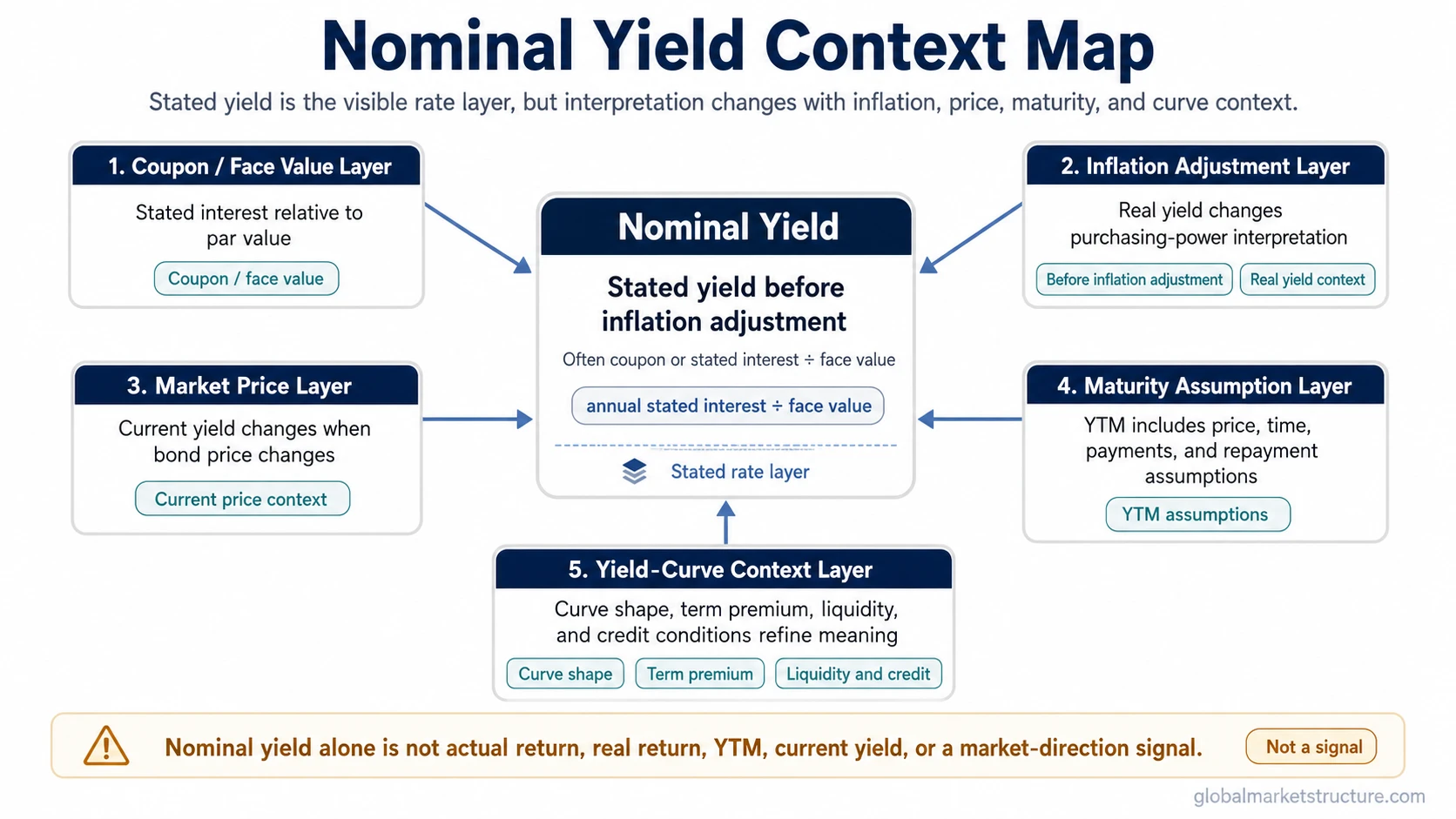

Nominal yields are stated yields before inflation adjustment. In bond usage, the term usually refers to the coupon or stated yield based on face value, not the current market price or realized return. In rates work, nominal yields identify the visible yield layer, while interpretation still depends on inflation expectations, real yields, term premium, liquidity conditions, credit behavior, and curve shape.

What Are Nominal Yields?

A nominal yield is a yield stated in non-inflation-adjusted terms. For a bond, it commonly describes the coupon or stated rate relative to the bond’s face value. That makes it useful as a simple reference point, but it does not measure purchasing-power return, market-price-based income yield, or the total return an investor may actually experience.

The useful distinction is simple: nominal yield describes the stated rate layer, while interpretation requires context. A nominal yield can help locate where a security or maturity sits in the rates structure, but it does not explain by itself why the rate is there or what it means for broader market conditions.

Nominal Yield Formula

In the basic bond context, nominal yield can be expressed as annual stated interest divided by face value.

Formula: nominal yield = annual stated interest / face value.

