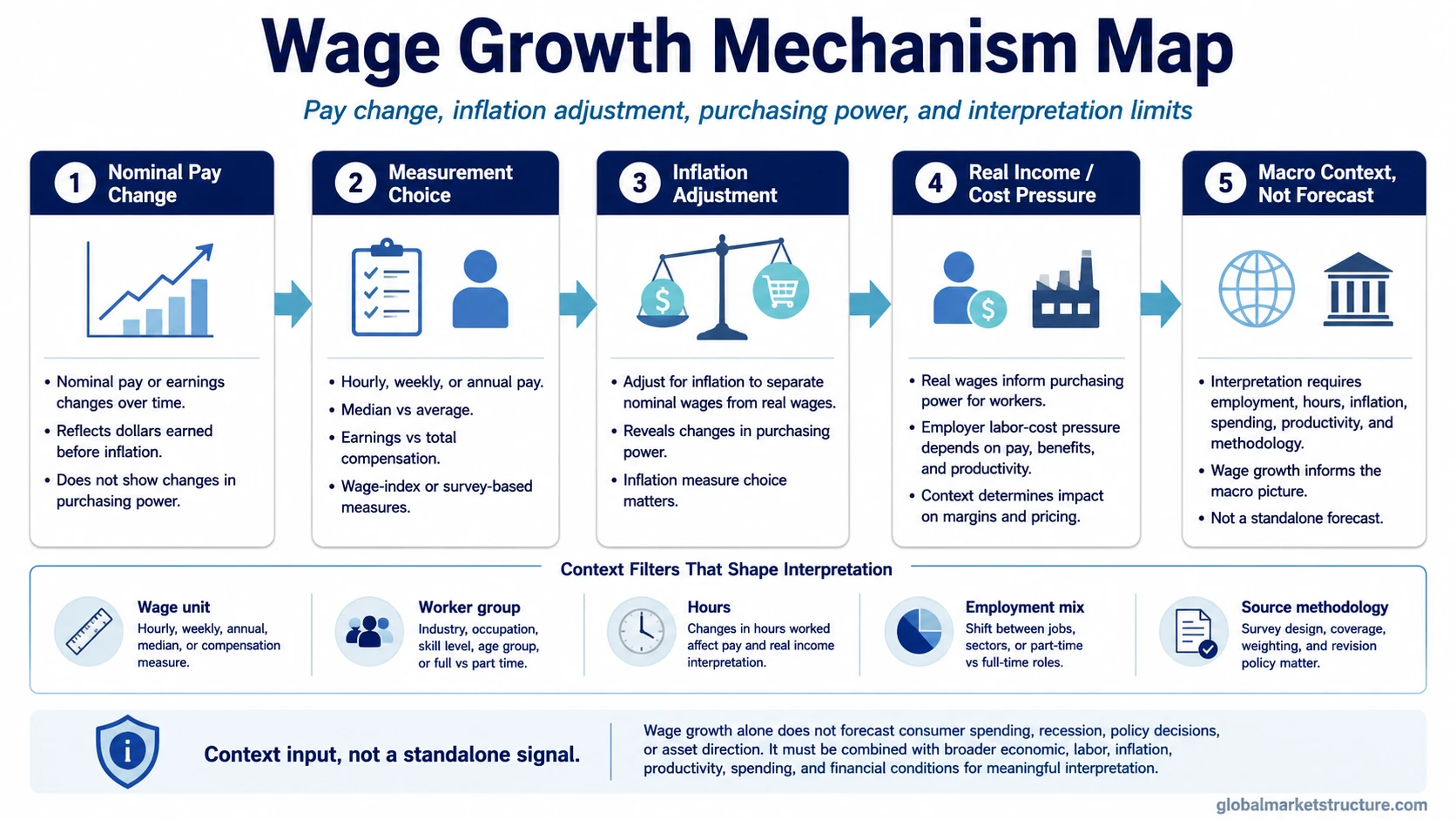

Wage growth is the change in wages or earnings over time, usually stated in nominal terms unless explicitly adjusted for inflation. It helps interpret labor income, household-income context, and employer cost pressure, but it is not automatically real purchasing power or a spending forecast. The reading depends on wage unit, worker group, inflation, hours worked, employment mix, and source methodology.

Definition: Wage growth measures how pay changes over a period. It can refer to hourly wages, weekly earnings, median worker-level wage changes, compensation, or a source-specific wage index. The term is not complete until the measure, population, period, and inflation treatment are clear.

What Wage Growth Is and What It Is Not

Wage growth is useful because it sits between labor-market conditions and household-income interpretation. It can show whether pay is rising, whether employer labor costs are increasing, and whether nominal income is adding pressure to the broader macro environment.

The boundary matters because the same phrase can be misread in several ways. A nominal wage increase does not prove that workers can buy more after inflation. A rising average earnings series does not necessarily mean the typical worker received the same raise. Wage growth also does not replace labor slack, employment, or demand indicators.

Wage growth is: pay change over time, a labor-income input, an employer cost-pressure input, and a context variable for inflation and demand interpretation.

Wage growth is not: automatically real wage growth, not the same as the unemployment rate, not proof of stronger consumer spending, not a recession forecast, not a policy forecast, and not an asset-market direction signal.

