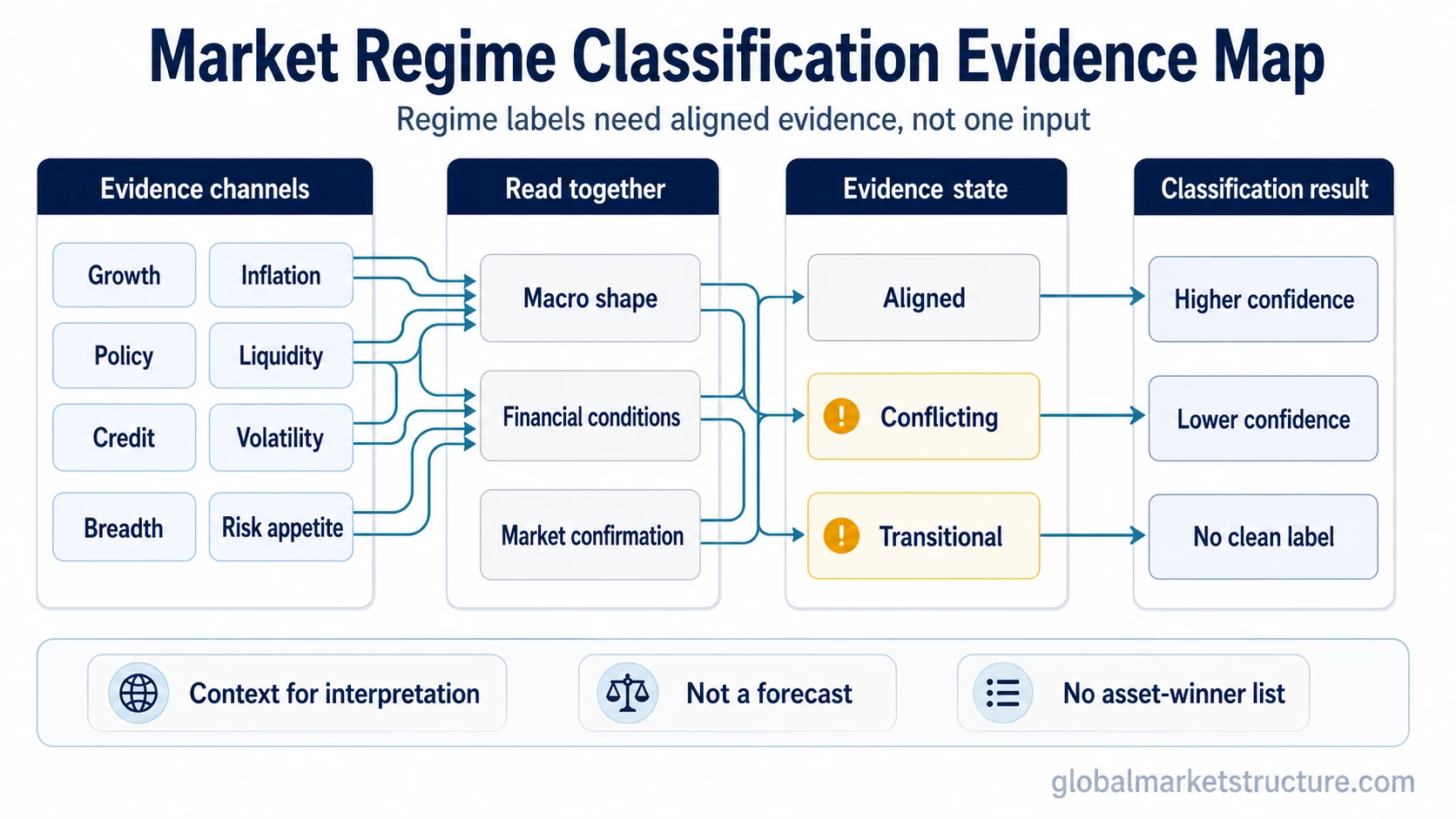

Market regime classification is the process of grouping market environments by reading several evidence channels together, including growth, inflation, policy, liquidity, credit, volatility, breadth, and risk appetite. A regime label is useful as context for interpretation, but it is not a forecast, a trading instruction, or a list of assets that should outperform.

