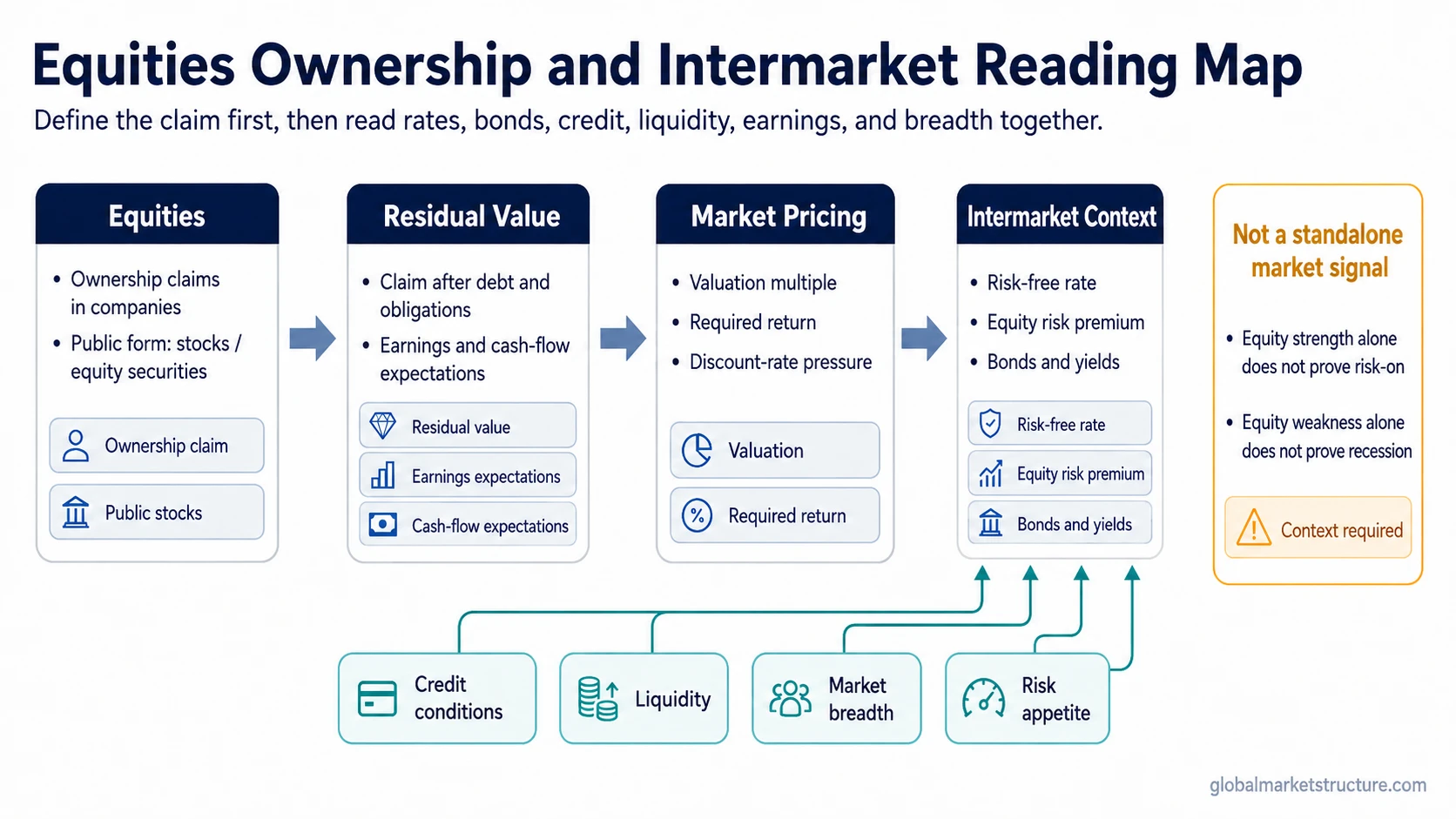

Equities are ownership claims in companies. In public markets, equities are usually represented by stocks, which give holders exposure to residual company value after debt and other obligations. For market-structure interpretation, equities are read with earnings expectations, rates, credit, liquidity, and risk appetite, not as a standalone market reading.

Equities in one view

- Ownership claim: equities represent ownership interests in a company.

- Public form: public equities are commonly represented by stocks traded in public markets.

- Different from bonds: bonds are debt claims, while equities sit on the ownership side of the capital structure.

- Market-structure role: equities are risk assets whose interpretation depends on earnings, rates, credit, liquidity, and risk appetite.

- Reading boundary: equity movement alone is not enough to define a market regime.

What equities mean

Equities mean ownership interests in a business. When a company issues equity, the equity holder owns a claim on residual value rather than a fixed promise of repayment. That residual claim can become more valuable if expected earnings, cash flows, and investor demand improve, but it can also lose value when expectations weaken or required returns rise.

In public markets, the word equities usually refers to stocks. A stock is the public-market form of an equity claim, while the broader term equity can also appear in accounting, private-company ownership, shareholder equity, or home equity. For market interpretation, the relevant scope is market-traded equity securities, not every possible use of the word equity.

