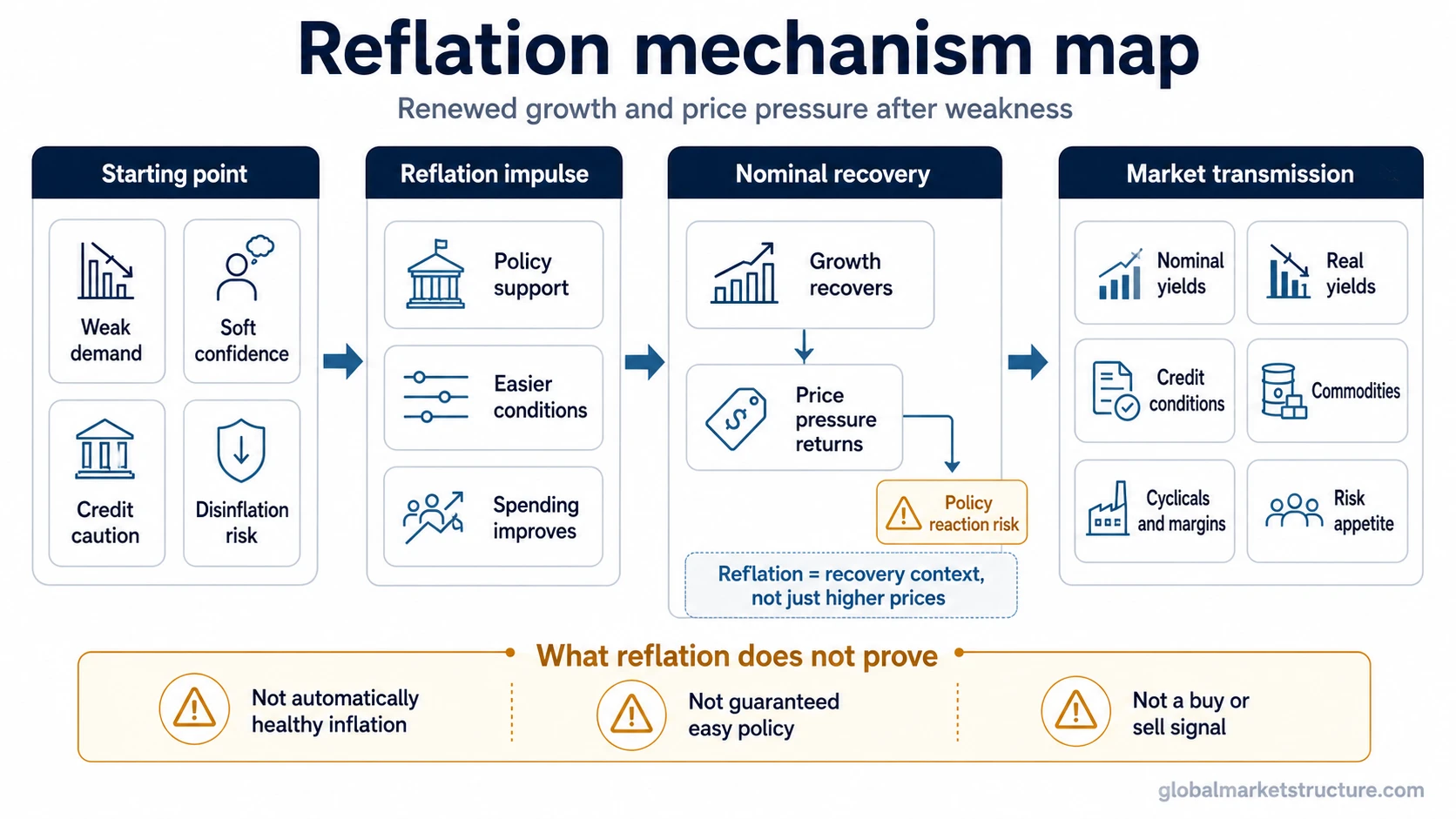

Reflation is a macro condition where economic activity and inflation pressure recover after weakness, slowdown, or deflation risk. It usually reflects a mix of stronger demand, easier financial conditions, policy support, and improving nominal growth. Reflation is not the same as ordinary inflation, and it is not a standalone signal that markets must rise.

Reflation means renewed growth plus renewed price pressure after a weak or disinflationary period. The term is most useful when it describes a shift in the macro environment, not just a single inflation reading or one strong market move.

- It usually follows weak demand, slowing inflation, or deflation pressure.

- It can appear when policy support, easier financial conditions, or improving confidence revive nominal activity.

- It can affect yields, credit, commodities, cyclicals, margins, and risk appetite.

- It does not prove that inflation is healthy, that policy will stay easy, or that a reflation trade will work.

What reflation means

Reflation describes a recovery in nominal economic activity after a period of weakness. The key feature is the combination of improving growth and rising inflation pressure. That makes it different from a simple price increase, because the concept is tied to a change in the economic cycle.

A reflationary environment often begins when demand has been weak, financial conditions have been restrictive, confidence has been low, or price pressure has been fading. If policy support, credit availability, income growth, or private demand improves, the economy can move away from deflation risk and toward stronger nominal growth.

The market meaning depends on context. Reflation can look constructive when it reflects a healthier recovery from weakness. It can become more difficult for markets if inflation pressure rises faster than real growth, if central banks respond by tightening policy, or if higher real yields offset the benefit of stronger nominal activity.

