Curve steepening is a yield-curve change where the spread between longer-term and shorter-term interest rates widens. It can occur when long-term yields rise faster, short-term yields fall faster, or both maturities move in unequal proportions. The market meaning depends on the driver behind the move, not only on the steeper curve shape.

Definition: Curve steepening means the yield curve becomes steeper as the gap between longer-maturity and shorter-maturity yields increases.

The slope change matters more than the direction of any single yield. A curve can steepen even when some yields are falling, as long as shorter-term yields fall more than longer-term yields. It can also steepen when longer-term yields rise more than shorter-term yields. The same visible shape can therefore reflect very different rate, policy, inflation, and risk conditions.

How Curve Steepening Works

A yield curve compares interest rates across maturities. Curve steepening occurs when the difference between a longer maturity and a shorter maturity increases. A common way to describe the move is through a spread such as a 10-year yield minus a 2-year yield, but the same logic can apply to other maturity pairs.

For example, if a longer-term yield rises while a shorter-term yield is stable, the spread widens. If a shorter-term yield falls while a longer-term yield is stable, the spread also widens. If both move, the curve steepens only when the longer-shorter spread becomes larger.

| Yield movement | Effect on curve slope | Basic interpretation |

|---|---|---|

| Long-term yields rise faster than short-term yields | The spread widens | The market may be repricing inflation, term premium, fiscal risk, supply conditions, or future nominal growth. |

| Short-term yields fall faster than long-term yields | The spread widens | The market may be repricing expected policy easing, weaker near-term growth, or lower front-end rate expectations. |

| Both maturities move, but the long-short spread increases | The curve steepens | The slope change matters more than the direction of any single yield. |

Curve Steepening vs a Steep Yield Curve

Curve steepening is a process. A steep yield curve is a shape. The difference matters because a curve can already be steep without steepening further, and a relatively flat curve can steepen from a low starting point.

A static curve shape describes the level of the spread at one point in time. Steepening describes how that spread changes over time. Confusing the two can lead to false readings, especially when the curve is moving from inversion toward a less inverted or positively sloped shape.

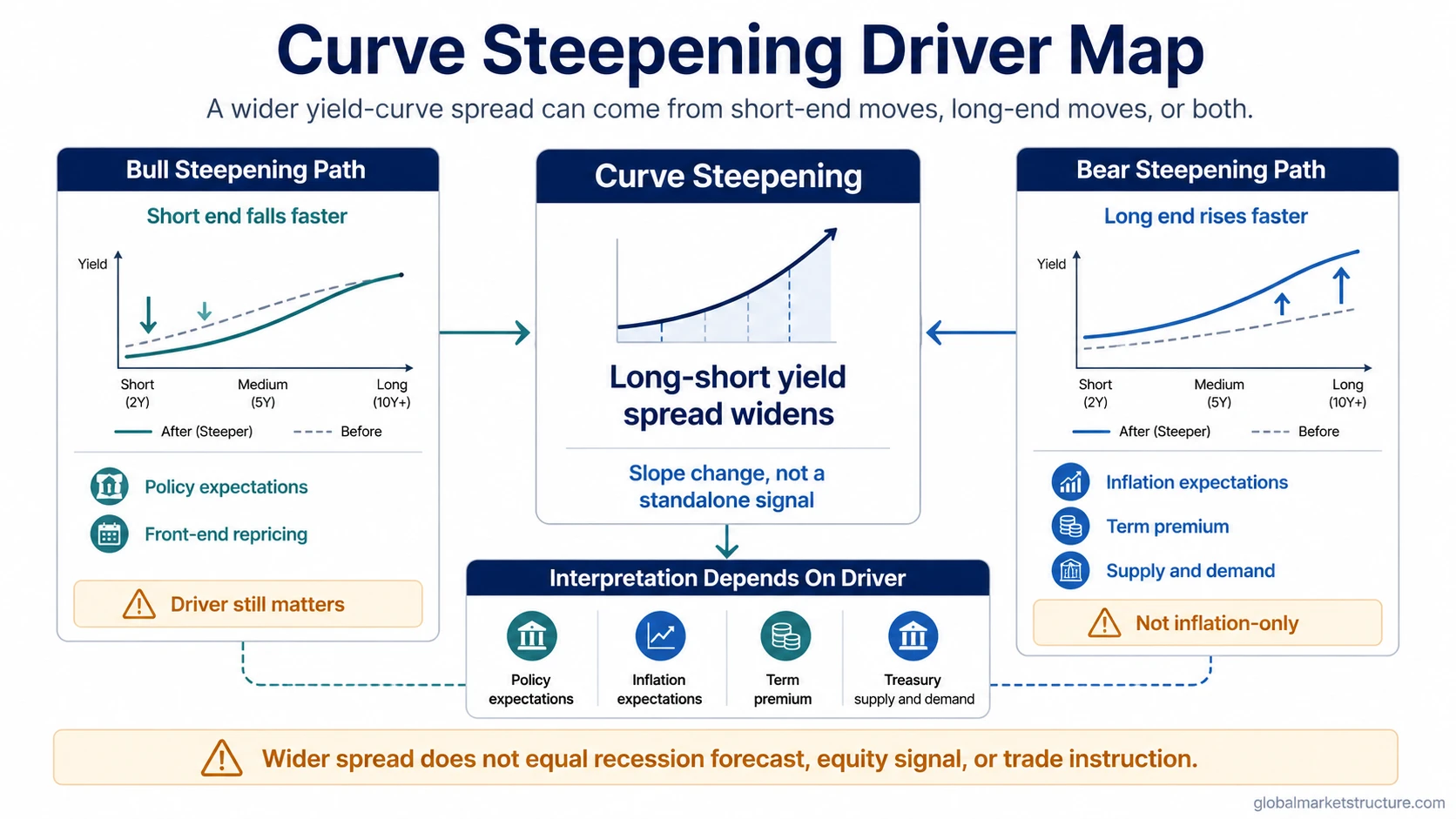

Bull Steepening vs Bear Steepening

Bull steepening and bear steepening classify different ways the curve can steepen. They are descriptive labels for yield-curve behavior, not recommendations or market signals by themselves.

