Refinancing risk is the risk that a borrower may be unable to roll over, replace, or refinance existing debt on acceptable terms when funding is needed. It is a credit and funding-pressure concept inside broader financial conditions. The risk becomes more important when higher rates, tighter credit access, wider spreads, stricter lender standards, or weaker borrower credit quality make replacement financing more expensive or unavailable.

Refinancing risk in one line: maturing debt creates pressure when replacement funding becomes costly, restricted, or unavailable.

Where it sits: refinancing risk belongs to credit conditions, funding access, borrower balance-sheet pressure, and the transmission of tighter financial conditions.

What it does not prove: refinancing risk is not a recession forecast, equity-direction signal, market-timing tool, consumer mortgage-refinance guide, or instruction to refinance, invest, hedge, buy, sell, or trade.

Key Points

- Refinancing risk is about replacing or rolling over debt on acceptable terms.

- The risk rises when funding costs increase, credit access weakens, or lenders demand stricter terms.

- It can transmit into broader credit conditions through borrower pressure and lender behavior.

- It should not be treated as a recession forecast, equity signal, or trading signal.

What Refinancing Risk Means

Refinancing risk appears when a borrower has debt coming due and needs new funding to repay, replace, or roll over the existing obligation. The risk is not simply that debt exists. The risk is that the next round of financing may come with higher costs, tighter covenants, shorter maturities, more collateral demands, or no acceptable lender support.

Rollover risk is closely related. Both ideas focus on the problem of replacing maturing obligations. Refinancing risk usually emphasizes the broader funding decision: whether a borrower can obtain replacement financing, on what terms, and with what effect on cash flow and balance-sheet flexibility.

The concept can apply to companies, financial institutions, governments, and other borrowers that depend on ongoing market access. It becomes more visible when debt maturities meet a less forgiving funding environment.

How Refinancing Risk Works

Refinancing risk works through a sequence of funding pressure. A borrower reaches a maturity date or a refinancing window. The borrower then faces the current market price of credit, the willingness of lenders to extend funding, and the borrower’s own credit profile at that moment.

