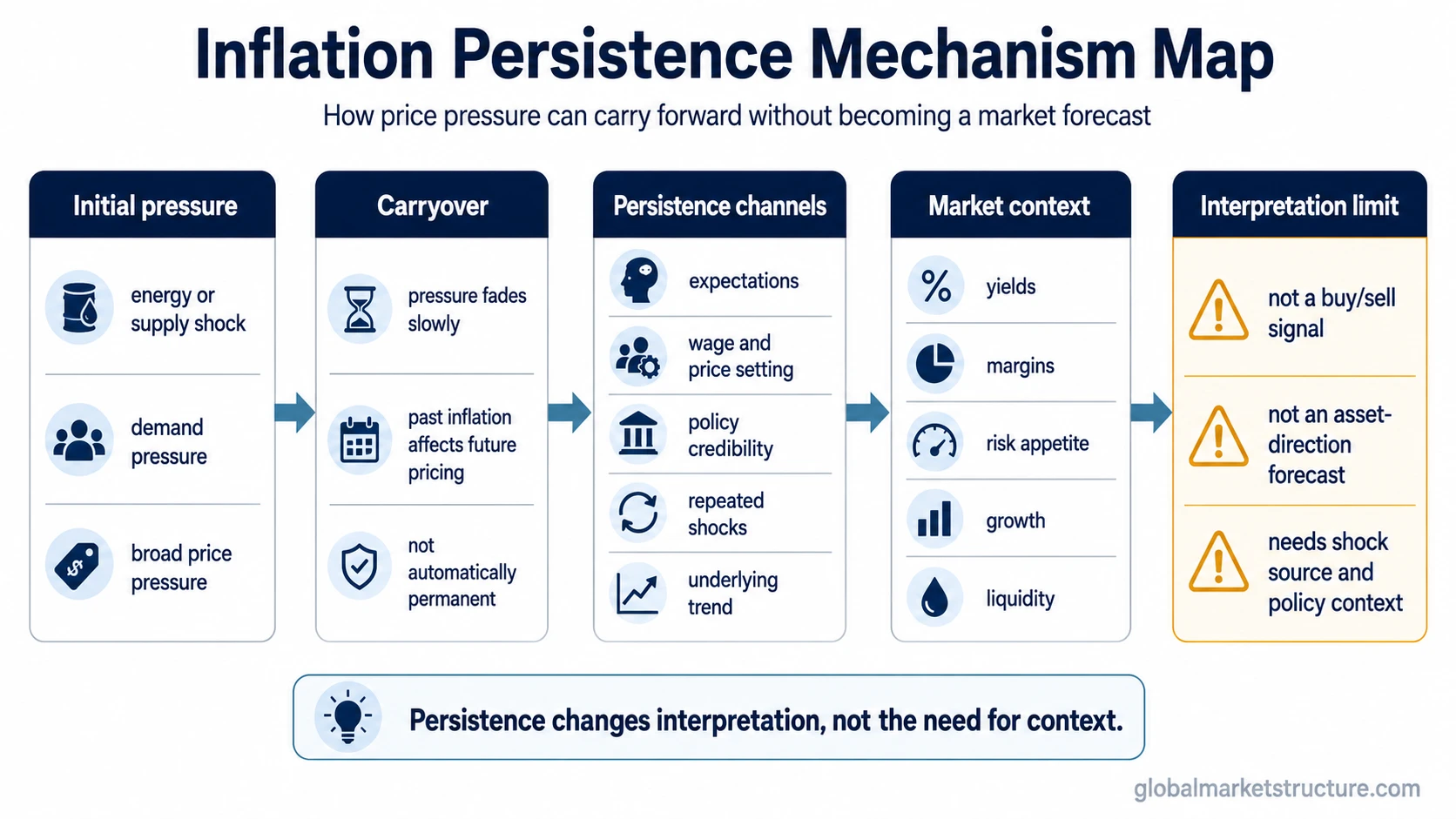

Inflation persistence describes how much current inflation pressure carries into future periods instead of fading quickly after a shock. Inside broader inflation dynamics, it helps explain why expectations, central-bank response, yields, margins, and risk appetite may stay sensitive after the first price shock is visible. It does not mean inflation stays high permanently, and it does not forecast asset direction by itself.

What inflation persistence does and does not mean

Inflation persistence is about durability, not just level. A high inflation reading can be temporary if the pressure fades quickly. A lower inflation reading can still matter if the underlying pressure carries forward through expectations, wage setting, pricing behavior, or repeated shocks.

| Not this | Instead this |

|---|---|

| Persistence means inflation is permanently high. | Persistence means inflation pressure fades more slowly than expected. |

| Persistence equals sticky inflation. | Sticky components can contribute to persistence, but they are not the whole concept. |

| Persistence is a market signal. | Persistence is an interpretation input that still needs growth, liquidity, policy, and shock context. |

| Persistence automatically forces one policy path. | The policy path depends on mandate, expectations, growth, credibility, and the source of inflation pressure. |

Why persistence matters inside inflation dynamics

Persistence changes how inflation data is interpreted. If inflation pressure is likely to fade quickly, policy makers and markets may treat the shock differently than if the pressure keeps feeding into future prices. The same headline inflation rate can carry different meaning depending on whether it reflects a fading one-time shock or a slower-moving process.

