A financial conditions index is a composite measure that condenses market and financial-system variables into a reading of easier or tighter financial conditions. It helps classify the macro and liquidity environment, but it is not monetary policy itself, not a direct stock-market forecast, and not the same thing as a financial stress index.

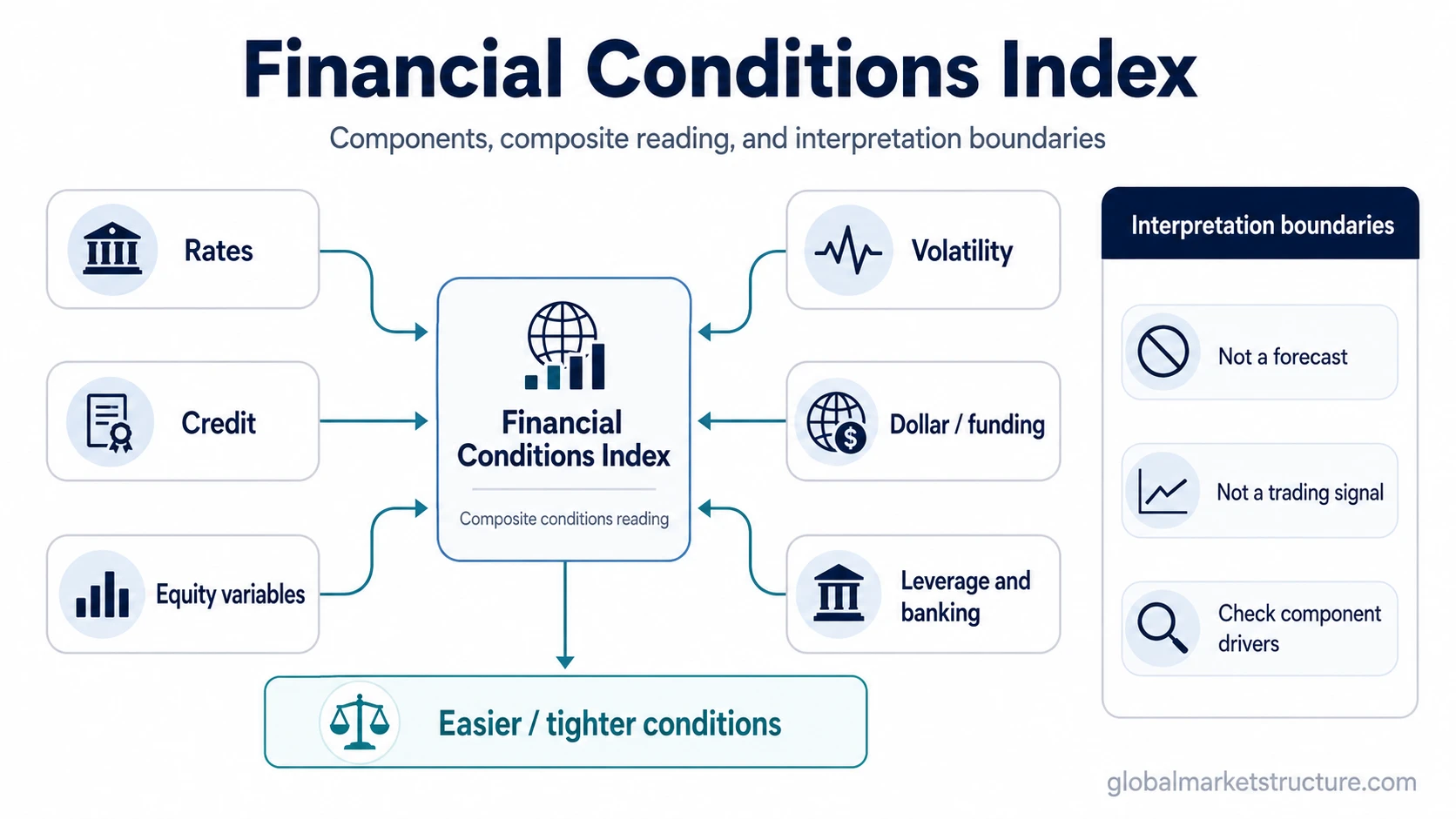

Definition: A financial conditions index combines selected indicators such as rates, credit spreads, equity-market variables, volatility, funding conditions, leverage, and banking conditions into one index reading. The exact inputs and weights depend on the index provider.