How reflation develops

Reflation usually develops through a sequence rather than one isolated event. The sequence often starts with weak demand, falling confidence, credit caution, disinflation, or concern that prices could decline more broadly. Policy support or easier financial conditions may then help demand recover.

As activity improves, companies may see better revenue conditions, households may spend more confidently, and commodity demand may strengthen. At the same time, inflation pressure and inflation expectations can rise if markets believe the recovery will persist.

| Stage | What changes | Why it matters |

|---|---|---|

| Prior weakness | Demand, confidence, or price pressure has been soft. | Reflation is usually measured against a weak starting point. |

| Support or easing | Policy, credit, liquidity, or financial conditions become less restrictive. | The recovery impulse can start before inflation pressure is fully visible. |

| Demand recovery | Spending, production, or risk appetite improves. | Nominal growth begins to recover. |

| Inflation pressure returns | Prices, wages, commodities, or expectations may firm. | The environment becomes reflationary rather than simply weak-but-stable. |

| Policy reaction risk | Central banks may tolerate, question, or lean against the move. | The same reflation impulse can have different market effects depending on real yields and policy expectations. |

Reflation vs inflation, disinflation, deflation, and stagflation

Reflation is easiest to understand by separating it from nearby inflation-dynamics terms. The difference is not only whether prices are rising or falling. The difference is the economic setting around the price trend.

| Concept | Core meaning | How it differs from reflation |

|---|---|---|

| Reflation | Growth and inflation pressure recover after weakness. | It is a recovery-linked condition, not just a price-level trend. |

| Inflation | Broad prices rise over time. | Inflation can occur with strong growth, weak growth, or overheating; reflation specifically follows weakness. |

| Disinflation | Inflation is still positive but slowing. | Disinflation points to slower price increases; reflation points to renewed nominal momentum. |

| Deflation | Broad price levels decline persistently. | Reflation can be a move away from deflation pressure, but it does not prove deflation risk is permanently gone. |

| Stagflation | Inflation pressure persists while growth is weak. | Reflation combines improving growth with rising price pressure; stagflation combines weak growth with inflation pressure. |

The most common mistake is treating any rise in inflation as reflation. A price increase caused by supply stress, margin compression, or currency weakness may be inflationary without being reflationary. Reflation requires some recovery element in demand, activity, or nominal growth.

How reflation can affect markets

Reflation can affect markets through several channels at once. The first channel is nominal growth. If revenues, wages, and demand improve from a weak base, cyclical earnings expectations may improve and risk appetite may recover.

The second channel is rates. Nominal yields may rise if investors expect stronger growth, higher inflation, or a different policy path. The market effect depends partly on whether real yields rise as well. A reflationary move supported by improving growth can be interpreted differently from one where higher real yields tighten financial conditions.

The third channel is credit and risk appetite. If credit spreads narrow, lending conditions improve, and market breadth strengthens, reflation may be read as a healthier recovery impulse. If credit spreads widen while inflation pressure rises, the same environment may look less benign.

The fourth channel is commodities and cyclical sectors. Reflation can support demand-sensitive areas, but it does not guarantee that commodities, banks, industrials, or other cyclicals will outperform. Positioning, valuation, margins, policy reaction, and the level of real yields can all change the outcome.

What reflation does not prove

Reflation is a macro condition, not a market instruction. It can help classify the environment, but it should not be treated as a direct asset-allocation signal or as a guaranteed reflation trade.

- It does not prove that growth is durable.

- It does not prove that inflation will stay controlled.

- It does not prove that central banks will keep policy easy.

- It does not prove that real yields will fall.

- It does not prove that commodities, banks, or cyclical sectors must outperform.

- It does not turn every recovery rally into a reflation trade.

The policy reaction is often the key limitation. If reflation is seen as normalization after weakness, markets may focus on improving activity. If it is seen as inflation becoming persistent, markets may focus on tighter policy, higher real yields, and pressure on risk assets.

Example of a reflationary setup

A simple reflationary setup could begin after a weak period when demand has slowed, inflation pressure has faded, and credit conditions are cautious. If policy becomes more supportive, financing conditions improve, and households or companies start spending again, nominal growth can recover. Inflation expectations may firm, yields may rise, and demand-sensitive sectors may improve.

The same setup can still be misread. If yields rise mainly because real rates are tightening, or if inflation pressure rises faster than earnings and margins, the market effect can become less supportive. The useful point is not that reflation creates one outcome, but that it changes which signals need to be watched together.

FAQ

Is reflation the same as inflation?

No. Inflation means broad prices are rising over time. Reflation refers to renewed growth and inflation pressure after weakness, slowdown, or deflation risk. It is tied to recovery context, not only to prices rising.

Is reflation the opposite of deflation?

Reflation can be a move away from deflation pressure, but it is not simply the opposite of deflation. Deflation describes broad price-level decline. Reflation describes a recovery in nominal activity and price pressure after weakness.

Does reflation mean markets should rise?

No. Reflation can support risk appetite when growth improves and financial conditions remain manageable, but it can also pressure markets if inflation expectations, real yields, or policy tightening risks rise too far.

What is the difference between reflation and a reflation trade?

Reflation is the macro condition. A reflation trade is a market expression based on expectations about which assets may benefit from that condition. The trade can fail even if the macro reflation impulse is real.