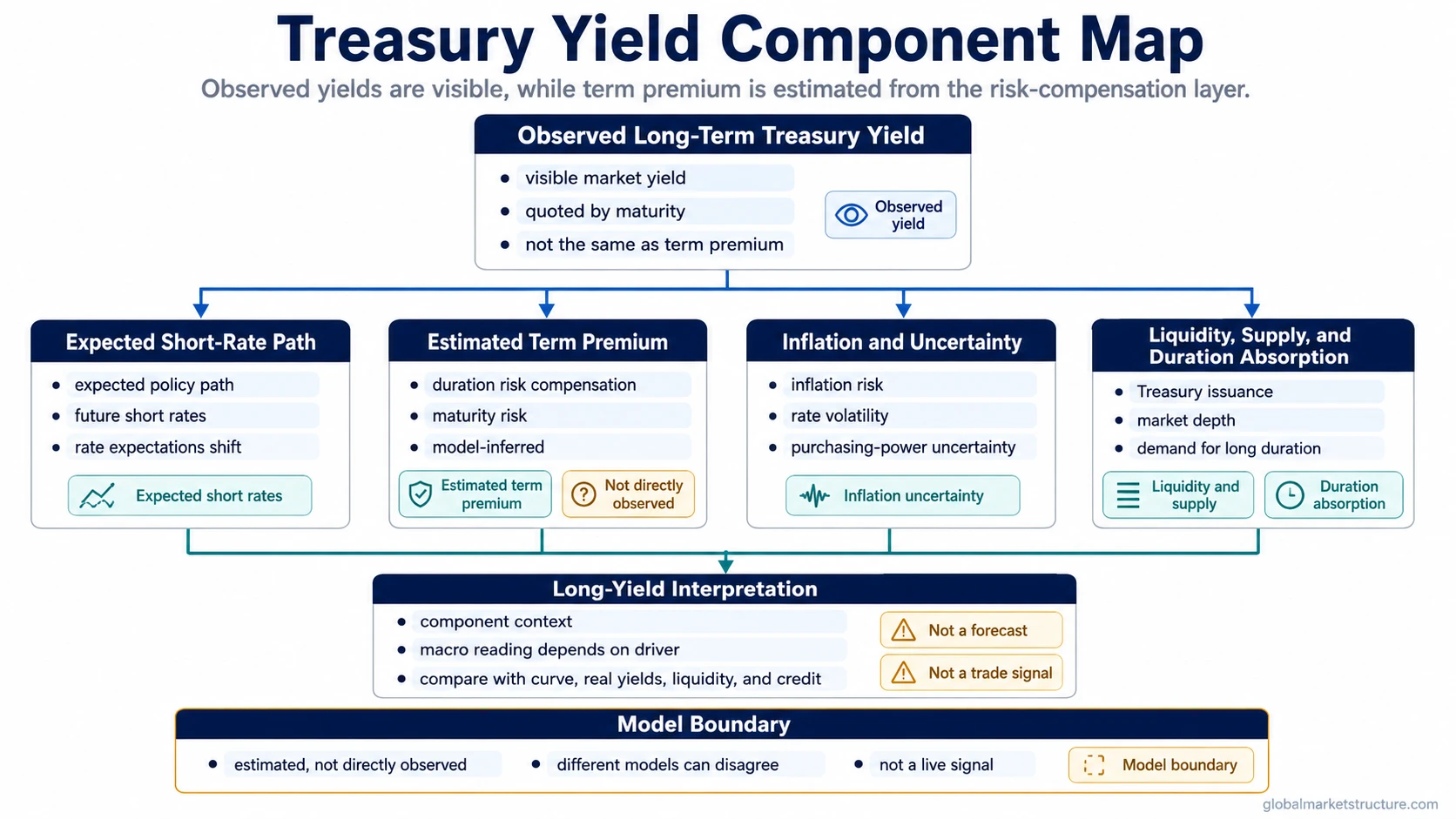

Treasury term premium is the estimated extra compensation investors require for holding longer-maturity Treasury risk instead of repeatedly rolling short-term rates. It is not the whole Treasury yield, not a real yield, and not a direct market forecast.