How Wage Growth Is Measured

Different wage-growth measures answer different questions. A headline wage number can describe an average, a median worker, an hourly rate, a weekly paycheck, or a broader compensation concept. The interpretation changes when hours, worker mix, benefits, inflation, and data methodology change.

| Measure | What it captures | What it can miss | Best use |

|---|---|---|---|

| Nominal wage growth | Change in wages before inflation adjustment. | Whether purchasing power improved after prices changed. | Reading pay pressure, labor-income growth, and employer wage costs. |

| Real wage growth | Wage growth adjusted for inflation. | Differences across worker groups, regions, hours, and job mix. | Interpreting purchasing-power change rather than nominal pay change. |

| Average hourly earnings | Average pay per hour for a covered worker group. | Weekly income changes caused by fewer or more hours worked. | Separating hourly pay pressure from total paycheck behavior. |

| Average weekly wages | Total weekly pay, affected by both wages and hours. | Whether the change came from hourly pay or hours worked. | Reading worker paycheck behavior. |

| Median wage growth | Typical worker-level wage change in a distribution. | Aggregate labor-cost pressure across all workers and employers. | Reducing distortion from extreme earners or composition shifts. |

| Compensation growth | Wages plus benefits or broader labor compensation. | Cash wage behavior if benefits are driving the move. | Reading total employer labor-cost pressure. |

| Wage index | A source-specific wage measure designed to control for some mix effects. | Direct comparison with simpler headline wage series. | Following cleaner methodology when the source design is understood. |

The most common mistake is comparing wage-growth figures as if they measure the same thing. An hourly wage measure, a weekly earnings measure, a median worker measure, and a compensation index can move differently even when the same labor market is being observed.

How Wage Growth Connects to Macro Interpretation

Wage growth can affect macro interpretation through several channels. Rising pay can support labor income. If pay rises faster than inflation, real purchasing power may improve. If pay rises quickly while productivity growth is weak, employer cost pressure may become more relevant for inflation and margins.

This does not make wage growth a standalone forecast. Household demand depends on more than pay growth, including employment, hours worked, taxes, savings, credit availability, debt service, wealth effects, and confidence. Wage growth is one input inside that broader structure.

Useful interpretation sequence:

- Start with the wage measure: hourly, weekly, median, compensation, or index-based.

- Check whether the figure is nominal or inflation-adjusted.

- Identify the worker group, sector, and methodology.

- Compare wage growth with inflation to assess purchasing-power pressure.

- Compare wage growth with productivity and margins to assess employer cost pressure.

- Cross-check with employment, hours, unemployment, labor-force participation, and demand indicators.

Why High Wage Growth Can Be Misread

High wage growth can be positive for workers, but the macro meaning depends on what else is happening. If inflation is higher than wage growth, real purchasing power may still be falling. If wage growth is concentrated in a narrow sector, it may not describe the typical worker. If weekly wages rise because hours increase, the signal differs from a broad rise in hourly pay.

Composition can also distort the reading. Average wages may rise if lower-paid workers leave the measured workforce, even if remaining workers did not receive large raises. A median measure may avoid some average-wage distortion, but it can still be shaped by methodology and sample design.

Interpretation limit: Wage growth should not be used alone to predict consumer spending, recession risk, central-bank decisions, or asset direction. It becomes more useful when combined with inflation, employment, hours, productivity, margins, and broader demand conditions.

Wage Growth Example in Context

A simple example shows why the distinction matters. If nominal wages rise 5% while inflation is 7%, workers may receive larger paychecks but still lose purchasing power in real terms. If nominal wages rise 4% while inflation is 2%, the real-wage picture is more favorable, but the demand effect still depends on employment, hours, credit conditions, and household balance sheets.

The same logic applies to employer cost pressure. A wage increase may be easier for firms to absorb if productivity rises, pricing power is strong, or margins are wide. It becomes more difficult to interpret as a cost-pressure signal when productivity is weak, margins are already compressed, or wage increases are concentrated in specific industries.

Practical reading: Wage growth is most useful when it is treated as a conditional macro input. The question is not only whether pay is rising. The question is which pay measure is rising, for whom, relative to what inflation rate, with what hours worked, and under what labor-market conditions.

Related Concepts for Interpreting Wage Growth

Wage growth is closely related to consumer spending, but it does not determine spending by itself. Spending also depends on real income, savings, credit, wealth effects, and confidence.

It also interacts with the unemployment rate. A tight labor market can support wage pressure, but unemployment and wage growth are not the same measure. Wage data describe pay behavior, while unemployment describes labor-market slack.

For purchasing-power analysis, wage growth should be separated from real wage growth. For demand analysis, it should be read alongside employment, hours, and inflation. For cost-pressure analysis, it should be read alongside productivity, margins, and pricing power.

FAQ

What is wage growth?

Wage growth is the change in wages or earnings over time. It is usually stated in nominal terms unless the source says it has been adjusted for inflation.

Is wage growth the same as real wage growth?

No. Wage growth usually refers to pay growth before inflation adjustment. Real wage growth adjusts pay growth for inflation to show whether purchasing power improved.

Does high wage growth always mean consumer spending will rise?

No. Consumer spending also depends on inflation, employment, hours worked, savings, credit, debt service, confidence, taxes, and wealth effects.

Why do different wage-growth sources show different numbers?

Different sources may use different worker groups, wage units, time periods, inflation adjustments, and methodologies. Hourly wages, weekly wages, median wage growth, compensation, and source-specific indexes are not interchangeable.