The useful question is not whether one indicator is rising or falling. The useful question is whether several channels are pointing toward the same broad condition, or whether the evidence is too mixed to support a confident label.

A market regime describes the broader backdrop. A classification framework explains how that backdrop is identified without turning the label into a prediction.

Key Points

- Market regime classification works best as a multi-channel evidence stack.

- No single indicator is enough to classify a regime by itself.

- Growth and inflation describe the macro shape, while policy, liquidity, credit, volatility, breadth, and risk appetite help confirm or challenge the reading.

- A regime label is conditional. Confidence falls when the evidence conflicts.

- Classification is context for interpretation, not a market forecast or trading system.

Why Regime Classification Needs Several Channels

Market environments are broad conditions, not isolated price moves. A rising equity index, a higher volatility reading, or a change in yields can matter, but none of those signals is enough on its own.

Classification becomes more useful when the evidence is grouped by role. Growth and inflation help define the macro condition. Policy and liquidity show whether financial conditions are becoming easier or tighter. Credit, volatility, breadth, and risk appetite show whether market behavior confirms or contradicts that backdrop.

A macro regime reading should not be reduced to one economic release or one chart. The label should reflect a pattern of conditions, not a single data point.

Market Regime Classification Signal Stack

A signal stack separates each channel by what it helps classify, what confirms the reading, and what weakens it. The goal is not to make every input agree perfectly. The goal is to avoid giving one signal more authority than it deserves.

For example, an inflation regime reading becomes more meaningful when price pressure aligns with policy, yields, liquidity, earnings pressure, and market breadth. Inflation alone is not enough to classify the whole environment.

| Channel | What it helps classify | Confirming evidence | What weakens the reading | Related concept |

|---|---|---|---|---|

| Growth | Expansion, slowdown, recession, or recovery. | Growth-sensitive indicators move together. | Data is mixed, lagging, revised, or contradicted by markets. | Macro regime |

| Inflation | Whether price pressure is regime-relevant. | Inflation aligns with policy, yields, margins, and pricing. | Pressure is falling, narrow, temporary, or offset by weak demand. | Inflation regime |

| Policy | Easing, tightening, or neutral policy conditions. | Guidance, rates, balance-sheet direction, and conditions align. | Policy language and market pricing disagree. | Macro regime context |

| Liquidity | Whether funding and risk capacity support markets. | Liquidity aligns with breadth, credit, and risk appetite. | One liquidity channel improves while funding stress rises elsewhere. | Market regime context |

| Credit | Whether risk pricing is improving or deteriorating. | Spreads, funding, and risk assets tell a consistent story. | Equities rise while credit stress increases, or credit stays calm while growth weakens. | Macro regime context |

| Volatility | Calm, unstable, transitional, or crisis-like stress. | Volatility aligns with liquidity, credit, breadth, and risk appetite. | Volatility rises briefly without credit, liquidity, or breadth confirmation. | Volatility regime |

| Breadth | Whether participation supports the headline move. | Leadership expands or narrows in line with the regime reading. | Index strength depends on narrow leadership while participation weakens. | Market regime context |

| Risk appetite | Preference for risk exposure, defense, or liquidity. | Cross-asset behavior shows consistent risk-seeking or risk-reducing behavior. | Risk assets, defensive assets, credit, and volatility conflict. | Risk appetite |

How to Sequence the Evidence

A practical classification process starts with the macro condition, then checks whether markets are confirming it. That sequence helps prevent a short-term market move from becoming the whole regime story.

| Step | Question | Purpose |

|---|---|---|

| 1. Define the macro backdrop | Are growth and inflation improving, slowing, overheating, or deteriorating? | Sets the broad regime candidate. |

| 2. Check policy and liquidity | Are financial conditions supporting risk-taking or restricting it? | Shows whether the macro backdrop is being amplified or restrained. |

| 3. Confirm with credit and volatility | Are stress and risk pricing aligned with the regime candidate? | Tests whether hidden pressure is building beneath headline price action. |

| 4. Test breadth and risk appetite | Is participation broad, narrow, defensive, speculative, or mixed? | Shows whether investor behavior confirms the label. |

| 5. Label confidence, not certainty | Does the evidence align, conflict, or remain transitional? | Prevents the label from becoming false precision. |

Qualitative judgment, rule-based scoring, statistical clustering, and machine learning can all be used inside this process. The method matters less than the discipline of separating evidence, conflict, and uncertainty.