For market-structure interpretation, persistence can affect the way investors read inflation expectations, rate-path sensitivity, nominal yields, real yields, corporate margins, and risk appetite. The connection is conditional. Persistent inflation can tighten the interpretation of the macro backdrop, but it does not automatically define the direction of stocks, bonds, commodities, or currencies.

Main channels behind inflation persistence

Inflation can become more persistent through several channels. These channels often overlap, which is why persistence should not be reduced to one simple cause.

- Lagged inflation: past inflation can influence future price and wage decisions when firms and households use recent experience as a reference point.

- Expectations: inflation can become harder to slow if households, firms, or markets begin to expect higher future inflation.

- Policy credibility: confidence in the central-bank response can influence whether temporary shocks stay contained or become more durable.

- Persistent shocks: repeated supply, energy, labor, or currency pressures can keep inflation pressure alive after the initial shock.

- Underlying trend: broad price pressure can matter more than a narrow category spike if many components keep rising together.

- Wage and price-setting behavior: contracts, pricing cycles, and compensation adjustments can slow the return toward lower inflation.

The practical distinction is between a shock that passes through the system and a shock that changes behavior. Inflation persistence becomes more important when price-setting, wage-setting, expectations, or policy tradeoffs start carrying the pressure forward.

Condition, implication, and limitation

The persistence label becomes more useful when it is tied to conditions. The same durability in inflation pressure can imply different risks depending on expectations, growth, liquidity, the policy response, and the original source of the shock.

| Condition | Possible implication | Limitation |

|---|---|---|

| Persistent inflation with anchored expectations | Inflation may fade more slowly while remaining more policy-manageable. | Current data and policy context are still required. |

| Persistent inflation with weakening growth | Policy tradeoff risk may rise because inflation pressure and growth risk can conflict. | This does not automatically imply recession, equity decline, or bond rally. |

| Persistent inflation with weak perceived policy response | Expectations may become more sensitive to each new inflation reading. | Credibility and expectations claims need survey, market, or institutional evidence. |

| Persistence after a temporary shock | Headline pressure can stay elevated longer than a one-month data point suggests. | The source of pressure still matters because some shocks fade without changing the trend. |

How persistent inflation can be misread

A common false reading is to treat persistent inflation as a direct forecast for markets. Persistent inflation with weakening growth and tighter financial conditions can carry a different interpretation than persistent inflation with strong nominal demand and anchored expectations. The first mix may raise policy tradeoff risk. The second may suggest stronger demand pressure. Neither case gives a standalone asset-direction answer without growth, liquidity, central-bank response, earnings sensitivity, and shock-source context.

Persistence should be read as a diagnostic layer. It helps classify how inflation pressure is behaving, but it does not replace the rest of the macro framework. The market impact depends on what is driving the persistence and how other parts of the system respond.

Difference from nearby concepts

Inflation persistence often gets confused with adjacent concepts. The distinctions matter because each concept answers a different question.

- Inflation: the broader concept describes the rise in the general price level. Persistence asks whether that pressure carries forward or fades quickly.

- Inflation expectations: expectations are one channel that can make inflation more persistent, but they are not the same as persistence itself.

- Sticky inflation: sticky categories or slow-moving prices can contribute to persistence, but persistence can also come from expectations, shocks, trend behavior, or policy credibility.

- Disinflation: disinflation means inflation is slowing. Persistence asks whether the remaining pressure is fading quickly or slowly.

- Inflation dynamics: the broader framework includes direction, expectations, persistence, sticky components, policy reaction, and market transmission.

Interpretive boundary

Inflation persistence is most useful when it prevents oversimplified readings. It can show that inflation pressure is not fading as quickly as a single data release might imply. It can also show why policy makers, bond markets, and risk assets may remain sensitive to the inflation path.

The useful question is not whether persistence is good or bad for markets, but what is keeping inflation pressure alive and which parts of the macro system are absorbing it.

The boundary is just as important as the definition. Persistence is an input into macro interpretation, not a complete forecast. It needs to be combined with the source of inflation pressure, growth conditions, expectations, liquidity, policy response, and market positioning before any broader market conclusion is defensible.

FAQ

Does inflation persistence mean inflation stays high forever?

No. Persistence means inflation pressure fades more slowly. It does not mean inflation is permanent, and it does not prove that high inflation will continue indefinitely.

How is inflation persistence different from sticky inflation?

Sticky inflation usually refers to price categories or components that adjust slowly. Inflation persistence is broader because it can also reflect expectations, lagged inflation, policy credibility, repeated shocks, and wage or price-setting behavior.

Does inflation persistence predict stocks or bonds?

No. Inflation persistence can affect how markets interpret yields, margins, policy reaction, and risk appetite, but it does not predict asset direction by itself. Growth, liquidity, expectations, policy response, and positioning still matter.