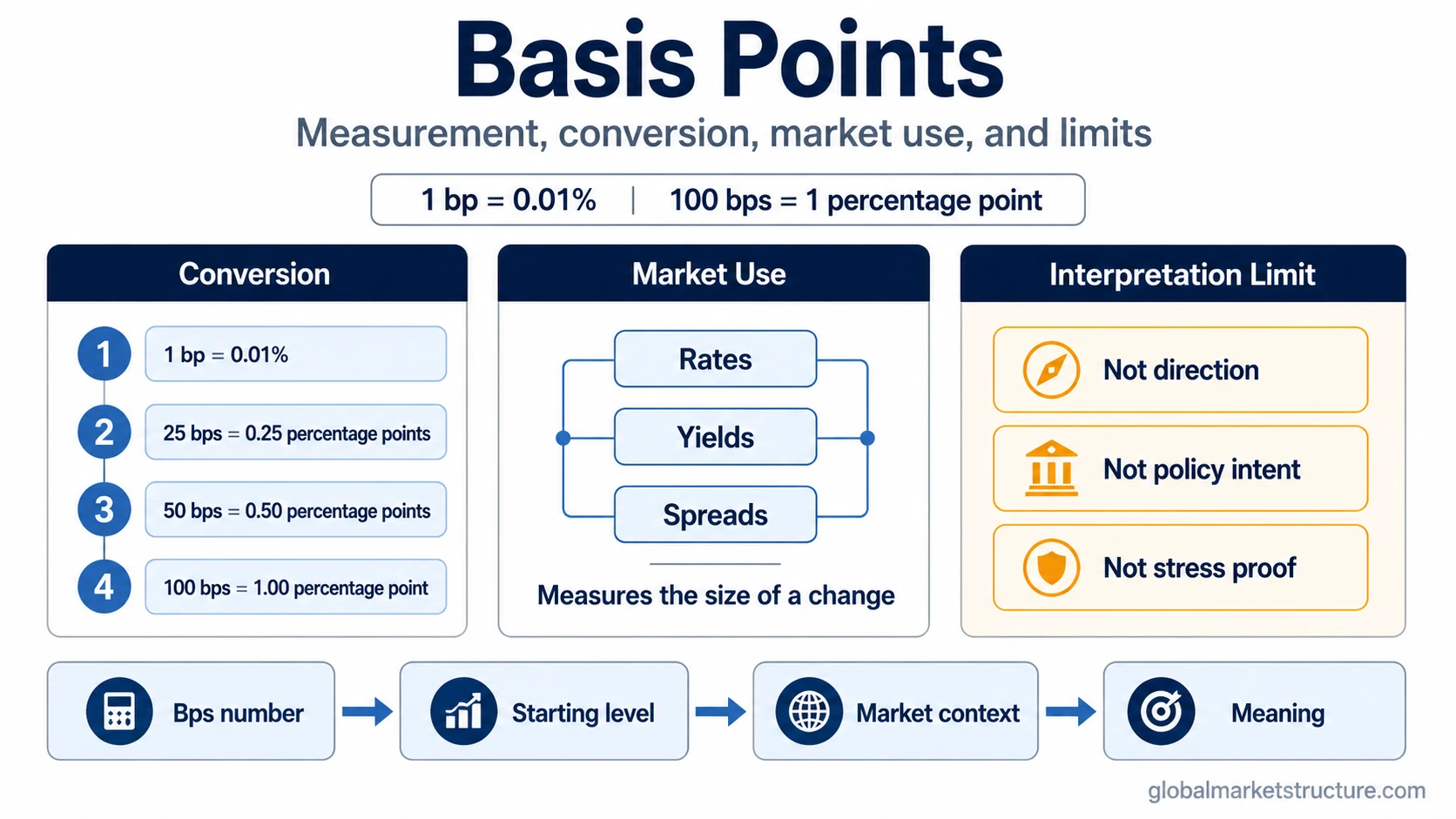

A basis point is one hundredth of one percentage point. One basis point equals 0.01%, and 100 basis points equal 1 percentage point. In market language, basis points are used to describe small changes in rates, yields, and spreads, but they measure the size of a change, not the market meaning of that change.

The abbreviation is usually written as bp for one basis point and bps for multiple basis points. A move of 25 bps means 0.25 percentage points. A move of 50 bps means 0.50 percentage points. This wording helps avoid confusion when markets discuss small changes in percentage-based measures.