Boundary: Easier conditions usually mean financing and risk-taking conditions are less restrictive relative to the index design. Tighter conditions usually mean financing, risk pricing, or market functioning has become more restrictive. The reading is macro context, not a mechanical forecast.

Key Points

- A financial conditions index summarizes several market and financial variables into one conditions reading.

- The index is narrower than the full financial conditions environment because it depends on a specific model and input set.

- NFCI, ANFCI, and FCI-G are different index families, so their readings can diverge.

- A tight or loose reading can support macro interpretation, but it does not prove recession, market direction, or trade timing.

What a Financial Conditions Index Measures

A financial conditions index measures the state of market-facing financial conditions through a selected basket of variables. Some versions emphasize credit and leverage, some emphasize the expected growth impact of financial variables, and some focus more directly on financial stress. The shared purpose is to compress many signals into a single reading of ease or restraint.

| Component channel | What it can capture | Why it affects the reading |

|---|---|---|

| Rates | Policy rates, Treasury yields, real yields, or other interest-rate measures | Higher borrowing costs can make financing more restrictive and change valuation pressure. |

| Credit | Corporate bond spreads, risk premia, or borrowing-risk measures | Wider credit spreads can indicate higher compensation demanded for credit risk. |

| Equity variables | Equity prices, valuations, or risk-appetite measures | Equity strength can ease conditions through wealth, collateral, and confidence channels. |

| Volatility | Market volatility, uncertainty, or risk pricing | Higher volatility can make financing and risk-taking less stable. |

| Dollar, funding, and liquidity variables | Funding pressure, dollar strength, liquidity proxies, or money-market conditions | Funding strain can tighten conditions even when some asset prices remain firm. |

| Leverage and banking conditions | Balance-sheet pressure, bank lending conditions, or leverage-sensitive indicators | Credit supply and leverage conditions influence how easily risk can be financed. |

No single component explains every reading. The index level reflects the combined effect of the variables selected by the provider, their weights, and the purpose of the model.

Financial Conditions vs Financial Conditions Index

Financial conditions describe the broader environment in which credit, liquidity, risk appetite, rates, funding, and market functioning interact. A financial conditions index is a constructed measurement tool that tries to summarize part of that environment in one number.

Broad financial conditions: the actual macro and market environment across credit, liquidity, rates, funding, leverage, and risk appetite.

Financial conditions index: a model-based composite reading built from selected variables that represent that environment imperfectly.

The distinction matters because the environment can be mixed. Credit can tighten while equities remain strong. Funding can become more fragile while headline index levels still look calm. A composite index is useful because it organizes the evidence, but it cannot replace the underlying components.

Main Financial Conditions Index Families

Different financial conditions indexes answer related but not identical questions. The Chicago Fed NFCI, the adjusted NFCI, and the Federal Reserve’s FCI-G should not be treated as interchangeable readings.

| Term | Core idea | Useful for | Main boundary |

|---|---|---|---|

| Financial conditions | The broader credit, liquidity, rates, funding, leverage, and risk-appetite environment | Understanding the macro backdrop | Not one index or one data point |

| Financial conditions index | A composite measure of easier or tighter financial conditions | Condensing several variables into a structured reading | Depends on methodology, variables, weights, and lags |

| NFCI | Chicago Fed National Financial Conditions Index | Reading financial conditions through a broad official index family | One official construction, not a universal conditions measure |

| ANFCI | Adjusted National Financial Conditions Index | Reading financial conditions relative to the current economic environment | Adjustment changes interpretation relative to the unadjusted index |

| FCI-G | Federal Reserve index focused on the growth impulse from financial conditions | Interpreting headwinds or tailwinds to future economic growth | Designed around a different purpose from NFCI |

| Financial stress index | A stress-focused measure of disruption or pressure in financial markets | Monitoring systemic stress and market functioning risk | Not the same as a broad ease/tightness index |

The same week can produce different signals across index families because the models are built for different questions. A growth-impulse index, a credit-heavy conditions index, and a stress index can disagree without making any single reading useless.