| Classification | Typical yield movement | What usually drives attention | Main limitation |

|---|---|---|---|

| Bull steepening | Short-term yields fall faster than long-term yields. | Policy-rate expectations, weaker near-term growth expectations, or front-end repricing. | It does not automatically mean risk conditions are improving. The reason short-end yields are falling matters. |

| Bear steepening | Long-term yields rise faster than short-term yields. | Inflation expectations, higher real-rate pressure, wider term premium, Treasury supply and demand conditions, or stronger nominal growth expectations. | It does not always mean inflation is the only driver. Long-end yields can rise for several different reasons. |

The bull versus bear label is useful because it separates the direction of the steepening from the driver. A bull steepener and a bear steepener can both widen the curve, but they often point to different parts of the rates market doing the work.

Driver Map for Curve Steepening

Curve steepening becomes more useful when the driver is identified. The same widening spread can reflect easier expected policy, higher long-end compensation, inflation concern, supply and demand pressure, or shifting growth expectations.

| Driver | Where it may show up | How it changes interpretation |

|---|---|---|

| Policy expectations | Front-end yields fall as markets price lower future policy rates. | Steepening may reflect easier expected monetary conditions, but the reason for expected easing still matters. |

| Inflation expectations | Longer-term yields rise as investors demand more compensation for future inflation risk. | Steepening may signal pressure at the long end rather than improvement in the growth outlook. |

| Term premium | Long-end yields rise even if near-term policy expectations are not changing much. | Steepening may reflect compensation for duration, uncertainty, or long-maturity risk rather than a simple policy view. |

| Treasury supply and demand | Longer maturities come under pressure if investors require higher yields to absorb supply. | Steepening may reflect market-clearing pressure in longer maturities, not only macro optimism or inflation fear. |

| Growth expectations | Long-term yields may rise if markets expect stronger nominal growth, or short-term yields may fall if near-term weakness dominates. | The same slope change can carry different messages depending on whether growth, inflation, or policy is leading the move. |

Treasury yields provide the raw maturity-by-maturity movements, while curve steepening focuses on how those movements change the slope between maturities.

Curve Steepening Is Not a Curve-Steepener Trade

Curve steepening describes a movement in the yield curve. A curve-steepener trade is a portfolio or trading expression designed to benefit if the curve steepens. Those are separate ideas.

Curve steepening does not require trade construction, leverage, duration exposure, futures, swaps, or bond allocation decisions. Treating every steepening move as a trade signal creates a category error: the curve movement is evidence to interpret, not an instruction to act.

Common False Readings

False reading: Curve steepening automatically means recession risk is gone.

Why it fails: A widening yield-curve spread does not settle the broader macro picture. Growth, inflation, policy expectations, credit conditions, liquidity, and risk appetite can point in different directions.

False reading: Bear steepening always means inflation is rising.

Why it fails: Long-end yields can rise because of inflation expectations, but also because of term premium, Treasury supply and demand conditions, real-yield repricing, or uncertainty around long-duration risk.

False reading: Curve steepening is bullish or bearish for stocks by itself.

Why it fails: Equity interpretation depends on the driver. A steepener caused by expected policy easing can differ from a steepener caused by long-end yield pressure. Credit spreads, liquidity, earnings expectations, and market breadth can change the signal.

Curve Steepening vs Curve Flattening

Curve flattening is the opposite slope process. The spread between longer-term and shorter-term yields narrows instead of widens. Both concepts describe changes in the curve, not fixed curve shapes.

| Curve process | Spread behavior | Core question |

|---|---|---|

| Curve steepening | The long-short spread widens. | Which maturity is driving the wider slope, and why? |

| Curve flattening | The long-short spread narrows. | Which maturity is compressing the slope, and why? |

How to Interpret Curve Steepening Without Overreading It

Curve steepening is best treated as a rates-market structure signal. It says that the relationship between shorter and longer maturities has changed. It does not, by itself, identify the full macro regime.

The interpretation strengthens when the curve move is compared with its driver. Policy expectations, inflation expectations, term premium, Treasury supply and demand, credit spreads, liquidity conditions, and risk-asset behavior can either reinforce or weaken the message from the curve.

Interpretation boundary: Curve steepening can be important, but it is not a standalone recession forecast, equity-market forecast, bond-return forecast, or trading signal. The slope change becomes more meaningful only when the underlying driver and surrounding market conditions are identified.

FAQ

What does curve steepening mean?

Curve steepening means the spread between longer-term and shorter-term yields widens. The curve becomes steeper because maturities move by different amounts.

Is curve steepening the same as a steep yield curve?

No. A steep yield curve is a shape at one point in time. Curve steepening is the process of the slope becoming steeper over time.

What is the difference between bull steepening and bear steepening?

Bull steepening usually describes short-term yields falling faster than long-term yields. Bear steepening usually describes long-term yields rising faster than short-term yields.

Does curve steepening predict a recession?

No. Curve steepening alone does not predict a recession or rule one out. The driver behind the move and the surrounding macro conditions matter.

Is curve steepening a trading signal?

No. Curve steepening describes a change in the yield curve. A curve-steepener trade is a separate trading or portfolio expression.