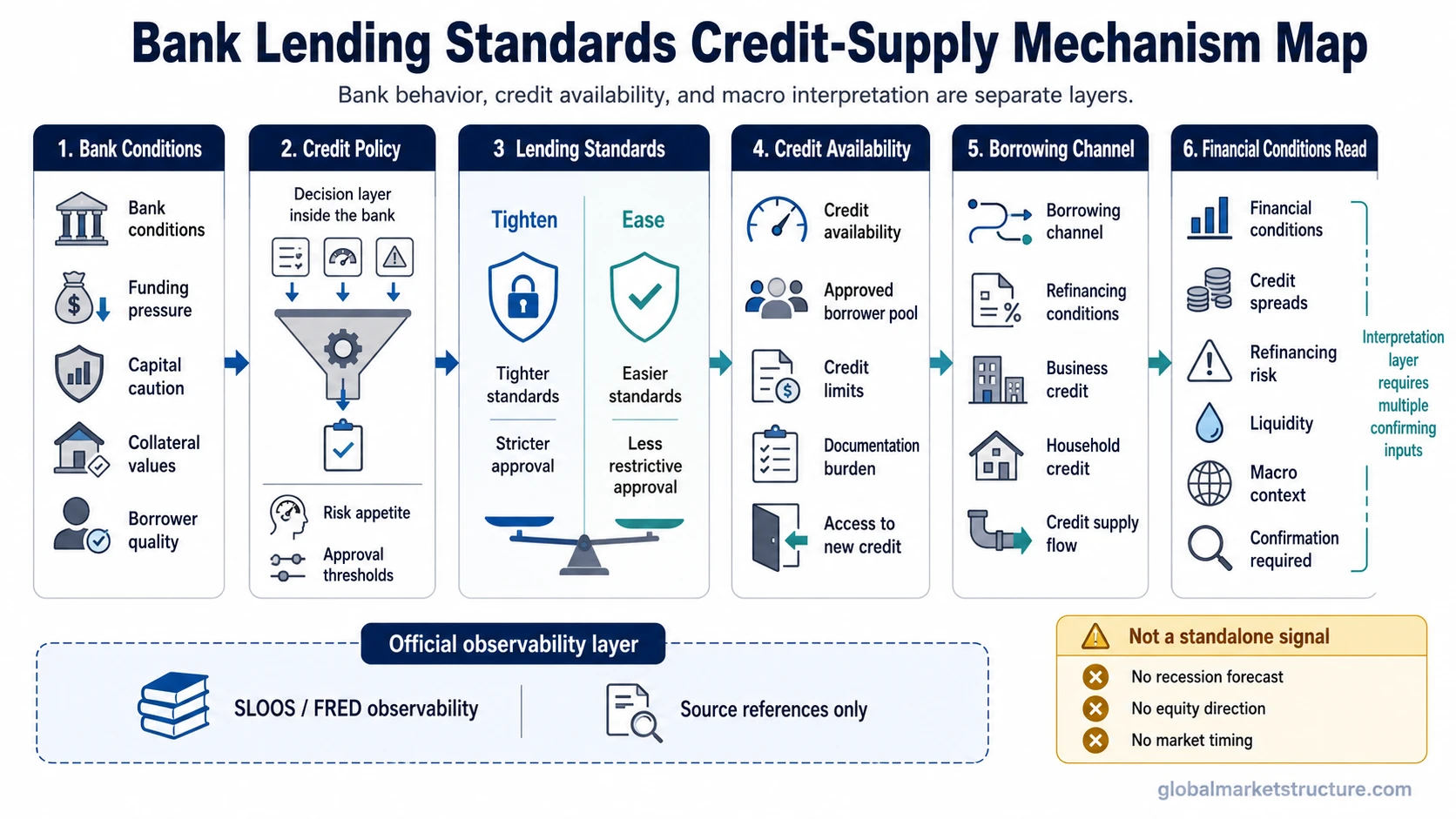

Bank lending standards are the rules, risk thresholds, and credit criteria banks use when deciding how freely to extend loans. In macro analysis, tighter standards point to more restrictive credit supply, while easier standards point to less restrictive bank behavior. They are a financial-conditions input, not a standalone recession forecast, equity signal, or market-timing tool.

