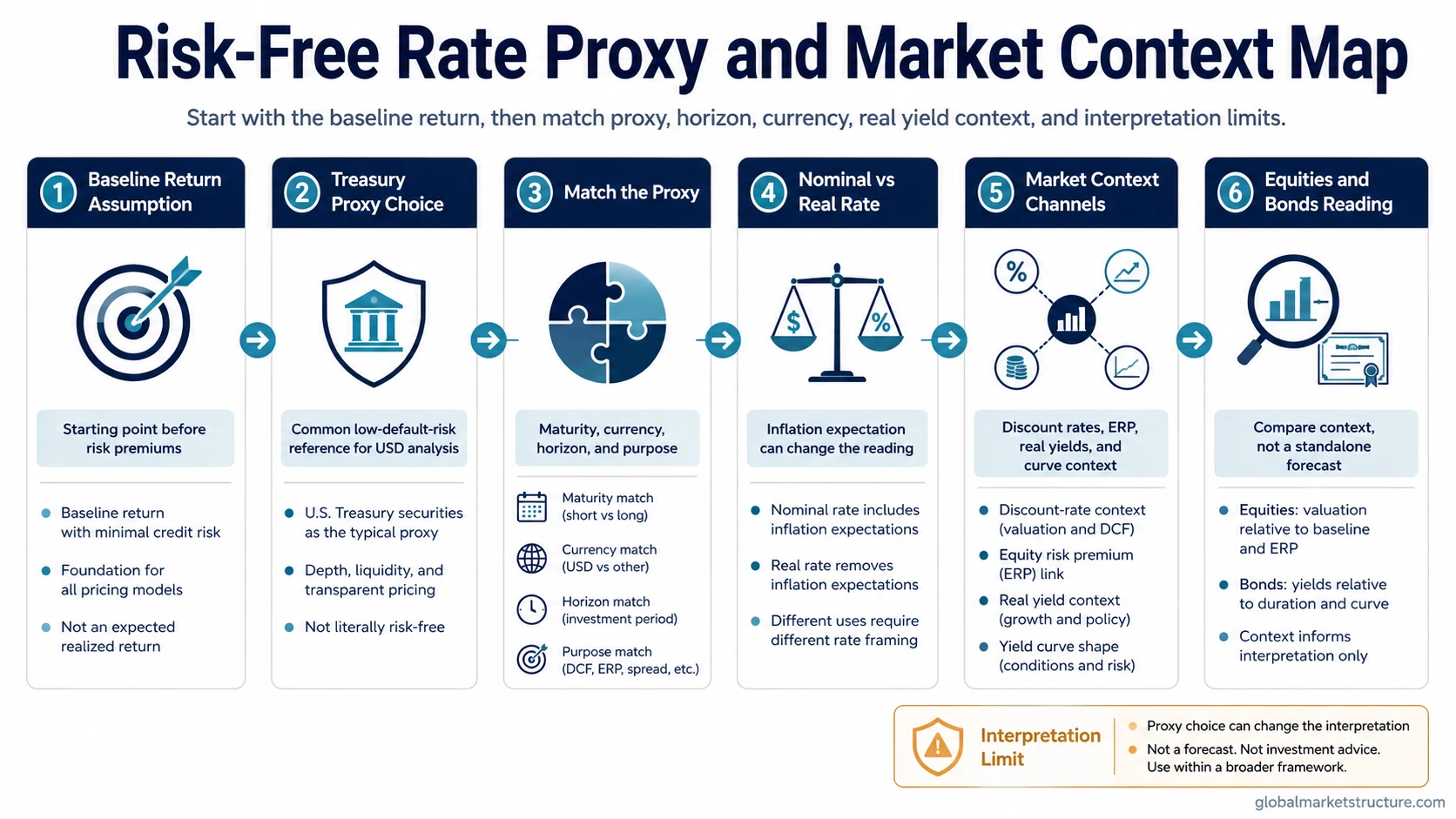

The risk-free rate is the baseline return assumption used to compare risky assets or discount future cash flows. In U.S. dollar markets, Treasury yields are commonly used as practical proxies, but “risk-free” does not mean free from inflation risk, duration risk, currency mismatch, liquidity conditions, or proxy selection errors.

Simple definition: the risk-free rate is the return assumption used as the starting point before adding risk premiums for assets that carry uncertainty.

