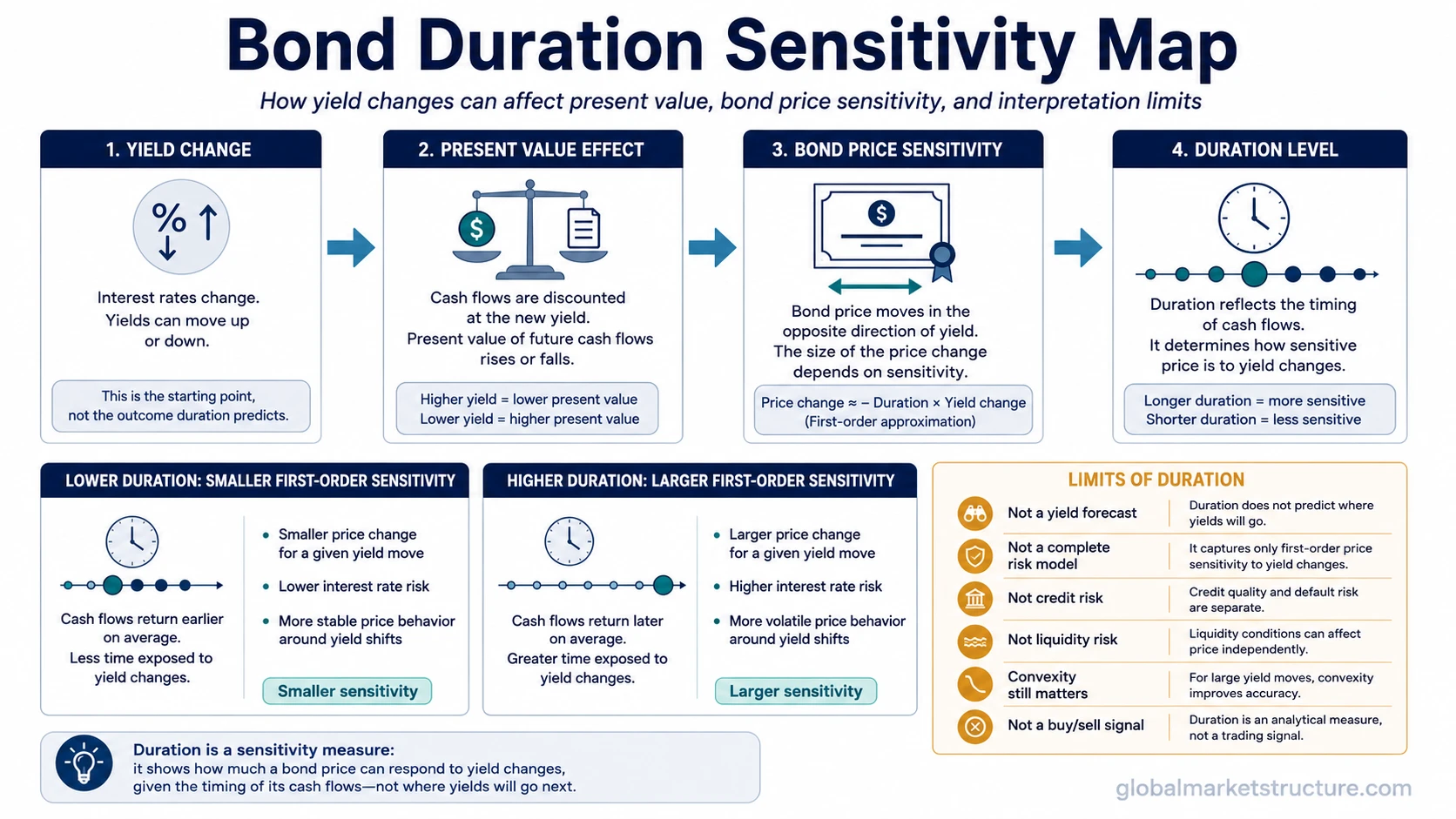

Bond duration is a fixed-income sensitivity measure. It estimates how much a bond’s price may respond when interest rates or yields change. It is related to the timing and present value of cash flows, but it is not the same as maturity. Higher duration generally means greater price sensitivity if yields move, but duration does not predict where yields will go and does not capture every bond risk.

Definition: Bond duration measures the sensitivity of a bond’s price to changes in yields or interest rates. In practical terms, it helps compare how strongly different bonds may react to the same yield move.

The key distinction is that duration is about sensitivity, not direction. A long-duration bond may be more exposed to a yield move than a short-duration bond, but duration by itself does not say whether yields should rise, fall, or remain stable.

Key Points

- Bond duration estimates price sensitivity to changes in yields or interest rates.

- Duration is related to cash-flow timing, but it is not the same as maturity.

- Modified duration is commonly used to approximate price change for a given yield move.

- Duration does not capture every risk, including credit risk, liquidity risk, convexity, curve-shape changes, or issuer-specific risk.

- For market-structure analysis, duration helps connect bonds, yields, discount rates, and broader rate-sensitive asset behavior.

What Bond Duration Is and Is Not

Duration is useful because it translates yield sensitivity into a more comparable measure. It is not a forecast, a full risk model, or a recommendation about which bonds to own.

| Bond duration is | Bond duration is not |

|---|---|

| A measure of bond price sensitivity to yield changes | A forecast of where yields will go |

| A cash-flow timing and present-value concept | The same thing as maturity |

| Useful for comparing rate sensitivity across bonds | A complete measure of bond risk |

| A way to interpret interest-rate exposure | A buy or sell signal |

| A useful input for market-structure interpretation | A substitute for credit, liquidity, convexity, or curve-shape analysis |

Why Duration Matters When Yields Move

Bond prices and yields generally move in opposite directions. When yields rise, the present value of a bond’s future cash flows usually falls. When yields fall, the present value of those cash flows usually rises.

