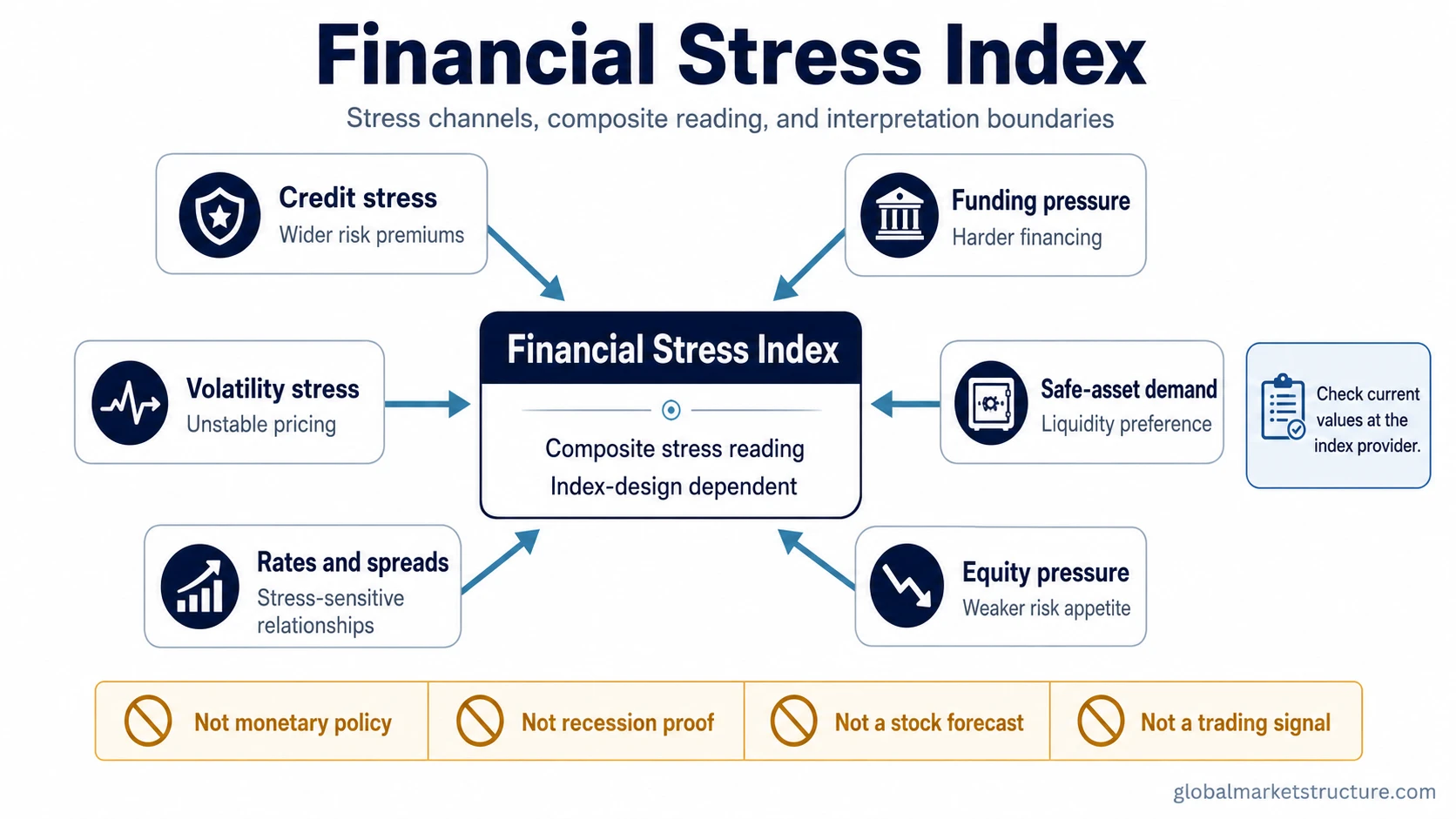

A financial stress index is a composite measure that condenses stress signals from selected financial-market channels into one reading. It helps classify whether market functioning looks calmer or more stressed than normal, but its meaning depends on the index design. It is not monetary policy itself, not recession proof, and not a direct stock-market forecast.

Definition: A financial stress index measures financial-market stress by combining selected indicators such as credit risk, funding pressure, volatility, safe-asset demand, rates, spreads, or equity-market pressure, depending on the methodology.

Boundary: The index is a stress monitor, not a forecast engine. A higher stress level can support market-structure interpretation, but it does not automatically prove a recession, a crisis, or a tradeable market direction.

Key Points

- A financial stress index summarizes stress across several financial-market channels rather than measuring one market alone.

- Different indexes can diverge because each methodology uses its own components, weights, frequency, geography, and baseline.

- Current values belong with official data providers or the index publisher because levels, revisions, and methodology notes can change.

- The index is most useful when interpreted with credit, funding, volatility, safe-asset, and broader financial-condition context.

What a Financial Stress Index Measures

A financial stress index measures pressure inside the financial system rather than ordinary market movement. The exact design varies, but the common idea is to combine several stress-sensitive variables into a single composite measure.

The pressure can come from wider risk premiums, harder funding conditions, rising volatility, stronger demand for safe assets, unstable rate spreads, or weakness in equity and credit markets. The index compresses the evidence into a headline value, while the component mix explains why the move happened.

A useful interpretation starts with three questions: which channels are contributing to stress, whether the move is broad or concentrated, and whether related markets confirm the same pressure. A single composite number can hide an important difference between broad systemic stress and a narrow move inside one market segment.