If a bond has a 5% coupon and a $1,000 face value, the stated annual interest is $50. That stated relationship can describe the nominal yield, but it does not show the inflation-adjusted return, the income yield based on the current market price, or the return to maturity under changing price and reinvestment assumptions.

What Nominal Yields Are and Are Not

Nominal yields are often confused with other yield measures because they all use similar language. The difference comes from what each measure adjusts for and what price base it uses.

| Concept | What it means | What it does not mean |

|---|---|---|

| Nominal yield | Stated yield before inflation adjustment, usually tied to coupon and face value | Actual return, real return, or current market yield |

| Real yield | Yield after adjusting for inflation or inflation expectations | The same thing as the stated coupon rate |

| Current yield | Annual income relative to the bond’s current market price | A face-value coupon relationship |

| Yield to maturity | A return-to-maturity estimate under assumptions about price, time, and payments | A simple stated coupon yield |

| Term premium | Compensation related to holding longer-maturity risk | A nominal yield definition |

| Yield-curve data | Observed or modeled rates across maturities | A standalone explanation of nominal yield |

Why Nominal Yields Matter for the Yield Curve

Nominal yields matter because the visible yield curve is usually discussed in nominal terms before deeper adjustments are made. Short-term and long-term nominal yields can show the surface shape of the rates structure, including whether longer maturities yield more or less than shorter maturities.

That surface view is only the first layer. A higher nominal yield can reflect different forces depending on the setting: inflation expectations, real-rate pressure, policy-rate expectations, duration risk, term premium, or changing demand for safe assets. Without that context, the same nominal-yield move can be misread.

| Possible driver | Why it changes interpretation |

|---|---|

| Inflation expectations | Nominal yields may rise while purchasing-power pressure remains unclear until real yields are checked. |

| Policy-rate expectations | Shorter maturities may respond more directly to expected central-bank policy paths. |

| Term premium | Longer maturities may move because investors require more compensation for duration and uncertainty. |

| Safe-asset demand | Yields may fall when demand for high-quality bonds rises, even if the macro story is not simple growth weakness. |

For market-structure interpretation, nominal yields are best treated as a starting input. They help frame the rates backdrop, while real yields, curve shape, liquidity conditions, and credit behavior help refine the interpretation.

Nominal Yields vs Real Yields, Current Yield, and YTM

Nominal yield and real yield answer different questions. Nominal yield states the yield before inflation adjustment. Real yield adjusts the rate for inflation or inflation expectations, which makes it more useful when the question is purchasing-power pressure rather than the visible stated rate.

Nominal yield and current yield also differ. Current yield uses the bond’s current market price, so it can change when the bond price changes. Nominal yield, in the common coupon-based bond usage, is tied to the stated interest and face-value relationship.

Yield to maturity is broader than nominal yield because it estimates return to maturity under assumptions about price, time, coupon payments, and repayment at maturity. That makes YTM a return estimate, not simply the stated yield. For a direct comparison of the inflation boundary, see nominal vs real yields.

Common Misreadings of Nominal Yields

Misreading 1: treating nominal yield as real return. A nominal yield does not adjust for inflation, so it cannot show purchasing-power return by itself.

Misreading 2: treating nominal yield as the return an investor will actually earn. Market price, holding period, reinvestment assumptions, default risk, and inflation can all change realized outcomes.

Misreading 3: treating nominal yields as a market-direction signal. A nominal-yield move can have different meanings depending on whether it is driven by growth expectations, inflation expectations, policy expectations, term premium, or liquidity conditions.

Misreading 4: treating the nominal yield curve as a complete macro explanation. Curve shape is important, but the interpretation is incomplete without inflation, real-yield context, and the term premium.

Simple Nominal Yield Example

A bond with a $1,000 face value and a 5% coupon pays $50 of stated annual interest. That 5% stated relationship can describe the nominal yield in the coupon-based sense. If the bond later trades above or below face value, the current yield changes because the market price changed. Inflation-adjusted return and return to maturity still require separate calculations.

Related Rates and Yield-Curve Concepts

Several adjacent concepts make nominal-yield interpretation more precise:

- Real yields: useful when the question is inflation-adjusted rate pressure.

- Term premium: useful when the question is compensation for longer-maturity risk.

- Nominal vs real yields: useful when the main confusion is whether the rate has been adjusted for inflation.

FAQ

Is nominal yield the same as coupon yield?

In common bond usage, they are closely related because nominal yield usually refers to the stated coupon rate relative to face value. The phrase still needs context because other yield measures may use market price, inflation adjustment, or maturity assumptions.

Are nominal yields the same as real yields?

No. Nominal yields are stated before inflation adjustment. Real yields adjust for inflation or inflation expectations.

Does nominal yield show the return an investor will actually earn?

No. Actual return depends on price paid, holding period, reinvestment assumptions, inflation, credit conditions, and other realized outcomes.