Quick definition: basis points are a measurement unit for absolute changes in percentage-based financial figures. They are common in interest rates, bond yields, credit spreads, and policy-rate communication.

Basis points conversion

To convert basis points into percentage points, divide the number of basis points by 100. The result is the percentage-point change.

| Basis points | Percentage-point equivalent | Decimal percent form |

|---|---|---|

| 1 bp | 0.01 percentage points | 0.01% |

| 5 bps | 0.05 percentage points | 0.05% |

| 10 bps | 0.10 percentage points | 0.10% |

| 25 bps | 0.25 percentage points | 0.25% |

| 50 bps | 0.50 percentage points | 0.50% |

| 100 bps | 1.00 percentage point | 1.00% |

| 200 bps | 2.00 percentage points | 2.00% |

For example, if a rate rises from 4.00% to 4.25%, the change is 25 basis points. It is clearer to say “up 25 bps” than “up 0.25%,” because the latter can be confused with a relative percent change.

Basis points vs percentage points, percent changes, and spreads

Basis points are useful because finance often deals with small changes in percentage-based numbers. The term keeps absolute rate changes separate from relative percent changes and from spreads between two instruments.

| Term | What it means | Example |

|---|---|---|

| Basis point | One hundredth of one percentage point. | A 10 bps move equals 0.10 percentage points. |

| Percentage point | An absolute difference between two percentage figures. | A move from 3.00% to 4.00% is 1 percentage point, or 100 bps. |

| Percent change | A relative change compared with the starting value. | A move from 4.00% to 4.25% is a 0.25 percentage-point move, but a 6.25% relative increase from the starting rate. |

| Spread | The difference between two rates or yields, often quoted in basis points. | If one yield is 5.00% and another is 4.50%, the spread is 50 bps. |

How basis points are used in markets

Basis points are common in markets because rates, yields, and spreads often move in small increments. A central bank decision, bond-yield move, credit-spread change, or rate-expectation shift can be described more clearly in bps than in decimal percentages.

For bond markets, basis points are often used to describe changes in nominal yields. A 20 bps rise in a yield means the yield moved up by 0.20 percentage points, but the basis-point number alone does not explain why the yield moved.

Basis points also matter when markets discuss the risk-free rate, because small rate changes can influence discount-rate assumptions, valuation pressure, and cross-asset comparisons. Even there, the bps figure is only the measurement. The interpretation still depends on growth expectations, inflation, liquidity, credit conditions, and positioning.

Practical interpretation example

Example: a bond yield can rise by 25 bps while a credit spread widens by 40 bps. The basis-point figures describe the size of the changes, but they do not automatically explain the cause. The yield move could reflect rate expectations, inflation pricing, term premium, or supply-demand pressure. The spread move could reflect changing credit risk, liquidity conditions, or risk appetite.

The useful reading comes from the surrounding evidence. A basis-point move becomes more informative when it is compared with the starting level, the instrument involved, the broader rate environment, liquidity conditions, credit behavior, and cross-market confirmation.

What basis points do not tell you

A basis-point move is not a complete market signal. It describes the numerical size of a change, not the reason for the change or the likely market outcome.

| False reading | Why it is incomplete |

|---|---|

| A 25 bps move proves policy is dovish or hawkish. | The basis-point size must be interpreted against expectations, guidance, inflation data, growth conditions, and prior pricing. |

| A spread move proves market stress. | Spread widening can matter, but stress interpretation depends on liquidity, breadth, funding conditions, and persistence. |

| A yield move predicts market direction. | Rates can affect assets differently depending on growth expectations, inflation, liquidity, positioning, and valuation context. |

| Basis points are the same as percent changes. | Basis points describe absolute percentage-point changes. Percent changes are relative to the starting value. |

The safer rule is simple: use basis points to measure the move, then use broader market evidence to interpret the move.

FAQ

What does 1 basis point mean?

One basis point means 0.01%, or one hundredth of one percentage point.

How much is 25 basis points?

Twenty-five basis points equal 0.25 percentage points. For example, a move from 4.00% to 4.25% is a 25 bps move.

Are basis points the same as percentage points?

No. Basis points are units used to express smaller increments of percentage-point changes. One percentage point equals 100 basis points.

Do basis points predict market direction?

No. Basis points measure the size of a rate, yield, or spread change. Market direction depends on broader context, not the bps number alone.