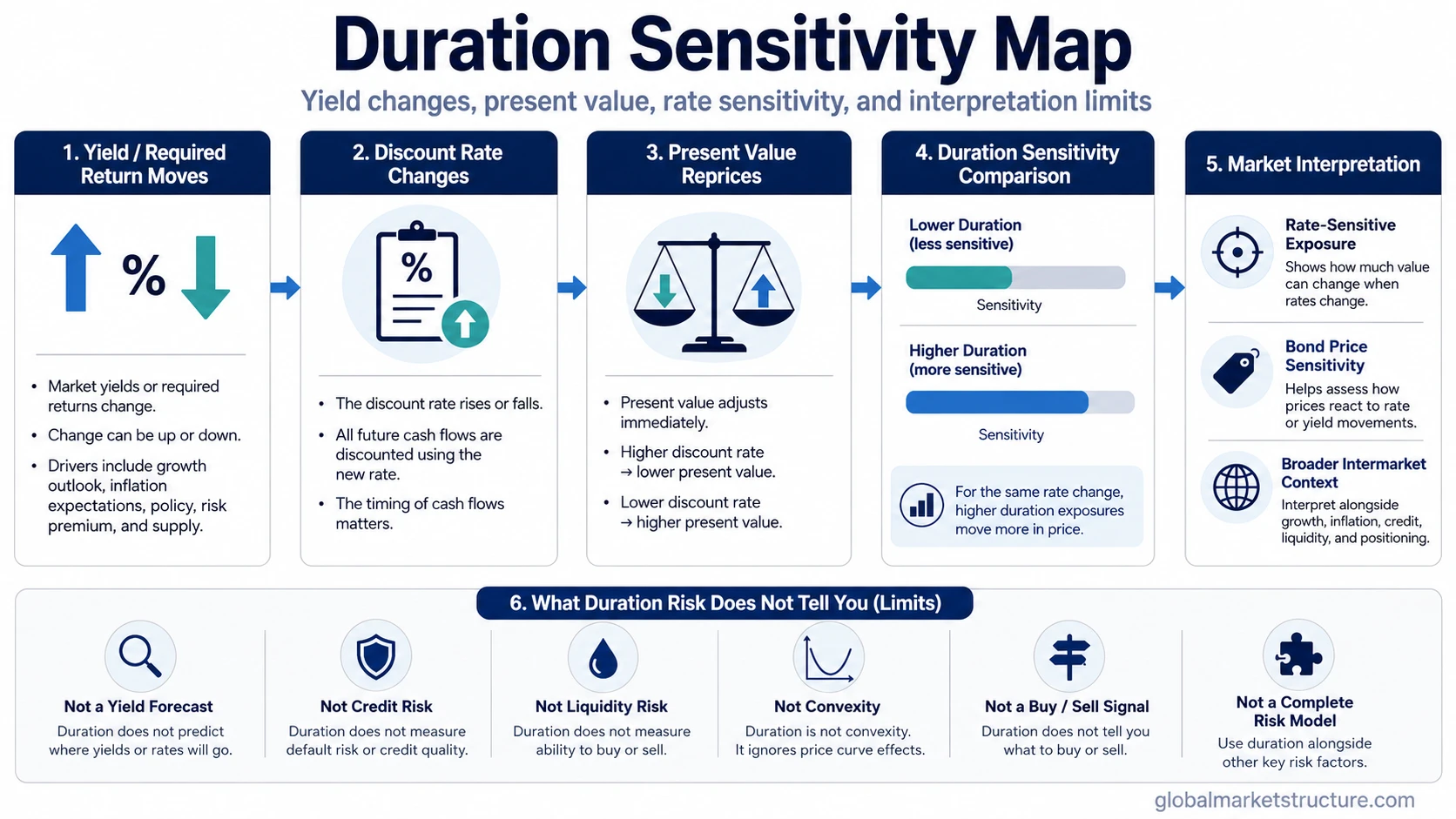

Duration risk is the risk that a bond or other rate-sensitive exposure changes in value when yields, interest rates, or required returns move. Higher duration generally means greater price sensitivity because more value depends on cash flows discounted over a longer horizon. Duration risk helps interpret rate pressure, but it does not forecast yields, measure credit risk, or explain every source of market risk.

Direct definition: Duration risk describes sensitivity to changes in yields, rates, or required returns. When the rate used to value future cash flows rises, the present value of those cash flows usually falls. When that rate falls, present value usually rises. The longer and more rate-sensitive the cash-flow profile is, the larger that reaction can be.

For bonds, duration risk is closely connected to bond duration, which is the measurement used to estimate that sensitivity. For broader market interpretation, the same idea also helps explain why long-horizon cash-flow assets can become more sensitive when the market reprices rates, inflation expectations, or required returns.