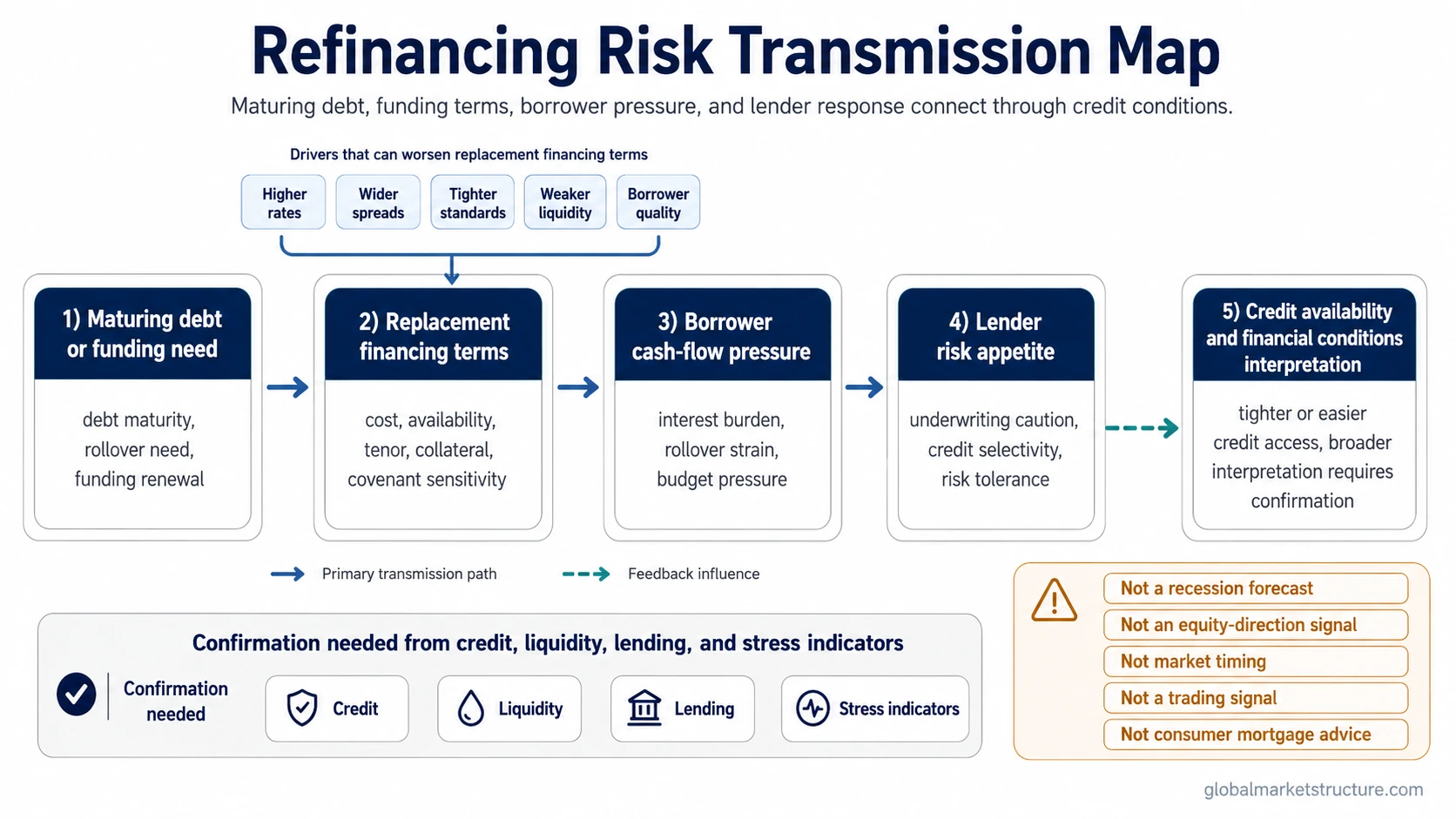

Refinancing risk transmission map:

- Maturing debt or funding need creates a replacement-financing requirement.

- Rates, spreads, lender standards, liquidity, and borrower quality shape available terms.

- Higher costs or weaker access reduce borrower flexibility.

- Cash-flow pressure, collateral demands, or balance-sheet stress can increase.

- Lenders may respond with stricter standards, wider risk premiums, or reduced credit availability.

- Broader market interpretation depends on confirmation from credit, liquidity, lending, and financial-stress signals.

The important distinction is that refinancing risk is conditional. A borrower can have maturing debt without immediate stress if credit access remains strong and terms remain manageable. The same maturity profile can become more difficult when funding costs rise, market liquidity weakens, or lenders become more selective.

What Increases Refinancing Risk?

Refinancing risk usually increases when debt maturities coincide with less favorable funding conditions. No single driver is enough on its own. The risk becomes more meaningful when several pressures reinforce each other.

| Driver | How it affects refinancing risk | Interpretation limit |

|---|---|---|

| Higher interest rates | Replacement debt may carry a higher coupon or higher total financing cost. | Higher rates do not automatically mean refinancing becomes unavailable. |

| Wider credit spreads | Credit spreads can raise the extra compensation lenders demand for credit risk. | Spread widening needs context from borrower quality, liquidity, and market stress. |

| Tighter lending standards | Bank lending standards can reduce access to credit or require stricter loan terms. | Lending standards are one channel, not the whole credit environment. |

| Weaker borrower credit quality | Lower cash-flow coverage, higher leverage, or weaker collateral can make refinancing less attractive to lenders. | Borrower weakness does not always lead to default if funding options remain open. |

| Weaker liquidity conditions | Reduced market depth or funding availability can make debt placement harder or more expensive. | Liquidity pressure needs confirmation from market and funding indicators. |

| Maturity concentration | Large amounts of debt coming due around the same window can increase sensitivity to funding conditions. | Specific maturity-wall claims require dated evidence before publication. |

| Broader financial stress | A stressed market can reduce lender risk appetite and make refinancing windows less reliable. | Financial stress index signals are separate indicators, not refinancing-risk measures by themselves. |

Refinancing Risk and Financial Conditions

Refinancing risk is one pressure channel inside broader financial conditions. It helps explain how the cost and availability of replacement funding can move from individual borrowers into wider credit behavior.

When refinancing becomes more expensive, borrowers may have less flexibility after interest expense, covenant pressure, or collateral requirements increase. When refinancing becomes harder to access, lenders may become more selective, credit availability may tighten, and risk premiums may rise. Those effects can contribute to tighter financial conditions, but they do not define the entire financial environment.

Broader interpretation requires confirmation. Refinancing pressure is more meaningful when it appears alongside tighter lending standards, wider credit spreads, weaker liquidity, or rising financial stress. Without that surrounding evidence, refinancing risk remains a funding-pressure concept rather than a complete market-regime signal.

