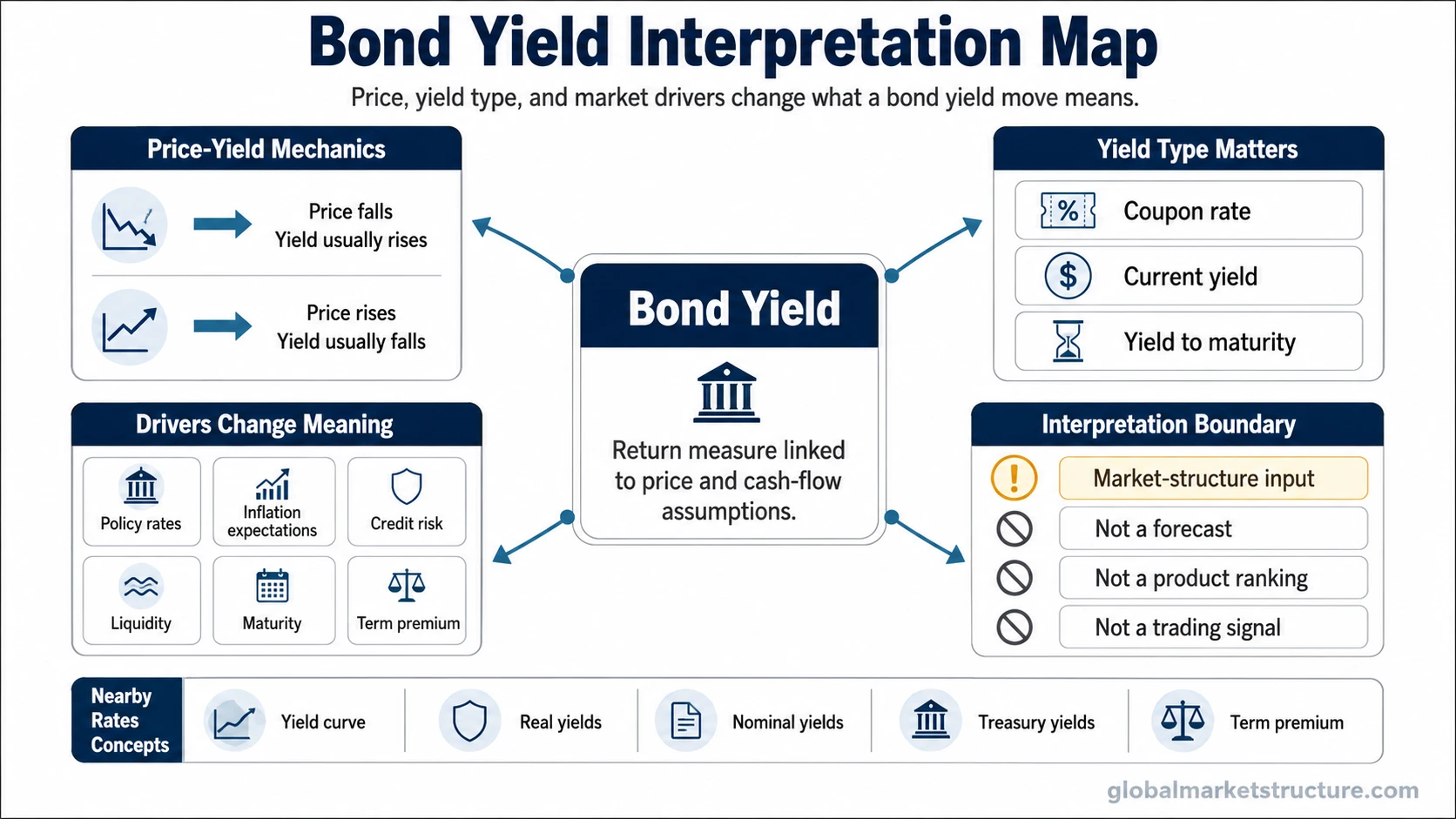

Bond yields are the return implied by a bond’s price and promised cash-flow terms. When a bond’s price falls, its yield usually rises; when its price rises, its yield usually falls. For market interpretation, the useful question is not only whether yields are higher or lower, but which yield is being discussed and what is driving the move.

Key points

- Bond yield is a rate of return measure tied to a bond’s price, coupon payments, maturity, and repayment terms.

- Bond prices and yields usually move in opposite directions because the same fixed cash flows become more or less attractive as price changes.

- Coupon rate, current yield, and yield to maturity answer different questions and should not be treated as the same number.

- A yield move can reflect inflation pressure, central-bank policy, credit risk, liquidity, maturity, or term premium.

- Bond yields are market-structure inputs, not automatic forecasts, product rankings, or buy/sell signals.

What bond yields mean

A bond yield expresses the return connected to owning a bond under a defined set of price and cash-flow assumptions. A bond normally has a face value, a coupon payment, a maturity date, and a market price. The yield links those elements into a rate that helps compare one bond, maturity, or credit condition with another.

The word “yield” can create confusion because it is not always one calculation. A quoted yield may refer to the coupon rate, the income return based on the current price, or a broader estimate that includes coupon payments, price paid, maturity, and repayment at face value. The meaning depends on the yield type.

Why bond prices and yields move in opposite directions

Most bonds promise a stream of cash flows. If the bond’s market price falls while those promised payments remain the same, the return available to a new buyer rises. If the bond’s market price rises, the same cash flows are being purchased at a higher cost, so the available yield falls.

This inverse relationship is central to bond-market interpretation. A rising yield can mean that investors are demanding more compensation, that market interest rates have risen, that credit risk is being repriced, or that liquidity has weakened. A falling yield can reflect lower rate expectations, stronger demand for safer assets, or changing growth and inflation expectations.