What Duration Risk Is and Is Not

Duration risk is often confused with other forms of risk because several forces can affect a bond or rate-sensitive asset at the same time. The useful distinction is that duration risk isolates sensitivity to yield or required-return changes. It does not explain every reason an asset may rise, fall, underperform, or become unstable.

| Item | Correct role | Boundary |

|---|---|---|

| Duration risk | Sensitivity to yield, interest-rate, or required-return changes | Not a forecast of where yields will go |

| Bond duration | A measurement used to estimate price sensitivity | Not identical to maturity |

| Credit risk | Issuer repayment, default, or spread risk | Separate from duration risk |

| Liquidity risk | Risk that an asset cannot be traded easily without a large price impact | Separate from rate sensitivity |

| Convexity | How rate sensitivity changes as yields move | Not replaced by duration |

| Equity-duration shorthand | A way to describe discount-rate sensitivity in some equities | Not measured exactly like bond duration |

How Duration Risk Works

The mechanism begins with valuation. A bond or rate-sensitive exposure is worth the present value of expected future cash flows. The discount rate is the required-return assumption used to convert those future cash flows into today’s value.

| Step | Mechanism | Market interpretation |

|---|---|---|

| 1. Yield or required return changes | The market reprices the return required to hold the exposure. | Rate pressure begins at the valuation input. |

| 2. Present value changes | Future cash flows are discounted at a higher or lower rate. | Longer-dated cash flows are usually more sensitive. |

| 3. Price sensitivity appears | The asset price adjusts to the changed present value. | Higher-duration exposure can move more for the same rate change. |

| 4. Intermarket meaning depends on context | The same rate move may reflect growth, inflation, policy, liquidity, or risk-premium pressure. | Duration risk helps interpret sensitivity, not the full market regime by itself. |

Coupon structure also matters because cash flows received sooner usually reduce sensitivity compared with cash flows concentrated farther in the future.

The mechanism runs from yield or required-return change to present-value effect, then to price sensitivity and broader market interpretation. Duration risk is strongest as a sensitivity lens. It is weaker when used as a stand-alone explanation for every bond, equity, or cross-asset move.

Why Curve Shape and Real vs Nominal Yields Matter

Duration risk is not only about whether rates are up or rates are down. The part of the yield curve that moves can matter. A parallel move, where many maturities shift together, is easier to summarize. A non-parallel move, where short-term and long-term yields move differently, can create a more complex sensitivity pattern.

The interpretation also changes depending on whether the pressure comes mainly from nominal yields or real yields. Nominal yields include inflation compensation and real-rate components. Real yields are often more directly connected to inflation-adjusted required returns. When real yields rise, long-duration exposures can face valuation pressure even if the growth story has not changed much.

The risk-free rate is one baseline input in the discount-rate channel. In equity analysis, required return also includes compensation for equity-specific uncertainty, often discussed through the equity risk premium. That is why duration language can appear in both bond-market and equity-market interpretation, even though the measurement is cleaner in fixed income.

A Short Illustrative Scenario

Consider two income-oriented exposures with similar headline labels. One receives most of its value from nearer cash flows. The other depends more heavily on cash flows farther in the future. If yields rise by the same amount, the second exposure can react more strongly because more of its value is tied to longer-horizon discounting.

The point is not that higher duration is automatically good or bad. The point is that labels such as defensive, income-oriented, or bond-like do not fully describe sensitivity. Duration risk asks how much value depends on future cash flows being discounted at a changing required return.

What Duration Risk Does Not Explain

Duration risk is an incomplete risk measure. It does not measure whether an issuer can repay, whether an asset can be sold easily, whether inflation will surprise, or whether a bond has call features that change the cash-flow path. It also becomes less precise when yield moves are large or when the yield curve moves unevenly.

Convexity is one important limitation. Duration gives a sensitivity estimate, while convexity describes how that sensitivity changes as yields move. That matters because the price response to a small rate move may not scale cleanly into the response to a much larger move.

Duration risk also does not prove a market regime. Rising yields may reflect stronger growth expectations, inflation pressure, tighter policy, higher term premium, liquidity stress, or a mix of forces. The duration lens shows where sensitivity exists. It does not decide the macro cause by itself.

Duration Risk in Intermarket Interpretation

Duration risk becomes useful in cross-asset work because it connects rates, valuation, bonds, and some equity behavior through the discount-rate channel. Long-duration bonds are the cleanest example, but rate sensitivity can also appear in equities whose valuation depends heavily on future earnings expectations.

That equity usage needs a boundary. Saying an equity behaves like a long-duration asset is shorthand for discount-rate sensitivity, not a precise bond-style duration measurement. Equity prices also depend on earnings revisions, margins, balance-sheet risk, sector leadership, liquidity, positioning, and risk appetite.

Duration risk can also interact with stock-bond correlation. If both stocks and bonds are pressured by the same rise in required returns, their diversification behavior may look different than in a growth-scare environment where bond yields fall while equities weaken.

Related Concepts

Several nearby concepts help keep the interpretation clean. Bond duration explains the measurement behind fixed-income sensitivity. The discount rate explains the present-value mechanism. The risk-free rate gives one baseline input in required-return pricing. Equity risk premium helps separate rate sensitivity from compensation for equity-specific uncertainty.

For equity-market transmission, how bond yields affect stocks is the more direct route into valuation multiples, sector sensitivity, and the difference between yield moves caused by growth optimism and yield moves caused by inflation or policy pressure.

FAQ

What is duration risk?

Duration risk is the risk that a bond or rate-sensitive exposure changes in value when yields, interest rates, or required returns move. Higher duration generally means greater sensitivity to the same yield change.

Is duration risk the same as credit risk?

No. Duration risk is about sensitivity to yield or required-return changes. Credit risk is about the issuer’s ability to repay or the market’s required compensation for default and spread risk.

Are high duration bonds more risky?

High duration bonds are usually more sensitive to yield changes, but that does not mean they are always worse or always better. The risk depends on the rate move, curve shape, credit quality, liquidity, convexity and the broader market context.

Does duration risk forecast interest rates?

No. Duration risk estimates sensitivity if yields or required returns change. It does not predict whether yields will rise or fall.

Why does duration risk matter for equities?

Some equities can be sensitive to discount-rate changes because more of their value depends on future earnings expectations. This is a useful shorthand, but it is not the same as measuring bond duration.