Refinancing Risk Is Not the Same as Nearby Concepts

Refinancing risk is a funding replacement risk, not a complete macro signal. It can help explain borrower pressure and credit transmission, but it does not independently forecast recessions, equity direction, market timing, or default outcomes.

| Concept | Core meaning | Difference from refinancing risk |

|---|---|---|

| Liquidity risk | Liquidity risk concerns the ability to meet cash needs or transact without severe cost. | Refinancing risk is specifically about replacing maturing or existing debt on acceptable terms. |

| Interest-rate risk | Interest-rate risk concerns sensitivity to changes in rates. | Refinancing risk can be affected by rates, but it also depends on credit access, lender behavior, spreads, and borrower quality. |

| Credit spreads | Credit spreads reflect the yield premium required above a safer benchmark. | Credit spreads can influence refinancing terms, but refinancing risk also includes maturity timing and access to funding. |

| Financial conditions | Financial conditions describe the broader environment for rates, credit, liquidity, lending, and risk appetite. | Refinancing risk is one channel within that environment, not the whole environment. |

| Financial conditions index | A financial conditions index combines selected market and credit variables into a summary measure. | Refinancing risk is a borrower funding-pressure concept, not an index formula. |

| Recession forecast | A recession forecast makes a claim about future economic contraction. | Refinancing risk can be part of a credit-pressure picture, but it does not forecast recession by itself. |

| Equity or trading signal | A signal implies a directional or timing interpretation for markets. | Refinancing risk does not provide buy, sell, hedge, timing, or allocation instructions. |

Practical Scenario

A borrower has debt maturing and needs replacement financing. New debt is available, but rates are higher and lenders require stricter terms. The borrower can refinance, but the new funding increases interest expense and reduces financial flexibility.

If access weakens further, the same refinancing window can become a balance-sheet pressure point. The borrower may need to accept less favorable terms, reduce spending elsewhere, sell assets, or negotiate with lenders. If many borrowers face similar conditions at the same time, refinancing pressure can feed into broader credit conditions.

The scenario is illustrative. It does not describe a specific company, sector, date, or market episode. A real-world claim about current refinancing stress would require dated evidence and source verification.

Can Refinancing Risk Be Reduced or Measured?

Refinancing risk can be assessed, but it does not usually reduce to one simple formula. Useful inputs include maturity schedules, interest coverage, leverage, cash-flow stability, collateral quality, available credit lines, lender concentration, market liquidity, and the likely terms of replacement debt.

Risk can be lower when maturities are spread out, cash flow is resilient, liquidity reserves are adequate, and lenders remain willing to provide funding. Risk can be higher when debt comes due in a tight credit environment, borrower quality weakens, or market access depends on a narrow refinancing window.

For market interpretation, the key is not only whether a borrower can refinance. The key is how the refinancing terms change cash-flow flexibility, lender behavior, and the broader credit environment.

Related Concepts

Refinancing risk becomes easier to interpret when it is placed beside nearby credit and liquidity concepts rather than treated in isolation.

- Financial conditions provide the broader setting for rates, credit access, liquidity, and risk appetite.

- Credit spreads help measure the extra compensation demanded for credit risk.

- Bank lending standards help show whether lenders are becoming easier or stricter.

- Financial stress indicators help separate normal repricing from broader market strain.

- Liquidity risk helps distinguish funding access from market trading conditions and cash availability.

FAQ

What is refinancing risk?

Refinancing risk is the risk that a borrower may be unable to roll over, replace, or refinance existing debt on acceptable terms when funding is needed.

Is refinancing risk the same as rollover risk?

The two concepts are closely related. Rollover risk usually emphasizes replacing maturing obligations, while refinancing risk can also emphasize the cost, access, and terms of replacement funding.

What increases refinancing risk?

Refinancing risk can increase when rates rise, credit spreads widen, lender standards tighten, borrower credit quality weakens, liquidity deteriorates, or many maturities cluster in the same funding window.

Does refinancing risk predict recessions?

No. Refinancing risk can contribute to credit-pressure analysis, but it does not forecast recession by itself. Broader interpretation requires confirmation from credit, liquidity, lending, and macro indicators.

Is refinancing risk a market timing signal?

No. Refinancing risk is a funding and credit-pressure concept. It does not provide equity-direction, trading, hedging, buying, or selling instructions.