Classification Is Not Prediction

Regime classification describes the current or developing backdrop. It does not automatically predict the next market move. A market can remain in the same broad regime while prices move sharply in both directions.

The classification becomes safer when it is treated as an interpretation filter. It can help explain why some signals deserve more attention under certain conditions, but it should not be used as a standalone instruction.

A volatility regime can change the interpretation of the same macro backdrop. Calm volatility may support a stable reading, while rising stress can weaken confidence even before the macro data fully confirms a transition.

For example, a risk-seeking environment does not simply mean all risky assets should rise. The reading depends on liquidity, credit, breadth, volatility, positioning, and the reason risk appetite is improving.

Practical Scenario: When Evidence Conflicts

A common illustrative scenario is an equity index making new highs while market breadth narrows, credit spreads stop improving, and volatility begins rising from a low base. A simple bull-market label would miss the internal disagreement.

The classification stack would treat the headline index as one input, not the final answer. If liquidity remains supportive and credit stress stays contained, the regime may still look resilient. If breadth keeps weakening while credit and volatility deteriorate together, confidence in a stable risk-on label falls.

This is where risk appetite has to be read as one confirmation channel rather than the entire regime label. The point is not to force a bearish or bullish conclusion. The point is to mark the environment as lower-confidence until the evidence resolves.

When Regime Labels Become Unreliable

Regime labels are weakest during transitions. Growth, inflation, policy, liquidity, and market behavior often turn at different speeds. A framework that demands one clean label too early can create false confidence.

| Failure mode | Why it creates risk | Better handling |

|---|---|---|

| Single-indicator classification | One input receives too much authority. | Require confirmation from several channels. |

| Volatility-only reading | Stress can rise briefly without a regime change. | Check credit, liquidity, breadth, and risk appetite together. |

| Risk-on / risk-off shortcut | Risk appetite is treated as the whole regime. | Use it as confirmation, not as the full classification. |

| Lagging macro data | Economic releases may confirm conditions after markets have started adjusting. | Separate confirmed data from forward-looking market behavior. |

| Overfitted model output | A statistical label may look precise while missing changing context. | Review whether the label makes sense across macro, liquidity, and market channels. |

| Asset-winner framing | The regime label turns into a performance promise. | Keep classification separate from allocation or trade decisions. |

What the Framework Connects

Market regime classification sits above several lower-level readings. Macro conditions identify the economic shape, inflation shows price-pressure context, volatility shows stress behavior, and risk appetite shows whether markets are rewarding or reducing exposure.

The framework becomes most useful when those components are read together. Alignment raises confidence in the label. Conflict lowers confidence and may point to a transition rather than a stable regime.

FAQ

Is market regime classification the same as forecasting?

No. Classification describes the broader backdrop. Forecasting tries to estimate what may happen next. A regime label can inform interpretation, but it does not predict the next market move by itself.

Which indicators are used to classify market regimes?

Common inputs include growth, inflation, policy, liquidity, credit, volatility, market breadth, and risk appetite. The framework is stronger when those inputs are checked together instead of relying on one indicator.

Can machine learning classify market regimes?

Machine learning can be used as one classification method, but model output still needs interpretation. A statistical label can be useful, but it should not be treated as the objective truth without checking the underlying evidence and limitations.

Why can regime labels become misleading?

Regime labels become misleading when evidence is mixed, data is lagging, transitions are underway, or one signal is treated as the whole market environment. Classification should mark uncertainty when the evidence does not align.