Coupon rate, current yield, and yield to maturity

Different yield measures answer different questions. Treating them as interchangeable can create a false reading of bond income, expected return, and market pressure.

| Yield measure | What it focuses on | What it does not prove |

|---|---|---|

| Coupon rate | The fixed interest payment as a percentage of the bond’s face value. | It does not show the return available at today’s market price. |

| Current yield | Annual coupon income relative to the bond’s current market price. | It does not fully include maturity value, reinvestment assumptions, or total return. |

| Yield to maturity | The estimated annualized return if the bond is held to maturity and assumptions are met. | It is not a guaranteed realized return, especially if the bond is sold early or assumptions change. |

What drives bond yields

Bond yields move for more than one reason. The same rise in yield can carry a different meaning depending on whether the driver is inflation, policy rates, credit risk, liquidity, maturity structure, or risk compensation.

| Driver | How it can affect yields | Market-structure interpretation |

|---|---|---|

| Policy rates | Expected central-bank policy can influence short and intermediate maturities. | Yields may reflect changing monetary conditions rather than only bond-specific demand. |

| Inflation expectations | Higher expected inflation can push nominal yields higher as investors demand compensation. | A higher nominal yield may not mean a higher real return if inflation expectations rise too. |

| Credit risk | Riskier issuers may need to offer higher yields to attract capital. | A higher yield can reflect compensation for default or downgrade risk, not simply better value. |

| Liquidity conditions | Less liquid bonds may trade at lower prices and higher yields. | Yield pressure can reveal market depth or funding stress, especially when selling becomes forced. |

| Maturity | Longer maturities often carry more sensitivity to rate expectations and term compensation. | The maturity point matters because short-term and long-term yields can move for different reasons. |

| Term premium | Investors may require extra compensation for holding longer-term bonds. | A long-term yield move can reflect changing risk compensation, not only expected policy rates. |

Bond yields and the yield curve

A single bond yield describes one bond or one maturity point. The yield curve connects yields across maturities, usually from short-term to long-term rates. That curve shape can show whether the market is pricing a normal upward slope, a flatter structure, or an inversion.

The curve matters because a short-term yield and a long-term yield may move for different reasons. Short maturities may be more sensitive to near-term policy expectations, while longer maturities may reflect inflation expectations, growth expectations, duration demand, and term premium. A bond-yield move becomes more useful when its maturity point and curve context are clear.

Bond yields versus related rates concepts

Bond yields overlap with several rates concepts, but each term has a different job. Keeping the boundaries clear prevents one yield move from being overread.

| Concept | Meaning | Boundary |

|---|---|---|

| Bond yields | Return measures connected to bond prices and promised cash flows. | The broad concept can apply across government, corporate, municipal, and other bonds. |

| Treasury yields | Yields on U.S. government Treasury securities. | They are important benchmarks, but they are not the same as all bond yields. |

| Nominal yields | Yields stated before adjusting for inflation. | They show the quoted rate, not the inflation-adjusted return. |

| Real yields | Yields adjusted for inflation or inflation expectations. | They help separate stated yield from purchasing-power-adjusted yield. |

| Yield curve | The relationship between yields at different maturities. | It is a curve structure, not one standalone bond yield. |

Common false reading

A higher bond yield does not automatically mean a better investment, a stronger economy, or a reliable market forecast. Higher yield may compensate for higher inflation, weaker credit quality, lower liquidity, longer maturity risk, or a wider term premium. The yield is only meaningful after the driver is identified.

The opposite mistake is treating falling yields as automatically positive. Falling yields may reflect lower inflation pressure, weaker growth expectations, demand for safety, or expectations of easier policy. The interpretation changes with the surrounding evidence.

Illustrative scenario

A corporate bond may show a higher yield after its price falls. That higher yield could look attractive if viewed only as income, but the reason matters. If the move comes from weaker issuer confidence or thinner market liquidity, the yield may be compensation for higher risk. If the move comes from broad policy-rate repricing while credit conditions remain stable, the interpretation is different.

What bond yields do not show on their own

Bond yields do not, by themselves, predict stocks, recessions, or future central-bank decisions. They are one input in a broader rates and market-structure framework. A stronger interpretation usually compares yields with inflation expectations, credit spreads, liquidity conditions, maturity structure, and cross-asset risk appetite.

Yield to maturity also should not be read as a guaranteed realized return. It depends on assumptions such as holding the bond to maturity, payment timing, reinvestment, and issuer repayment. Selling before maturity, credit events, or liquidity stress can change the outcome.

How bond yields connect to nearby rates concepts

Bond yields connect bond price, coupon terms, maturity, and yield measures. Treasury yields refer to U.S. government benchmark rates. Nominal yields state the quoted yield before inflation adjustment, while real yields adjust the interpretation for inflation. The yield curve compares yields across maturities rather than describing one standalone bond yield.

Credit-sensitive yield moves can also connect with credit spreads, because the spread between safer and riskier debt can show how much extra compensation investors demand for credit risk.

FAQ

What are bond yields in simple terms?

Bond yields are return measures connected to a bond’s price and cash-flow terms. They help show what return is implied by the bond’s coupon payments, market price, maturity, and repayment assumptions.

Why do bond yields rise when bond prices fall?

When a bond’s price falls, the same promised cash flows can be purchased at a lower price. That usually raises the yield available to a new buyer. When the price rises, those same cash flows cost more, so the yield usually falls.

Is a higher bond yield always better?

No. A higher yield can reflect higher income potential, but it can also reflect higher inflation risk, credit risk, liquidity risk, maturity risk, or term premium. The driver matters more than the headline yield alone.

Are bond yields and Treasury yields the same?

No. Treasury yields are yields on U.S. government Treasury securities. Bond yields are the broader category and can include government, corporate, municipal, and other bond markets.