The concept separates long-end yield moves driven by the expected path of short-term interest rates from moves linked to risk compensation, inflation uncertainty, liquidity, Treasury supply, and demand for long-duration exposure.

Definition: Treasury term premium is an estimated component of a longer-term Treasury yield that reflects compensation for bearing maturity, duration, and interest-rate uncertainty beyond the expected path of short-term rates.

| Term premium is | Term premium is not |

|---|---|

| Estimated risk compensation for holding longer-maturity Treasury exposure. | A directly observed market yield quoted on a screen. |

| One component in long-yield analysis. | The whole 10-year Treasury yield. |

| Model-dependent and sensitive to assumptions. | A single true number that every model must match. |

| A context input for long-end yield moves. | A forecast, recession trigger, or market timing signal. |

How Treasury Term Premium Fits Into Long-Term Yields

A longer-term Treasury yield can be interpreted as a combination of expected future short-term rates, term premium, and model-specific assumptions. The observed yield is visible in the market. The term premium is inferred from a model that tries to separate the expected rate path from the compensation required for holding longer maturity risk.

A simplified decomposition is:

Long-term Treasury yield = expected future short rates + term premium + model or estimation residual.

This decomposition is analytical, not a separate quoted instrument. Two models can look at similar market data and produce different term-premium estimates because they may use different assumptions about inflation expectations, rate expectations, volatility, risk preferences, or the statistical behavior of yields.

| Component | What it represents | Why it matters | Limitation |

|---|---|---|---|

| Expected short-rate path | Market-implied or model-estimated expectations for future short-term policy rates. | Helps separate longer-yield moves caused by expected policy-rate changes. | Expectations are inferred and can shift quickly with growth, inflation, and policy data. |

| Term premium | Estimated compensation for bearing longer-maturity interest-rate risk. | Helps identify whether investors require more or less reward to hold duration risk. | It is not directly observable and varies by model. |

| Inflation uncertainty | Uncertainty around future purchasing power and inflation outcomes. | Can increase the compensation demanded for holding long fixed-rate cash flows. | Inflation risk is related to term premium but not identical to real yield. |

| Liquidity / supply / duration absorption context | Market depth, Treasury issuance, balance-sheet capacity, and demand for duration. | Can affect how much compensation buyers require to absorb longer-maturity supply. | These forces can overlap, making clean attribution difficult. |

Why Term Premium Can Change

Term premium can rise when investors demand more compensation for holding longer-duration Treasury exposure. That demand can come from higher rate volatility, more inflation uncertainty, heavier Treasury supply, weaker balance-sheet capacity, or reduced willingness to hold long maturities at existing yields.

Term premium can fall when long-duration Treasuries are in stronger demand, inflation uncertainty is lower, expected policy risk feels more contained, or investors accept lower compensation for maturity risk. In risk-off environments, demand for long-duration safety can sometimes compress term premium, although the result depends on inflation, liquidity, and policy context.

Limitation: A term-premium estimate does not identify one clean cause by itself. A model may show higher estimated compensation, but the final reading depends on Treasury supply, inflation uncertainty, rate volatility, liquidity, risk appetite, and the expected policy path.

Current estimate boundary: Current term-premium estimates should be checked against dated model data, because the estimate changes over time and can differ across models.