Common proxy: U.S. Treasury yields are often used in U.S. dollar analysis because Treasuries are treated as very low default-risk instruments, but the chosen maturity must match the analysis.

Market-structure role: the risk-free rate helps connect bonds, equities, valuation pressure, real yields, and equity risk premium, but it is not a standalone forecast for stocks or bonds.

What the Risk-Free Rate Means

The risk-free rate is not a single permanent number. It is a baseline return used inside financial comparison. A risky asset must usually offer some reason to be held above that baseline, whether that reason is expected growth, income, diversification, or a higher required return.

In theory, the risk-free rate represents a return with no default risk over the chosen horizon. In practice, analysts usually use a high-quality government yield as a proxy. For U.S. dollar analysis, that usually means a Treasury yield, but the proxy should fit the currency, time horizon, and purpose of the analysis.

The Treasury yield is the proxy, not the concept itself. A short-term Treasury bill, a 10-year Treasury note, and an inflation-protected Treasury yield can all answer different questions.

Why Treasury Yields Are Commonly Used as Proxies

Treasury yields are commonly used because U.S. government debt is treated as a low default-risk reference point for U.S. dollar markets. That makes Treasury yields useful as a starting rate when comparing bonds, equities, and other risky assets.

The proxy still needs to match the job. A one-month cash comparison does not use the same horizon as a long-term equity valuation. A nominal cash-flow model does not ask the same question as a real-return analysis. A non-dollar asset may require a currency-consistent proxy instead of a U.S. Treasury rate.

| Use case | Common proxy logic | Main limitation |

|---|---|---|

| Short-term cash comparison | Short-dated Treasury bill yield can approximate a low default-risk cash baseline. | It may not represent long-term discount-rate pressure or duration sensitivity. |

| Longer-term equity or bond context | Intermediate or long Treasury yields may be used when the horizon is longer. | The proxy can mix expected policy rates, inflation expectations, growth expectations, and term premium. |

| Real-return analysis | Inflation-protected yields can help separate real yield from nominal yield. | Real yields still depend on market pricing and may not match every investor’s inflation experience. |

| Non-U.S. dollar analysis | A currency-matched government yield is usually more consistent than a U.S. Treasury proxy. | Currency risk can distort the comparison if the proxy and asset cash flows do not match. |

Risk-Free Does Not Mean Riskless in Every Sense

Default risk is only one part of the issue. A Treasury proxy may be treated as low default risk, but that does not remove inflation risk, reinvestment risk, currency mismatch, liquidity conditions, or price sensitivity from changing yields.

Duration still matters. A longer-maturity bond can lose market value when yields rise, even if the issuer is still expected to pay. That is why bond duration and duration risk matter when the risk-free proxy is a longer-term yield.

Current yield levels change over time. A Treasury yield proxy should be read with its date and maturity. Stale values can distort the comparison because the risk-free-rate proxy is time-sensitive.

Treasuries are not riskless in every practical sense. A Treasury yield can serve as a relatively low default-risk baseline for a specific currency and horizon.

Nominal vs Real Risk-Free Rate

A nominal risk-free rate includes inflation expectations inside the quoted yield. A real risk-free rate attempts to express the return after expected inflation. Market interpretation can change depending on whether yields are rising because real returns are rising, inflation expectations are rising, or both are moving together.

| Rate type | What it represents | Why it matters |

|---|---|---|

| Nominal risk-free proxy | A quoted government yield before adjusting for inflation. | Useful for nominal cash flows and broad market comparisons. |

| Real risk-free proxy | A yield measure intended to reflect return after expected inflation. | Useful for reading real yield pressure on valuation, duration, and risk appetite. |

| Inflation expectation gap | The difference between nominal and real yield interpretation. | Helps avoid treating every yield move as the same kind of market reading. |

How the Risk-Free Rate Connects to Equities and Bonds

The risk-free rate is one of the baseline inputs behind cross-asset comparison. It affects how investors compare safe yield, risky cash flows, bond prices, and expected compensation for uncertainty.

For equities, the risk-free rate connects to valuation through the required return. When the baseline return rises, future cash flows may face a higher hurdle. That does not automatically mean stocks must fall, because earnings expectations, growth, liquidity, risk appetite, and credit conditions may offset or amplify the pressure.