How to Interpret Tight or Loose Readings

A tighter financial conditions index reading usually points to more restrictive conditions relative to the index baseline. A looser reading usually points to easier conditions. For some index families, positive and negative values are interpreted relative to a historical average or model baseline, but the exact meaning depends on the source methodology.

Tighter reading: financing, risk pricing, credit availability, volatility, or funding conditions may be becoming less supportive.

Looser reading: financing, risk appetite, volatility, or asset-price conditions may be becoming more supportive.

Mixed reading: some components may ease while others tighten, making the headline index less intuitive.

The reading becomes more useful when it is compared with its component behavior. A headline index that tightens because credit spreads widen carries a different message from a tightening driven mainly by rate moves or equity weakness.

Financial Conditions Index Example in a Mixed Market

Equity markets can remain firm while credit conditions begin to deteriorate. In that environment, equity variables may still point toward risk appetite, but credit spreads may widen, funding conditions may become less comfortable, and dollar strength may add pressure to global financing conditions.

The headline index may tighten only moderately if equity strength offsets credit or funding weakness inside the model. That does not erase the credit signal. It means the composite reading needs to be separated into its component channels before drawing a macro conclusion.

This type of mixed reading is one reason a financial conditions index works best as a context tool. It can organize the environment, but the interpretation still depends on which components are driving the move.

Common Misreadings and Limitations

The most common mistake is treating a financial conditions index as if it were a direct forecast. A tighter reading can indicate more restrictive conditions, but it does not automatically prove that a recession is coming. A looser reading can support risk appetite, but it does not guarantee stronger asset prices.

Methodology risk: different indexes use different variables, weights, and statistical designs.

Lag risk: some variables update slowly or reflect conditions that changed before the index is published.

Component-offset risk: easier equity conditions can offset tighter credit or funding conditions inside a composite reading.

Forecast risk: a conditions index can support macro interpretation, but it cannot replace growth, inflation, labor, credit, liquidity, and policy analysis.

Financial conditions indexes are most useful when they are read alongside component evidence. Credit, funding, rates, volatility, liquidity, and banking conditions can each change the meaning of the headline number.

Where Current Values Belong

Live index readings should be checked at the relevant official data source because observations change over time and need a clear date. Public interpretation can explain how the index works, but current values should not be copied without a source, observation date, and update context.

For interpretation, the stronger question is not only where the index stands today. The stronger question is what changed, which components drove the move, whether the move is broad or narrow, and whether related credit, funding, rate, dollar, and stress measures confirm the same environment.

Related Concepts

Broad financial conditions describe the full environment across credit, liquidity, rates, funding, leverage, and risk appetite. Credit spreads add a narrower credit-risk compensation lens because they show the extra yield demanded above safer benchmarks. Financial stress, lending standards, and refinancing risk add separate views of disruption, credit supply, and debt rollover pressure.

The strongest interpretation usually comes from comparing the index with its major channels rather than reading the headline number alone.

FAQ

Is a financial conditions index a forecast?

No. A financial conditions index summarizes conditions that can influence the macro environment, but it does not mechanically predict recession, stock-market direction, or trade timing.

Why do different financial conditions indexes show different readings?

Different indexes use different variables, weights, baselines, and purposes. One index may emphasize credit and leverage, while another may focus on the expected growth impulse from financial variables.

How is a financial conditions index different from a financial stress index?

A financial conditions index usually measures broader ease or tightness across financial variables. A financial stress index focuses more directly on disruption, pressure, or stress in financial markets.