Credit spreads widening means the yield premium demanded on riskier corporate credit is increasing relative to safer benchmark bonds. In bond-market interpretation, wider spreads can point to higher perceived credit risk, weaker risk appetite, tighter liquidity, or broader financial-condition pressure. The move does not, by itself, confirm recession, stock-market weakness, or a trading signal.

Here, credit spreads refers to bond-market credit spreads, not options credit spread strategies. The focus is the extra yield investors demand for holding corporate credit instead of safer benchmark debt.

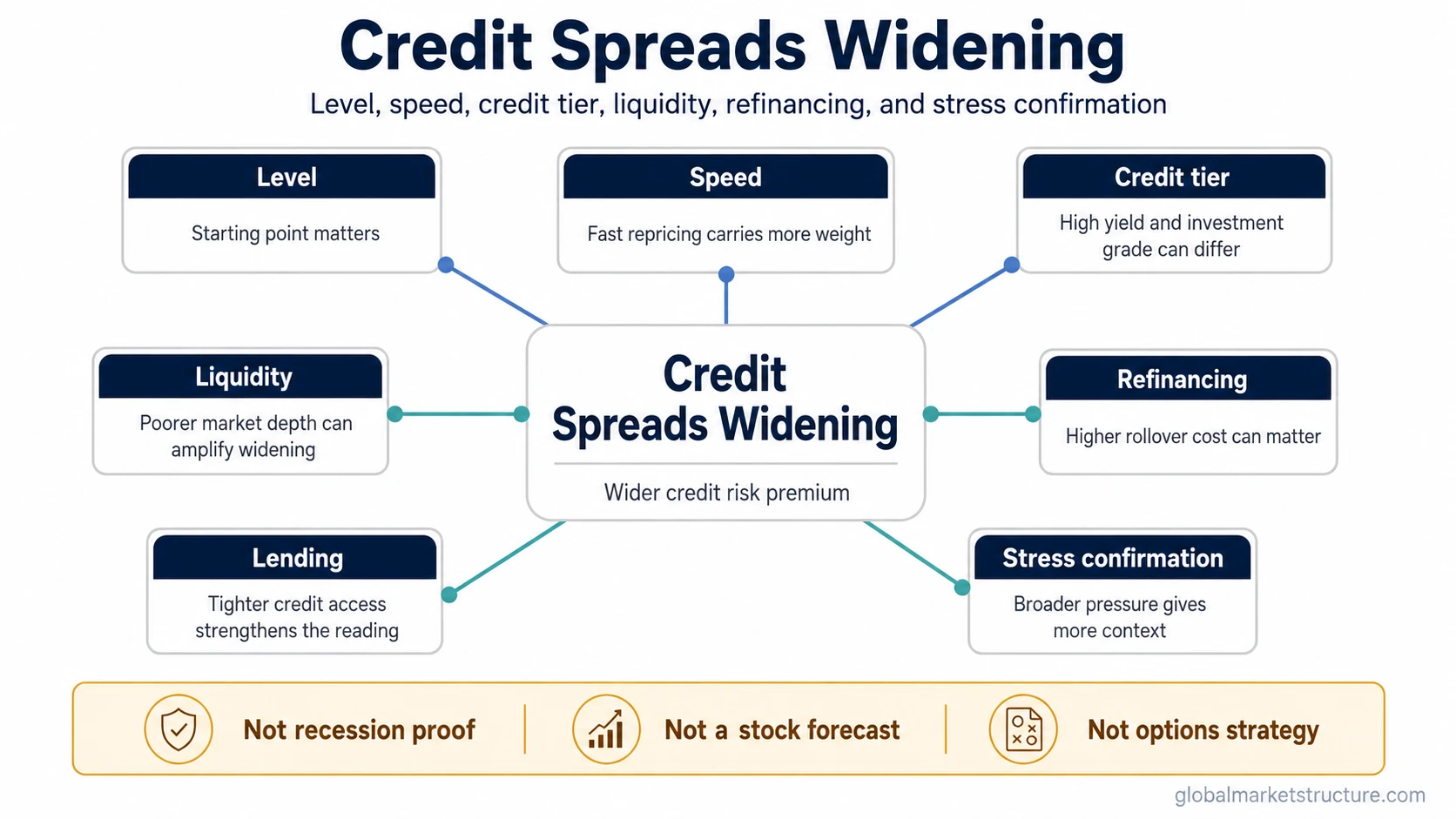

Key Points

- Widening credit spreads mean riskier borrowers are being priced with a larger yield premium.

- The move can reflect default concern, weaker liquidity, lower risk appetite, or refinancing pressure.

- The signal becomes stronger when widening is fast, broad, and confirmed by other financial-condition indicators.

- Widening alone is a pressure input, not a complete macro or market conclusion.

What Credit Spreads Widening Means

A credit spread is the extra yield investors require to hold a riskier bond instead of a safer benchmark with a similar maturity profile. When spreads widen, that extra yield increases. The market is demanding more compensation for credit risk, liquidity risk, or uncertainty around the borrower’s ability to refinance and repay.

The broader concept of credit spreads covers the full relationship between corporate bond yields and safer benchmark yields. Credit spreads widening is narrower: it describes the direction of change and what that change may imply.

For market-structure analysis, the direction matters because widening spreads can show that credit investors are becoming less willing to accept low compensation for risk. That can happen before broader risk conditions become obvious in equity indexes, but it can also happen during ordinary repricing from unusually tight levels.