Key Points

- Bank lending standards describe how strict banks are when extending credit.

- Tightening standards usually point to reduced credit supply, while easing standards point to less restrictive credit conditions.

- Lending standards are different from loan terms, borrower demand, interest rates, and credit spreads.

- Federal Reserve SLOOS and related FRED series can make lending-standard changes observable, but official sources remain the place for current readings and methodology details.

- Bank lending standards should be read with other financial-condition signals before drawing broader market conclusions.

Bank Lending Standards Definition

Bank lending standards refer to the credit approval rules banks apply before extending loans. They include internal judgments about borrower quality, collateral, leverage, repayment capacity, sector risk, and the bank’s own willingness to add credit exposure.

When standards tighten, banks become more selective. A borrower who may have qualified under easier conditions can face stricter approval thresholds, more documentation, lower credit limits, or rejection. When standards ease, banks are more willing to approve credit under less restrictive conditions.

The macro importance comes from the bank lending channel. If banks become less willing to lend, credit supply can weaken even before every borrower stops asking for loans. That makes lending standards useful for reading credit availability, but not sufficient for predicting a recession or asset-market direction by themselves.

How Bank Lending Standards Work

Lending standards sit between the banking system and the real economy. Banks do not only respond to the level of interest rates. They also decide how much risk they are willing to accept when new borrowers, companies, households, or institutions request credit.

Standards can tighten when banks become more cautious about borrower risk, asset quality, funding conditions, capital pressure, collateral values, or the economic outlook. The result is not always an immediate collapse in lending. The first change can be a narrower group of approved borrowers and a slower flow of new credit.

Standards can ease when banks become more comfortable with risk, funding pressure is lower, balance sheets are more flexible, and the economic outlook appears less threatening. Easier standards can support credit creation, but they still need to be interpreted alongside demand, loan terms, pricing, and broader financial conditions.

Credit-Supply Mechanism

Bank risk appetite: A bank that becomes more cautious may require stronger borrower income, better collateral, lower leverage, or more conservative loan structures.

Balance-sheet constraints: Capital pressure, funding costs, liquidity needs, or portfolio losses can reduce a bank’s willingness to expand credit exposure.

Borrower risk assessment: Weakening business conditions, falling collateral values, or greater default concern can make the same borrower look riskier than before.

Credit availability: Tighter standards can reduce the amount of credit available to the private sector, especially for borrowers that depend heavily on bank financing.

Financial conditions: When credit availability weakens, broader financial conditions can become more restrictive, particularly if credit pricing and market liquidity are also deteriorating.

Standards vs Terms vs Demand vs Credit Spreads

Bank lending standards are often confused with nearby credit concepts. The distinction matters because each one answers a different question about credit conditions.

| Concept | What It Measures | What It Can Indicate | Common Misread |

|---|---|---|---|

| Bank lending standards | How strict banks are when approving credit | Bank willingness to lend and credit-supply restraint | Reading stricter standards as a complete recession signal |

| Loan terms | The pricing, collateral, covenants, maturity, or conditions attached to a loan | How costly or restrictive approved credit becomes | Treating tougher terms as the same thing as rejected credit |

| Loan demand | How much borrowers want credit | Borrower appetite, investment plans, working-capital needs, or caution | Confusing weak demand with banks refusing to lend |

| Credit spreads | The market price difference between riskier credit and safer benchmark debt | Market pricing of credit risk and risk compensation | Treating market pricing as identical to bank loan approval behavior |

How SLOOS and FRED Make Lending Standards Observable

Bank lending standards are not directly visible in a market price. They are usually observed through official survey and data sources, especially SLOOS and related FRED series. These sources can show whether banks are reporting tighter or easier standards for different categories of lending.