Duration helps estimate the size of that response. A bond with higher duration is usually more sensitive to the same yield change because more of its value depends on cash flows received farther in the future. A bond with lower duration usually has less price sensitivity because more of its value is tied to nearer cash flows or higher coupon payments.

This matters for market interpretation because yield changes can transmit through the broader rate structure. When the risk-free rate changes, the discounting framework used across fixed income and other rate-sensitive assets can change as well.

Bond Duration vs Maturity

Maturity is the date when the bond’s principal is scheduled to be repaid. Duration is different. It reflects the weighted timing of the bond’s cash flows and the bond’s sensitivity to yield changes.

A bond can have a long maturity but a lower duration if it pays a high coupon, because more cash is received earlier. A zero-coupon bond usually has duration close to its maturity because the investor receives the cash flow at the end rather than through periodic coupons.

Maturity answers: when is principal scheduled to be repaid?

Duration answers: how sensitive is the bond’s price to changes in yields?

Macaulay Duration vs Modified Duration

Macaulay duration and modified duration are related, but they answer different questions. Macaulay duration focuses on the weighted average timing of cash flows. Modified duration translates that timing concept into an approximate price sensitivity measure.

| Duration type | Main purpose | How to read it |

|---|---|---|

| Macaulay duration | Measures weighted average cash-flow timing | Useful for understanding how far into the future the bond’s present value is concentrated |

| Modified duration | Approximates price sensitivity to yield changes | Useful for estimating how much a bond price may move for a change in yield |

Modified duration is often the more practical market-sensitivity measure. For example, a modified duration of 5 implies that a 1 percentage point rise in yield would be associated with an approximate 5% price decline, before considering convexity and other real-world factors.

What Affects Bond Duration

Duration is shaped by the timing, size, and discounting of a bond’s cash flows. The same maturity can produce different duration depending on coupon structure, yield level, and embedded features.

| Factor | Typical effect on duration | Reason |

|---|---|---|

| Longer maturity | Usually increases duration | More cash-flow value is tied to the future |

| Higher coupon | Usually lowers duration | More cash is received earlier |

| Lower coupon | Usually raises duration | More value depends on later principal repayment |

| Lower yield | Can increase duration | Distant cash flows become more important in present-value terms |

| Embedded options | Can change effective duration | Expected cash flows may change when rates move |

Simple Bond Duration Example

Suppose one bond has a modified duration of 2 and another has a modified duration of 8. If yields rise by 1 percentage point, the lower-duration bond would have an approximate 2% price decline, while the higher-duration bond would have an approximate 8% price decline, before convexity and other factors are considered.

Example: A higher-duration bond is not automatically better or worse. It simply has more price sensitivity to yield changes. Whether that sensitivity is desirable depends on the broader rate environment, credit quality, liquidity, portfolio role, and investor constraints.

This is why duration should be treated as an exposure measure. It helps describe how sensitive the bond is, but it does not tell the investor what should happen next.

Duration in Market-Structure Interpretation

For Global Market Structure, duration matters because it connects fixed-income pricing with the broader discount-rate environment. When yields move, duration helps explain why some bonds, sectors, and rate-sensitive assets may react more than others.

Duration also helps interpret why the same yield move can have different market effects. A rise in yields driven by stronger growth expectations may be read differently from a rise in yields driven by inflation pressure, policy tightening, or term-premium repricing.

This distinction is important when reading the discount rate channel across markets. Duration can help identify sensitivity, but the reason behind the yield move still matters for broader market interpretation.

Market-structure note: Duration is most useful when it is combined with yield-curve context, credit spreads, liquidity conditions, inflation expectations, and cross-asset confirmation. It is weakest when used as a standalone signal.

Duration is also relevant when reading how bonds interact with equities. A deeper explanation of the bond-equity channel belongs on the related page about how bond yields affect stocks.

What Duration Does Not Capture

Duration is a sensitivity measure, not a complete risk system. It can help estimate how price may respond to yield changes, but it leaves out several conditions that can dominate real market behavior.

Credit risk: Duration does not measure whether an issuer’s credit quality is improving or deteriorating.

Liquidity risk: Duration does not show whether the bond can be traded easily without large price impact.

Convexity: Duration is a linear approximation, while the bond price and yield relationship is curved.

Curve shape: A duration estimate can miss how different maturities move when the yield curve steepens, flattens, or twists.

Real vs nominal yield context: Duration does not explain whether the yield move is being driven by inflation expectations, real yields, policy expectations, or term premium.

Embedded options: Callable or option-sensitive bonds can behave differently because expected cash flows may change when rates move.

The practical mistake is treating duration as if it explains the whole bond. A duration estimate is most useful when it is paired with credit analysis, liquidity context, convexity, curve-shape awareness, and the reason yields are moving.

Related Concepts

Duration risk is the exposure created by duration sensitivity. Bond duration defines the sensitivity metric, while duration risk describes the market risk that appears when rates or yields move against that exposure.

FAQ

Is bond duration the same as maturity?

No. Maturity is the date when principal is scheduled to be repaid. Duration measures weighted cash-flow timing and price sensitivity to yield changes.

Does higher bond duration mean higher risk?

Higher duration usually means greater sensitivity to interest-rate or yield changes. It does not measure every risk, so credit quality, liquidity, convexity, curve shape, and issuer structure still matter.

Does bond duration predict where yields will go?

No. Duration estimates how sensitive a bond’s price may be if yields change. It does not forecast the direction of yields.

Why do long-duration bonds move more when yields change?

Long-duration bonds usually depend more on cash flows received farther in the future. Those distant cash flows are more sensitive to discount-rate changes, so price sensitivity is usually higher.