Why Credit Spreads Widen

Credit spreads can widen when investors become more concerned about default risk. If borrowers look less able to service debt, or if the economic backdrop becomes less supportive, investors usually demand more yield before holding that credit exposure.

Spreads can also widen when risk appetite weakens. Investors may prefer safer assets, reduce exposure to lower-quality credit, or demand more compensation for uncertainty. In that setting, the spread move is partly about credit risk and partly about the broader willingness to hold risk.

Liquidity can amplify the move. If corporate bonds become harder to trade, or if dealers and investors become less willing to warehouse risk, buyers may require wider spreads to compensate for poorer market depth.

Refinancing pressure can matter as well. When borrowers must roll debt at higher rates or in less receptive markets, refinancing risk can become part of the spread-widening story.

Sector-specific stress can widen spreads in one part of the credit market without creating a broad systemic signal. A move concentrated in one industry does not carry the same meaning as widening that appears across credit tiers, maturities, and borrower types.

What Changes the Interpretation

The first question is not only whether spreads widened. The more useful question is what widened, from what level, how quickly, and with what confirmation.

Widening from very tight levels may show that risk pricing is becoming less complacent, but the absolute spread level can still be moderate. A small move from already-stressed levels can be more important than a larger move from unusually calm conditions.

Speed matters because fast widening can signal forced repricing, weaker liquidity, or a sudden shift in risk appetite. Slow widening may still matter, but it often requires more confirmation from lending, funding, volatility, and broader financial-condition measures.

Credit tier also matters. High-yield spreads usually carry more sensitivity to default risk and risk appetite than higher-quality credit. Investment-grade spreads can still widen during stress, but the interpretation may involve duration, liquidity, rate volatility, or balance-sheet repricing as well as default concern.

Confirmation is the difference between a single market move and a broader tightening signal. A widening move becomes more serious when it appears alongside weaker lending conditions, rising funding pressure, falling market depth, or deterioration in a financial stress index.

Condition, Implication, and Limitation

| Condition | What widening may imply | Limitation |

|---|---|---|

| Widening from very tight levels | Risk pricing is becoming less complacent | The absolute level may still be moderate |

| Fast widening across high-yield credit | Risk appetite and credit liquidity may be weakening | Sector-specific stress can exaggerate the signal |

| Widening in investment-grade spreads | Higher-quality borrowers are being repriced | The move may reflect rates, liquidity, or duration effects |

| Widening with weaker lending standards | Financial conditions may be tightening more broadly | Other indicators still need to confirm the pressure |

| Widening with refinancing pressure | Borrowers may face higher rollover costs | Maturity schedules and issuer quality change the risk |

When Widening Can Be Misleading

Credit spread widening can look alarming when the percentage move is large, but the starting point matters. A move from unusually tight spreads can represent a return toward more normal risk compensation rather than a crisis signal.

A common false alarm occurs when spreads widen from very calm levels while the absolute spread level remains moderate. The change deserves attention because investors are demanding more compensation for credit risk, but it does not prove that defaults, recession, or broad market stress are imminent.

The signal weakens when widening is narrow, slow, or concentrated in one sector. It strengthens when the move is broad across lower-quality and higher-quality credit, appears quickly, and is confirmed by weaker liquidity, tighter lending, or broader financial stress measures.

What Widening Spreads Do Not Prove

Widening credit spreads do not prove recession. They can reflect rising credit concern, but recessions depend on a wider set of growth, employment, lending, income, production, and policy conditions.

Widening spreads do not prove that stocks must fall. Equity-market behavior also depends on earnings expectations, valuation, liquidity, positioning, rates, leadership, and market breadth.

Widening spreads are a credit-market pressure input, not a complete macro conclusion. The reading becomes more useful when liquidity, lending, funding, volatility, and broader financial-condition evidence point in the same direction.

How Widening Fits Inside Financial Conditions

Credit spreads are one part of the financial-conditions picture. Wider spreads can raise borrowing costs, reduce investor willingness to fund riskier borrowers, and make refinancing more difficult. That can tighten conditions even if policy rates or equity prices have not moved much.

A financial conditions index can include credit spreads alongside other variables such as rates, equity prices, volatility, currency pressure, and funding conditions. The spread move gains meaning when those other components point in the same direction.

The cleanest interpretation separates observed fact from inference. The observed fact is that the yield premium has widened. The inference may be weaker risk appetite, higher perceived credit risk, poorer liquidity, or tighter financial conditions. The inference becomes more reliable only when surrounding evidence supports it.

Related Credit-Market Concepts

Credit spreads define the broader benchmark relationship behind the widening condition.

Financial stress measures become more useful when credit widening appears alongside funding, volatility, or liquidity pressure.

Credit-tier interpretation can be separated through high-yield spreads and investment-grade spreads, because lower-quality and higher-quality borrowers can reprice for different reasons.

FAQ

Does widening credit spreads mean a recession is coming?

No. Widening credit spreads can show higher perceived credit risk or weaker risk appetite, but recession requires confirmation from broader economic and financial conditions.

Are widening credit spreads bad for stocks?

They can be a negative risk-condition input, but they do not automatically mean stocks will fall. Equity interpretation also depends on earnings, rates, liquidity, valuation, positioning, and market breadth.