyday categories such as food, housing-related services, transportation, healthcare, recreation, and other goods and services purchased by households. The macro focus is not whether one household spends more or less, but whether household demand is strong enough to affect output, inflation, business revenue, and policy expectations.

In the United States, the main macro measurement frame is personal consumption expenditures, commonly shortened to PCE. PCE is closely watched because it connects household spending to national income accounting, inflation measurement, and the broader growth picture. Other household-spending sources can add useful detail, but they are not interchangeable with PCE.

| Concept | What it means | How it relates to consumer spending |

|---|---|---|

| Consumer spending | Actual household spending on goods and services. | The core concept: realized household demand. |

| PCE | Personal consumption expenditures, a major U.S. macro measurement frame. | One of the main ways consumer spending is tracked in official macro data. |

| Consumer confidence | Survey-based household views about economic conditions and expectations. | Soft data that may influence spending appetite, but it is not actual spending. |

| Consumer sentiment | Survey-based mood and expectations about personal finances and the economy. | Another soft-data input, not a substitute for observed spending behavior. |

| Aggregate demand | Economy-wide demand for goods and services. | A broader demand category that includes consumer demand alongside other sources. |

| Wage growth and real wages | Income growth and purchasing-power inputs. | Upstream drivers that can support or constrain household spending capacity. |

How consumer spending is measured

PCE is the central U.S. macro frame for consumer spending because it is tied to official national accounts. It can be viewed in nominal terms, where price changes are included, or in real terms, where inflation adjustment helps show changes in purchasing volume. That distinction matters because spending can rise in dollars even when households are not buying much more in real terms.

The Bureau of Labor Statistics Consumer Expenditure Surveys provide a different lens on household expenditures. They can help describe household spending patterns, but they serve a different purpose from PCE. Treating PCE and consumer expenditure survey data as identical can blur the difference between macro accounting and household survey detail.

Current values, release changes, and short-term surprises need dated source support. Without a current official release and date, consumer spending should be discussed as a macro concept rather than as a live data dashboard.

Where consumer spending fits in the demand chain

Consumer spending sits downstream from labor income, purchasing power, and credit conditions. It is realized demand, not a survey expectation. That is why it often carries more macro weight than confidence or sentiment alone, while still needing context before it can be interpreted.

Demand sequence: labor income and real wages → disposable income → credit conditions → spending capacity → spending mix → aggregate demand → growth and inflation pressure → policy and market-regime interpretation.

The sequence begins with household income. Strong wage growth can improve spending capacity, but the real effect depends on inflation. If prices rise faster than wages, nominal income growth may not translate into stronger real demand.

Credit conditions also matter. Households can maintain spending for a period through borrowing, lower saving, or delayed adjustment. That can support demand in the short run, but it may become less durable if debt service rises, lending standards tighten, or real incomes weaken.

At the macro level, household spending feeds into aggregate demand. The broader interpretation depends on whether consumer demand is reinforcing growth, sustaining inflation pressure, absorbing higher prices, or beginning to weaken beneath headline activity.

Why consumer spending matters for growth, inflation, and policy

Strong consumer spending can support economic growth because businesses see demand for goods and services. That can help revenue, production plans, hiring, and earnings expectations. The interpretation is not automatically positive for markets, because strong demand can also keep inflation pressure elevated.

When spending remains firm while supply is constrained or pricing power stays strong, policymakers may read the demand backdrop as less compatible with rapid easing. In that environment, the same spending strength that supports growth can also keep rates, real yields, or expected policy settings restrictive.

Weak consumer spending can point to cooling demand. That can reduce growth expectations and pressure revenue-sensitive sectors. It can also reduce inflation pressure or shift expectations toward easier policy if the weakness becomes broad enough. The market reaction depends on which force dominates: slower growth, lower inflation, policy relief, margin pressure, or risk appetite.

Consumer spending also affects corporate margins. If households keep spending because nominal wages are rising, businesses may protect revenue. If spending only holds because prices are higher while volumes weaken, margins and earnings quality may look more fragile. The mix between goods, services, essentials, discretionary spending, and credit-funded purchases changes the signal.

Common false readings

Consumer spending is not a standalone market signal. Strong spending is not automatically bullish, and weak spending is not automatically bearish. The useful question is what the spending data says about demand, inflation, income, credit, margins, and policy reaction together.

A strong spending report can look supportive for growth but uncomfortable for inflation. A weak spending report can look negative for revenue but supportive for lower inflation or easier policy expectations. The direction of the market response depends on the surrounding regime, not the spending number alone.

Another common mistake is treating confidence or sentiment as if they were spending. Survey data can help frame household mood, but households may say they feel cautious while still spending, or express confidence before actual spending improves. Hard spending data and soft survey data answer related but different questions.

A third false reading is ignoring prices. Nominal spending can rise because households are paying more, not because real demand is expanding strongly. Real spending, inflation, wages, and credit conditions need to be read together before drawing a macro conclusion.

Illustrative demand scenario

A practical scenario is a period where consumer spending remains firm while inflation is still above the level policymakers want. Businesses may see revenue support, but central-bank expectations may stay restrictive because demand has not cooled enough. In that setting, spending strength can support the growth side of the macro picture while also limiting policy relief.

The opposite scenario can also occur. Spending may slow as real wages weaken and credit becomes more expensive. That can pressure growth-sensitive sectors, but it may also reduce inflation pressure and change policy expectations. The same spending slowdown can therefore carry both risk-off and policy-relief implications, depending on the broader context.

How to interpret consumer spending in a market-regime framework

Consumer spending becomes more useful when it is interpreted through several questions at once. Is spending rising in real terms or only in nominal dollars? Is income growth supporting it? Are households using credit to maintain it? Is inflation cooling or staying sticky? Are margins improving or being squeezed? Are rate expectations easing or tightening?

| Spending backdrop | Possible macro reading | What can change the interpretation |

|---|---|---|

| Strong real spending with stable inflation | Demand may be supporting growth without immediate inflation stress. | Credit, wages, margins, and policy expectations still need confirmation. |

| Strong nominal spending with sticky inflation | Revenue may look firm, but policy relief may be harder to price. | Real volumes and purchasing power become important checks. |

| Weak spending with easing inflation | Demand may be cooling, possibly shifting policy expectations. | The balance between growth risk and policy relief drives market meaning. |

| Weak spending with tight credit | Household demand may be under pressure from financing conditions. | Labor income and debt-service stress help judge durability. |

The strongest interpretation comes from a sequence, not one release. Consumer spending is more informative when it is aligned with labor income, real wages, credit conditions, inflation data, business margins, and policy communication. When those signals conflict, the spending data should be treated as one part of the regime map rather than as a final answer.

FAQ

Is consumer spending the same as PCE?

No. Consumer spending is the broader concept of household spending on goods and services. PCE is a major official U.S. measurement frame used to track that spending in macro data.

Is consumer spending the same as consumer confidence?

No. Consumer confidence is survey-based soft data about household views and expectations. Consumer spending is actual observed spending behavior. Confidence can influence spending appetite, but it is not the spending itself.

Why does consumer spending matter for markets?

Consumer spending can affect growth, inflation pressure, business revenue, margins, and policy expectations. Its market meaning depends on the surrounding macro regime, so it should not be treated as a standalone signal.

Can strong consumer spending be negative for markets?

It can be, depending on context. Strong spending may support growth and revenue, but it may also sustain inflation pressure or keep policy expectations restrictive if demand remains too firm.