For bonds, the relationship is more direct but still not one-dimensional. A bond’s price sensitivity depends on maturity, coupon, and duration. A short bill and a long bond can respond very differently to the same change in the rate environment.

A cross-asset reading stays conditional. The risk-free rate is a baseline input, not a standalone market call. Its meaning becomes clearer when read beside real yields, yield-curve shape, credit spreads, liquidity conditions, and market breadth.

Risk-Free Rate vs Nearby Concepts

The risk-free rate is often mixed together with related terms. The cleanest way to avoid confusion is to separate the baseline rate from the broader return measures built on top of it.

| Concept | Core meaning | Common confusion |

|---|---|---|

| Risk-free rate | The baseline return assumption before adding risk compensation. | It is sometimes mistaken for a guarantee of no real-world risk. |

| Discount rate | A broader required-return measure used to discount future cash flows. | It may include the risk-free rate plus additional risk premiums. |

| Equity risk premium | The extra return investors require for holding equities above the baseline rate. | It is sometimes confused with the risk-free rate itself. |

| Duration risk | The sensitivity of a bond’s price to changes in yields. | It explains why low default-risk bonds can still have price risk. |

| Real yield | A yield measure after adjusting for expected inflation. | It can change the interpretation of whether yields are tightening financial conditions. |

A Practical Market-Structure Reading

A rise in the Treasury proxy can mean different things depending on why it is rising. If yields rise because growth expectations are improving, the equity interpretation may differ from a rise driven by inflation pressure, policy tightening, or term-premium repricing.

A useful reading separates four questions:

- Is the move mainly nominal or real?

- Is the maturity point short-term, intermediate, or long-term?

- Are credit spreads and liquidity confirming stress or staying calm?

- Are equities responding through valuation pressure, earnings resilience, breadth weakness, or sector rotation?

The risk-free rate becomes more useful when it is treated as a reference point inside the broader market structure. It becomes weaker when it is treated as a mechanical market call.

Common Mistakes When Reading the Risk-Free Rate

Mistake 1: treating the 10-year Treasury as always correct. The 10-year yield is widely watched, but the right proxy depends on the time horizon, currency, and purpose of the analysis.

Mistake 2: treating risk-free as free from inflation risk. A nominal Treasury yield can still leave the holder exposed to inflation if purchasing power changes.

Mistake 3: treating the rate as a stock-market prediction. A higher baseline return can pressure valuations, but equity outcomes also depend on earnings, liquidity, credit, positioning, and risk appetite.

Mistake 4: mixing the proxy with the concept. Treasury yields are practical proxies. The risk-free rate is the baseline assumption those proxies are used to estimate.

Related Concepts

The risk-free rate connects to several nearby concepts that should stay separate. The discount rate explains the broader required-return measure. Equity risk premium explains the additional compensation demanded for equity risk. Bond duration and duration risk explain why bond prices can remain sensitive even when default risk is low.

Keeping these concepts separate makes the intermarket reading cleaner: the risk-free rate sets the baseline, risk premiums add compensation for uncertainty, duration explains rate sensitivity, and market context determines whether the rate environment is tightening, easing, or simply repricing expectations.

FAQ

What is the risk-free rate?

The risk-free rate is the baseline return assumption used before adding compensation for risky assets. In practice, it is usually represented by a high-quality government yield that matches the currency and time horizon of the analysis.

What is commonly used as the risk-free rate?

In U.S. dollar markets, Treasury yields are commonly used as proxies. The correct maturity depends on the use case, so a short-term bill, an intermediate yield, or a longer Treasury yield may answer different questions.

Is the 10-year Treasury the risk-free rate?

The 10-year Treasury is a widely watched proxy, but it is not always the correct risk-free rate for every purpose. The proxy should match the horizon, currency, and cash-flow structure being analyzed.

Does risk-free mean there is no risk?

No. Risk-free usually refers to very low default risk in a model or comparison. It does not remove inflation risk, duration risk, currency mismatch, liquidity conditions, or proxy selection risk.

How does the risk-free rate affect stocks and bonds?

The risk-free rate affects stocks and bonds by changing the baseline return used for comparison. For stocks, it can influence valuation and equity risk premium. For bonds, it connects to yield levels and price sensitivity, especially through duration.