Treasury yields are the yields on U.S. Treasury securities across different maturities. They act as rates-market reference points for U.S. government debt and help explain the yield curve, but they do not by themselves predict stock direction, recession timing, Fed policy, or market timing.

Definition: Treasury yields represent the return associated with Treasury bills, notes, and bonds at different maturities. A short-term Treasury yield reflects a different part of the rates market than a 10-year or 30-year Treasury yield, so the maturity matters as much as the yield level itself.

Treasury yields can show:

- rates-market pricing across different maturities;

- the yield attached to Treasury securities at specific points on the maturity spectrum;

- inputs used to interpret the Treasury yield curve;

- nominal rate pressure before inflation adjustment.

Treasury yields do not show alone:

- exact stock-market direction;

- recession certainty or timing;

- the full inflation-adjusted pressure on markets;

- the complete Fed policy outlook;

- a complete risk-asset framework.

Treasury yields are one part of the broader bond yields universe. They are often treated as benchmark rates because U.S. Treasury securities sit near the center of global rates pricing, collateral markets, discount-rate assumptions, and yield-curve interpretation.

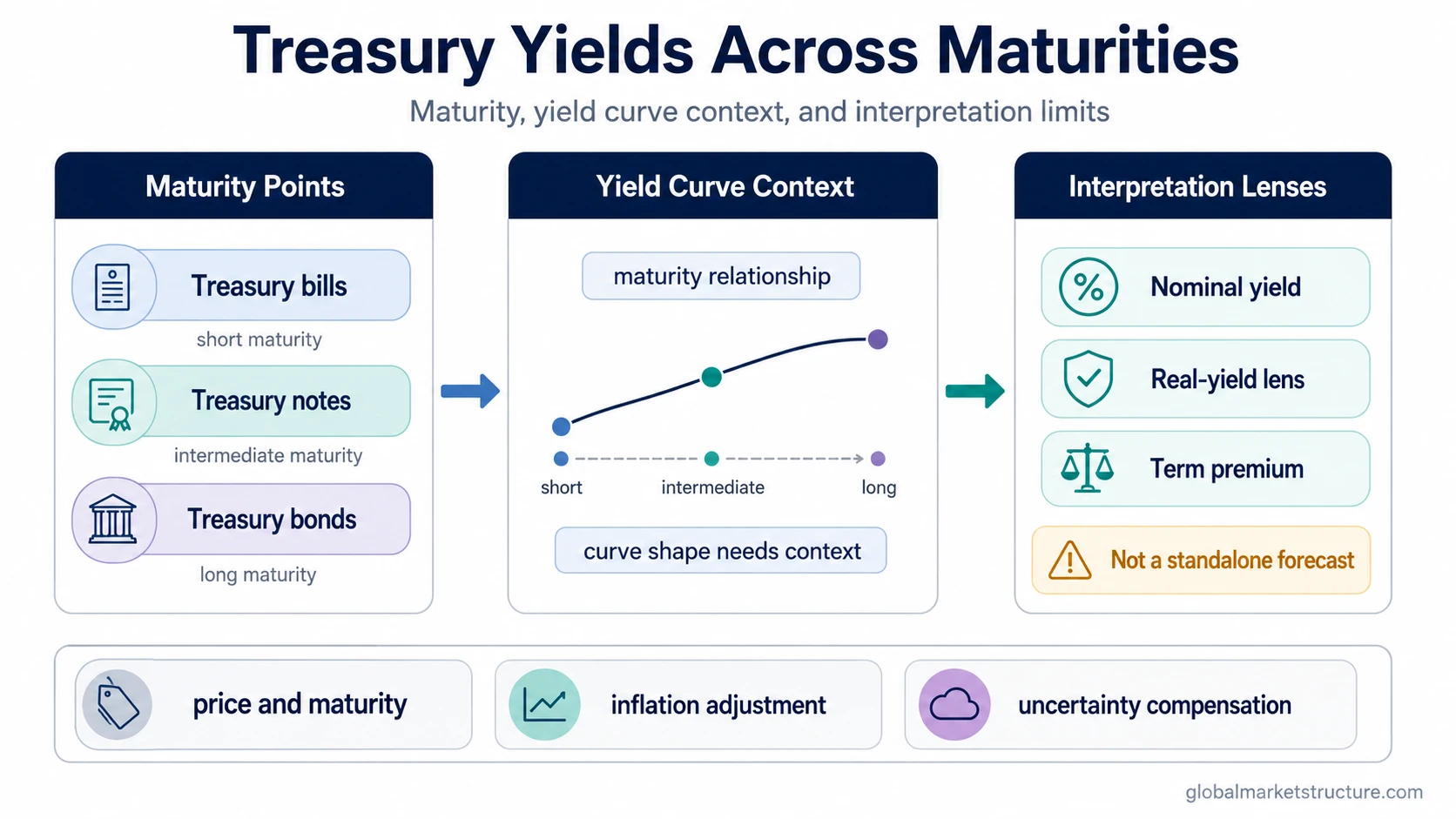

Treasury Maturity Structure

Treasury yields differ by maturity because short-term and long-term securities respond to different mixtures of policy expectations, inflation expectations, growth expectations, supply and demand, and duration risk.

| Treasury security | Typical maturity area | What its yield helps represent | Interpretation limit |

|---|---|---|---|

| Treasury bills | Short-term | Near-term rates-market pricing and short-maturity cash alternatives. | Short yields can be heavily influenced by policy expectations and money-market conditions. |

| Treasury notes | Intermediate-term | Medium-maturity expectations around policy, growth, inflation, and risk appetite. | The same note yield can reflect different drivers depending on the macro backdrop. |

| Treasury bonds | Long-term | Long-maturity pricing, duration compensation, and longer-horizon uncertainty. | Long yields can include compensation for inflation risk, uncertainty, and term premium, not only growth expectations. |

The 10-year Treasury yield is widely watched because it sits in the intermediate part of the Treasury maturity structure and often serves as a reference point for broader rates-market interpretation. That does not make it a standalone forecast.