Equities vs stocks vs bonds

Equities and stocks are closely related, but they are not always identical terms. Stocks are the most common public-market expression of equity ownership. Equities is the broader market category for ownership claims, especially when comparing them with debt instruments, rates, credit, and other asset classes.

The cleaner distinction is between equities and bonds. Equities are ownership claims with residual value exposure. Bonds are debt claims with contractual payment terms. That distinction matters because the bond market often gives a different reading of rates, credit risk, and liquidity conditions than equities alone.

| Concept | What it means | Why it matters in market structure | Common mistake |

|---|---|---|---|

| Equities | Ownership claims in companies | Used to read risk appetite, earnings expectations, valuation, liquidity, and equity risk premium context | Treating equity movement as a complete market regime reading |

| Stocks | Publicly traded shares of equity ownership | Used as the common public-market expression of equities | Assuming the word stock covers every form of equity ownership |

| Bonds | Debt claims with contractual payment terms | Used to read rates, credit conditions, duration pressure, and funding context | Comparing bonds with equities without separating debt claims from ownership claims |

| Risk-free rate | A baseline return reference for lower-risk assets | Helps frame the return investors require before accepting equity uncertainty | Reading equity valuation without checking the return available in safer assets |

| Equity risk premium | The extra return investors require for holding equity risk | Connects ownership uncertainty with required return, valuation, and risk appetite | Treating it as a fixed number instead of a context-dependent comparison |

A deeper comparison belongs in stocks vs bonds, where the ownership claim and debt claim distinction can be read side by side.

Why equities matter in market structure

Equities matter because they convert expectations about future company value into market prices. Those expectations are not only about earnings. Equity pricing also reflects the return investors require for holding uncertain ownership claims instead of safer or more senior claims.

The basic mechanism is: equity holders are exposed to residual earnings and cash flows, those expectations are translated into market prices, and those prices are influenced by valuation multiples, discount rates, liquidity, and risk appetite. When the required return rises, the same expected earnings can support a lower valuation. When liquidity is easier or risk appetite improves, investors may accept a lower required return, but that interpretation still depends on surrounding evidence.

The risk-free rate is one reference point in that process because it affects how investors compare equity risk with lower-risk alternatives. Equities usually require a premium over safer assets because equity cash flows are uncertain and sit below debt in the capital structure.

How equities fit into an intermarket reading

Equity markets are often treated as a quick read on confidence, but the stronger interpretation comes from comparison. Equity movement becomes more useful when it is read with bond yields, credit spreads, liquidity conditions, earnings expectations, market breadth, and the behavior of other risk assets.

| Input | What it can change | Why it matters for equities |

|---|---|---|

| Earnings expectations | Expected residual value | Equity holders are exposed to future company profits and cash-flow expectations. |

| Rates | Discount-rate pressure | Higher required returns can pressure valuations, while lower required returns can support higher multiples under the right conditions. |

| Credit conditions | Risk appetite and financing stress | Credit deterioration can weaken the quality of an equity rally if risk pricing is worsening beneath the surface. |

| Liquidity | Market capacity to absorb risk | Easier liquidity can support risk-taking, while tighter liquidity can make equity strength more fragile. |

| Market breadth | Participation quality | A narrow equity advance can mean something different from a broad advance across sectors and market-cap groups. |

Illustrative scenario: why equity strength can mislead

A common scenario is that a major equity index rises while the underlying message is mixed. The move can come from stronger earnings expectations, easier liquidity, multiple expansion, nominal repricing, or concentration in a small group of large companies. Without checking bonds, credit, breadth, and liquidity, the equity move may look cleaner than the broader market structure actually is.

The same logic works in reverse. Equity weakness does not automatically prove recession risk, policy stress, or a full risk-off regime. It may reflect valuation compression, rate pressure, sector concentration, earnings uncertainty, or temporary positioning. The useful reading comes from the combination of signals, not from equities alone.

What equities do not tell you by themselves

Equities are important, but they are not a complete market reading. A strong equity market does not automatically prove that the economy is strong. A weak equity market does not automatically prove that recession risk is confirmed. Equity behavior can reflect changes in earnings expectations, discount rates, liquidity, credit stress, sector leadership, valuation, and investor positioning.

- Equity strength alone does not define a risk-on regime.

- Equity weakness alone does not define a recession regime.

- Higher bond yields do not always hurt equities in the same way.

- Lower bond yields do not always support equities for the same reason.

- Equities should be read with rates, credit, liquidity, breadth, and bond behavior.

FAQ

Are equities the same as stocks?

In public-market usage, equities are often represented by stocks. Stocks are the common traded form of public equity ownership, while equity is the broader ownership concept.

How are equities different from bonds?

Equities are ownership claims on residual company value. Bonds are debt claims with contractual payment terms. Equity holders usually take more uncertainty, while bondholders have a defined claim structure.

Does equity strength mean the economy is strong?

Not necessarily. Equity strength can reflect earnings expectations, liquidity, valuation multiples, sector concentration, or investor positioning. It should not be treated as a standalone reading of the economy or market regime.