Term Premium vs Nearby Yield Concepts

Term premium is easiest to misread when it is blended with nearby yield concepts. Nominal yields are stated market yields before inflation adjustment. Real yields adjust the yield lens for inflation expectations or realized inflation context. Term premium is different: it is an estimated risk-compensation component inside longer-term yield analysis.

| Concept | Main idea | How it differs from term premium |

|---|---|---|

| Observed Treasury yield | The market yield quoted for a Treasury maturity. | Term premium is only one inferred component of that observed yield. |

| Expected short-rate path | The expected future path of short-term policy rates. | Term premium is the compensation beyond that expected rate path. |

| Nominal yield | The stated yield before inflation adjustment. | Term premium can influence nominal yield analysis, but it is not the same concept. |

| Real yield | A yield lens adjusted for inflation expectations or inflation context. | Term premium reflects maturity risk compensation, not simply inflation adjustment. |

| Yield curve shape | The relationship between shorter and longer Treasury yields. | Term premium can affect curve interpretation, but the curve also reflects expected policy and growth conditions. |

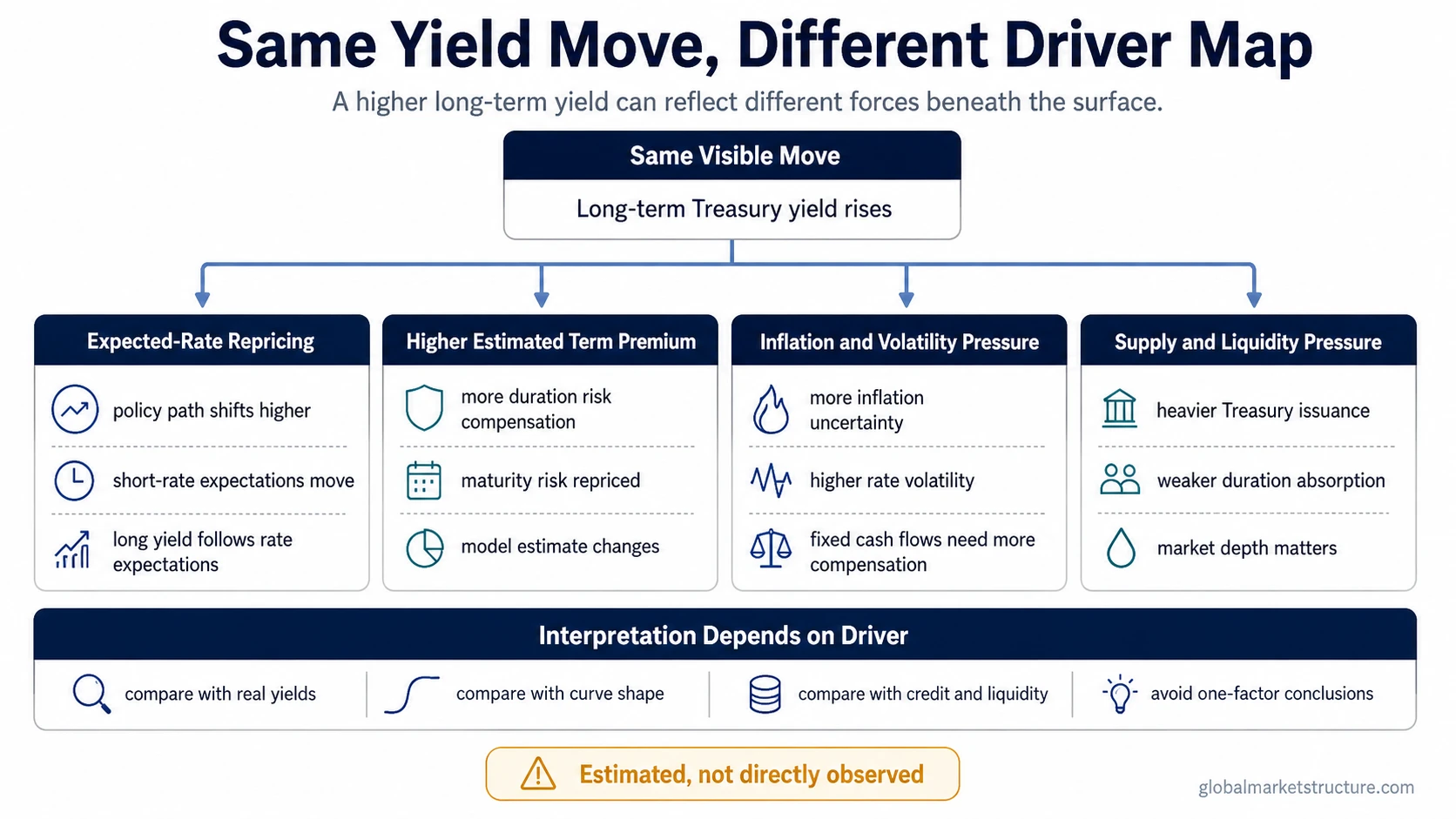

Term premium also changes how curve moves are read. During curve steepening, a rising long-end yield can mean different things depending on whether the move is mostly expected-rate repricing, higher risk compensation, inflation uncertainty, or supply absorption pressure.

Practical Scenario: Same Yield Move, Different Meaning

A common scenario is a rise in the 10-year Treasury yield while short-rate expectations are not moving much. The first read may be that markets are pricing a more restrictive policy path, but that read is incomplete if the expected short-rate path is stable. A term-premium lens would ask whether investors are demanding more compensation for inflation uncertainty, rate volatility, Treasury supply, or duration risk.

The same yield increase means something different if the expected policy path is also moving higher. In that case, the yield move may be more about short-rate expectations than term premium. A cleaner macro read compares the expected-rate component, inflation expectations, real yields, liquidity, credit conditions, and curve shape before assigning one driver to the long-end move.

Common Misreadings

Misreading 1: Term premium is the whole 10-year yield. The 10-year yield is observed in the market. Term premium is an estimated component used to interpret part of that yield.

Misreading 2: Term premium is directly observable. Term premium is inferred through models. Different models can disagree because their assumptions and inputs differ.