The important distinction is source role. Official data sources provide the measurement surface. A macro interpretation layer explains why the measurement matters, how it differs from nearby credit indicators, and what limits should apply before turning the data into a broader market view.

Current readings, survey scope, respondent details, release timing, and data units should be checked directly against official sources before publication. Without a dated source, the safer treatment is conceptual: SLOOS and FRED can help observe lending-standard changes, but they should not be replaced by a static summary.

Why Lending Standards Matter for Financial Conditions

Lending standards matter because bank credit is part of the transmission path between financial conditions and economic activity. When banks become more selective, some borrowers may lose access to credit, receive smaller commitments, or face more restrictive approval hurdles.

This can affect business investment, working capital, commercial real estate financing, consumer credit availability, and the ability of weaker borrowers to roll existing obligations. The pressure can become more important when borrowers already face refinancing risk, because stricter standards can make debt renewal harder.

The signal is strongest when lending standards align with other evidence of tighter financial conditions. If standards are tightening while credit spreads widen, liquidity weakens, and borrower demand softens, the credit environment is more restrictive than a single indicator would show on its own.

Practical Scenario

A common credit-cycle scenario is that banks become more cautious before every borrower shows obvious distress. Loan officers may raise approval thresholds because collateral quality looks weaker, borrower leverage is higher, or the economic outlook is less stable.

In that setting, credit availability can weaken even if headline demand has not collapsed. The useful interpretation is not that a recession is guaranteed. The useful interpretation is that the bank lending channel is becoming less supportive, and that the signal needs confirmation from other credit and liquidity conditions.

What Bank Lending Standards Do Not Mean

Bank lending standards do not prove that a recession has started. They can show a more cautious credit-supply environment, but recessions require broader economic evidence.

They do not predict equity direction by themselves. Equity markets can respond to earnings, liquidity, rates, positioning, valuation, policy expectations, and risk appetite in ways that do not map mechanically to one lending survey input.

They are not the same as loan demand. A bank can tighten standards while borrowers still want credit, and borrowers can reduce demand even if banks are still willing to lend.

They are not consumer underwriting advice. The macro question is how banks behave as credit suppliers across the economy, not whether one borrower qualifies for a specific loan.

How to Read Lending Standards With Related Signals

Lending standards are most useful when read as one part of a financial-conditions map. The first question is whether banks are becoming more or less restrictive. The second question is whether other credit signals confirm the same direction.

Tightening lending standards deserve closer attention when they appear alongside wider credit spreads, weaker credit availability, tighter funding conditions, or more difficult refinancing conditions. That combination can point to a credit environment where both bank behavior and market pricing are becoming less supportive.

The opposite is also important. If standards ease while demand remains weak or spreads remain elevated, the credit cycle may still be fragile. Easier bank standards do not automatically mean strong borrowing, stronger growth, or immediate risk-on conditions.

Official Data vs Macro Interpretation

Use official Federal Reserve and FRED sources for current readings, survey scope, respondent details, release timing, and data units. Bank lending standards describe bank willingness to extend credit; macro interpretation requires separate confirmation from credit pricing, liquidity, borrower demand, and funding stress.

FAQ

What are bank lending standards?

Bank lending standards are the rules, risk thresholds, and credit criteria banks use when deciding whether to approve loans. In macro analysis, they help show whether banks are becoming more or less willing to supply credit.

Are tighter lending standards the same as weaker loan demand?

No. Tighter lending standards describe bank behavior, while loan demand describes borrower behavior. Banks can become more restrictive even when borrowers still want credit, and borrowers can reduce demand even when banks remain willing to lend.

Do tighter lending standards predict a recession?

Tighter lending standards can indicate a more restrictive credit environment, but they do not prove that a recession is coming or already underway. They should be read with other economic, credit, liquidity, and market signals.