Financial Stress Index vs Financial Conditions Index

A financial stress index is narrower than a financial conditions index. The stress index focuses on signs of disruption, risk aversion, funding pressure, volatility, and market-functioning strain. A financial conditions index usually describes broader ease or tightness across rates, credit, equities, exchange rates, and policy-sensitive variables.

That distinction keeps financial stress focused on strain and disruption, while broader financial conditions can tighten without acute market-functioning stress.

Policy rates can rise and financial conditions can tighten without an immediate breakdown in market functioning. Stress becomes more relevant when the tightening is accompanied by risk-premium expansion, funding friction, volatility shocks, or a stronger demand for safe assets.

Simple distinction: a financial conditions index usually asks whether the environment is easy or tight. A financial stress index usually asks whether the financial system is showing signs of strain.

Main Stress Channels Inside a Financial Stress Index

The component set depends on the index provider, but several channel families appear frequently in financial-stress frameworks. Separating each stress channel from its interpretation boundary prevents the composite number from being treated as one universal signal.

| Stress channel | What it captures | Interpretation boundary |

|---|---|---|

| Credit stress | Higher compensation demanded for taking credit risk, often visible through wider credit spreads. | Credit stress is stronger when spread widening appears across lower-quality and higher-quality credit, not only in one narrow segment. |

| Funding pressure | More difficult access to short-term financing, collateral, liquidity, or balance-sheet capacity. | Funding stress needs context because temporary liquidity demand can look different from persistent refinancing risk. |

| Volatility stress | Higher uncertainty and larger price swings across risk assets, rates, credit, or currencies. | Volatility alone is not enough. The signal becomes more meaningful when volatility rises alongside liquidity strain or risk-premium expansion. |

| Safe-asset demand | Stronger preference for safer or more liquid assets during stress episodes. | Safe-asset demand can reflect growth fear, liquidity preference, policy expectations, or risk-off positioning, so confirmation matters. |

| Rates and spread pressure | Stress-sensitive movements in interest-rate spreads, term structure, or money-market relationships. | Rate-spread moves can reflect policy expectations, inflation repricing, growth concern, or funding stress depending on the surrounding data. |

| Equity-market pressure | Stress reflected through equity volatility, valuation compression, drawdowns, or weaker market risk appetite. | Equity weakness is not automatically systemic stress. It becomes more relevant when credit, funding, and volatility channels deteriorate together. |

How to Interpret the Index Without Overreading It

The first step is to read the index on its own terms. Some indexes use a zero or normal-stress baseline. Others use their own scale, regional design, weighting method, or component list. A positive, negative, high, or low value is not universal unless the index methodology defines what that level means.

The second step is to separate the composite level from the driver. A rise caused mainly by volatility is not identical to a rise caused by credit-market stress. A move driven by funding pressure can carry a different message than a move driven by equity-market turbulence.

The third step is to compare the index with the broader financial conditions backdrop. A stress measure is more useful when it is interpreted beside credit risk, liquidity conditions, rates, policy expectations, market breadth, and cross-asset confirmation.

Current readings: Live values, revisions, frequency, and methodology notes should be checked at the official index provider or a reliable data publisher. Interpretation depends on the source that maintains the actual index.

What a Financial Stress Index Does Not Prove

A financial stress index can help identify a more fragile market environment, but it does not prove a single macro or market outcome. Stress can rise before a downturn, during a temporary liquidity shock, after a volatility spike, or around a narrow credit event. The index needs confirmation from the surrounding market structure.

Common misread: A high stress level does not automatically prove recession risk has become certain. A low or negative level does not mean markets are safe. Both interpretations ignore methodology, component drivers, and the wider regime backdrop.

The index also should not be treated as a positioning trigger or market-timing shortcut. A stress monitor can help frame risk appetite and market functioning, but it cannot decide positioning, valuation, liquidity needs, or horizon by itself.

Country-level or regional financial stress indexes need extra care. Different economies have different market structures, banking systems, capital markets, currencies, and data availability. A country-level value is most useful inside its own methodology rather than as a simple global ranking.

Financial Stress Index Example in Context

A practical stress scenario can begin with several channels deteriorating at the same time. Credit spreads widen, funding markets become less forgiving, volatility rises, and safe-asset demand strengthens. The composite index may move higher because multiple parts of the financial system are showing pressure together.

That situation is more meaningful than a one-channel move, but it remains conditional. The index design still controls what the composite number means. The next question is whether the stress is broad, persistent, and confirmed by related markets, or whether it is concentrated in one temporary channel.

The strongest interpretation comes from sequence rather than one print. Component deterioration, a rising composite value, cross-asset confirmation, and persistent pressure create a more coherent stress picture. A single spike without confirmation is weaker evidence.

Related Concepts

Financial stress belongs inside the wider market-conditions layer. The distinction from financial conditions prevents the stress index from becoming a broad ease-or-tightness proxy. Credit spreads help explain the credit-risk premium channel, while refinancing risk helps explain why funding pressure can become more damaging when borrowers must roll debt in harder conditions.

Financial stress can also interact with the broader financial cycle when credit expansion, leverage, and refinancing pressure change together, but the index itself remains a stress measure rather than a full cycle model.

FAQ

Is a financial stress index the same as a financial conditions index?

No. A financial stress index focuses on market strain, disruption, volatility, funding pressure, and risk-premium stress. A financial conditions index usually measures broader ease or tightness across financial variables.

Does a financial stress index predict recessions?

No. A financial stress index can support recession-risk analysis, but it does not prove that a recession will happen. The measure needs context from growth, credit, policy, liquidity, and broader market behavior.

Where should current financial stress index readings come from?

Current readings should come from the official index provider or a reliable data publisher. Values, revisions, frequency, and methodology notes can change, so live levels need direct-source confirmation.