Misreading 3: Term premium is the same as real yield. Real yield is an inflation-adjusted yield concept. Term premium is compensation for maturity and duration risk beyond expected short rates.

Misreading 4: Higher term premium automatically means recession risk. Term premium can interact with growth, inflation, liquidity, supply, and risk appetite, but it should not be treated as a standalone recession indicator.

Misreading 5: Term premium gives a bond allocation rule. A term-premium estimate can inform market interpretation, but it does not decide portfolio exposure by itself.

How Term Premium Fits Into Market-Structure Interpretation

Term premium works best as a context input. A higher estimate can change the reading of a long-end yield move, but the signal becomes more useful when it is compared with nominal yields, real yields, inflation expectations, credit spreads, liquidity conditions, Treasury supply, and curve behavior.

For example, a higher long-end yield alongside stable short-rate expectations, wider credit spreads, and weaker liquidity conditions carries a different market message than a higher long-end yield alongside stronger growth expectations and stable credit. The term-premium lens helps separate risk-compensation pressure from a simple policy-rate story.

Clean interpretation sequence: start with the observed Treasury yield, separate expected short-rate repricing from estimated term premium, compare inflation and real-yield context, then read the move against yield-curve shape, liquidity, credit, and broader risk appetite.

Related Concepts

Nominal yields: useful for separating stated market yield from inflation-adjusted and component-based interpretation.

Real yields: useful for distinguishing inflation-adjusted yield pressure from term-risk compensation.

Yield curve: useful for connecting maturity structure, expected policy path, and long-end compensation.

Curve steepening: useful when long-end yields move more than short-end yields and the driver needs to be separated.

FAQ

Is term premium directly observable?

No. Term premium is estimated through models. The observed Treasury yield is visible in the market, but the term-premium component must be inferred from assumptions about expected short rates, risk compensation, and related market variables.

Is term premium the same as real yield?

No. Real yield is an inflation-adjusted yield concept. Term premium is estimated compensation for holding longer-maturity Treasury risk beyond the expected path of short-term rates.

Does a higher term premium predict a recession?

No. A higher estimate can reflect changing risk compensation, inflation uncertainty, supply pressure, or rate volatility, but it should not be used alone as a recession indicator or market forecast.