How Treasury Prices and Yields Move

Treasury prices and Treasury yields move in opposite directions. When the price of a Treasury security rises, its yield falls. When the price falls, its yield rises.

The mechanism comes from cash-flow pricing. A Treasury security has promised payments, and the market price adjusts around those payments. If investors pay a higher price for the same stream of payments, the yield implied by that price is lower. If investors demand a lower price, the implied yield is higher.

This inverse relationship is one reason Treasury yields may move quickly when demand for safety, inflation expectations, policy expectations, or Treasury supply conditions change. The yield is not only a quote-screen number. It is also a market-clearing expression of price, maturity, and expected compensation.

How Treasury Yields Connect to the Yield Curve

Treasury yields across maturities form the Treasury yield curve. A short-term yield, a 2-year yield, a 10-year yield, and a 30-year yield are not separate facts in isolation. Together, they describe how the rates market is pricing time.

An upward-sloping curve usually means longer maturities yield more than shorter maturities. A flatter curve means the difference between short and long maturities has narrowed. An inverted curve means some shorter maturities yield more than longer maturities.

Curve shape can help interpret the relationship between policy expectations, growth expectations, inflation expectations, and risk appetite. It still needs context because the same curve shape can appear for different reasons.

Why Treasury Yields Move

Treasury yields move for several reasons, and a single yield change should not be reduced to one cause automatically.

- Fed policy expectations: Shorter maturities can react when markets reprice the expected path of policy rates.

- Inflation expectations: Yields may rise when investors demand more compensation for expected inflation risk.

- Growth expectations: Stronger growth expectations may lift yields if investors expect firmer demand, tighter policy, or less demand for safety.

- Safe-haven demand: Yields may fall when demand for Treasuries rises during periods of stress or uncertainty.

- Treasury supply and demand: Issuance, investor demand, and auction dynamics can influence pricing pressure.

- Term premium: Longer maturities can include extra compensation for uncertainty, duration exposure, and future rate risk.

The interpretation depends on the driver. A rise in yields caused by stronger growth expectations can carry a different market meaning than a rise caused by inflation pressure, weak demand for duration, or a higher term premium.

Treasury Yields, Nominal Yields, Real Yields, and Term Premium

Most quoted Treasury yields are nominal yields. They show the quoted yield before directly adjusting for inflation expectations.

Real yields add the inflation-adjusted lens. A nominal yield can look high, but the real-yield pressure depends on expected inflation and the inflation-adjusted return implied by the market.

Term premium is a separate concept. It helps explain the compensation investors may demand for holding longer-maturity securities when future inflation, policy, growth, supply, and duration uncertainty are harder to price.

Useful distinction: Treasury yields describe yields on U.S. Treasury securities. Nominal yields describe quoted yields before inflation adjustment. Real yields adjust the lens for inflation expectations. Term premium helps explain why longer maturities may require additional compensation beyond expected short-rate paths.

Same Yield, Different Meaning

A 10-year Treasury yield can rise for different reasons. It may rise because growth expectations improve, inflation expectations increase, real yields reprice higher, Treasury supply pressure builds, or term premium changes.

The market interpretation changes with the driver. A growth-led yield rise can point to stronger expected nominal activity. An inflation-led yield rise can point to pressure from purchasing-power risk. A real-yield-led move can tighten discount-rate conditions even if the nominal yield level looks similar.

The same yield level therefore does not have one fixed meaning. Maturity, inflation expectations, real-yield pressure, curve shape, and cross-asset behavior all affect the interpretation.

Common Treasury Yield Misreadings

- Reading one yield as a full market forecast: A single maturity cannot summarize the entire macro backdrop.

- Assuming all yield increases are inflation: Growth expectations, real yields, supply, and term premium can also matter.

- Assuming all yield declines mean recession: Lower yields can reflect safety demand, policy repricing, lower inflation expectations, or other drivers.

- Confusing Treasury yields with real yields: Quoted Treasury yields are usually nominal unless inflation adjustment is specified.

- Using yields as direct trading signals: Treasury yields help frame conditions, but they do not give buy or sell instructions by themselves.

Related Treasury Yield Concepts

Treasury yields sit at the center of several related rates concepts. Bond yields place Treasuries inside the broader fixed-income universe. The yield curve organizes yields by maturity. Nominal yields describe quoted yield levels before inflation adjustment. Real yields add the inflation-adjusted lens. Term premium helps explain why long-maturity yields may include compensation for uncertainty and duration risk.

A clean Treasury-yield reading usually starts with maturity, then checks whether the move is nominal, real, curve-driven, policy-sensitive, inflation-sensitive, or term-premium-related.

FAQ

Are Treasury yields the same as bond yields?

No. Treasury yields are a specific category of bond yields tied to U.S. Treasury securities. Bond yields also include corporate, municipal, agency, and other fixed-income markets.

Are Treasury yields real yields?

Most quoted Treasury yields are nominal yields unless the inflation-adjusted measure is specified. Real yields require an inflation-adjusted lens, usually tied to expected inflation or inflation-protected securities.

Why do Treasury prices and yields move in opposite directions?

They move inversely because the market price changes around a security’s cash flows. A higher price implies a lower yield from those payments, while a lower price implies a higher yield.

Can Treasury yields predict stocks or recessions?

Treasury yields can help interpret rates pressure, curve shape, and macro expectations, but they do not predict stock direction or recession timing by themselves. The interpretation depends on the wider macro and cross-asset backdrop.