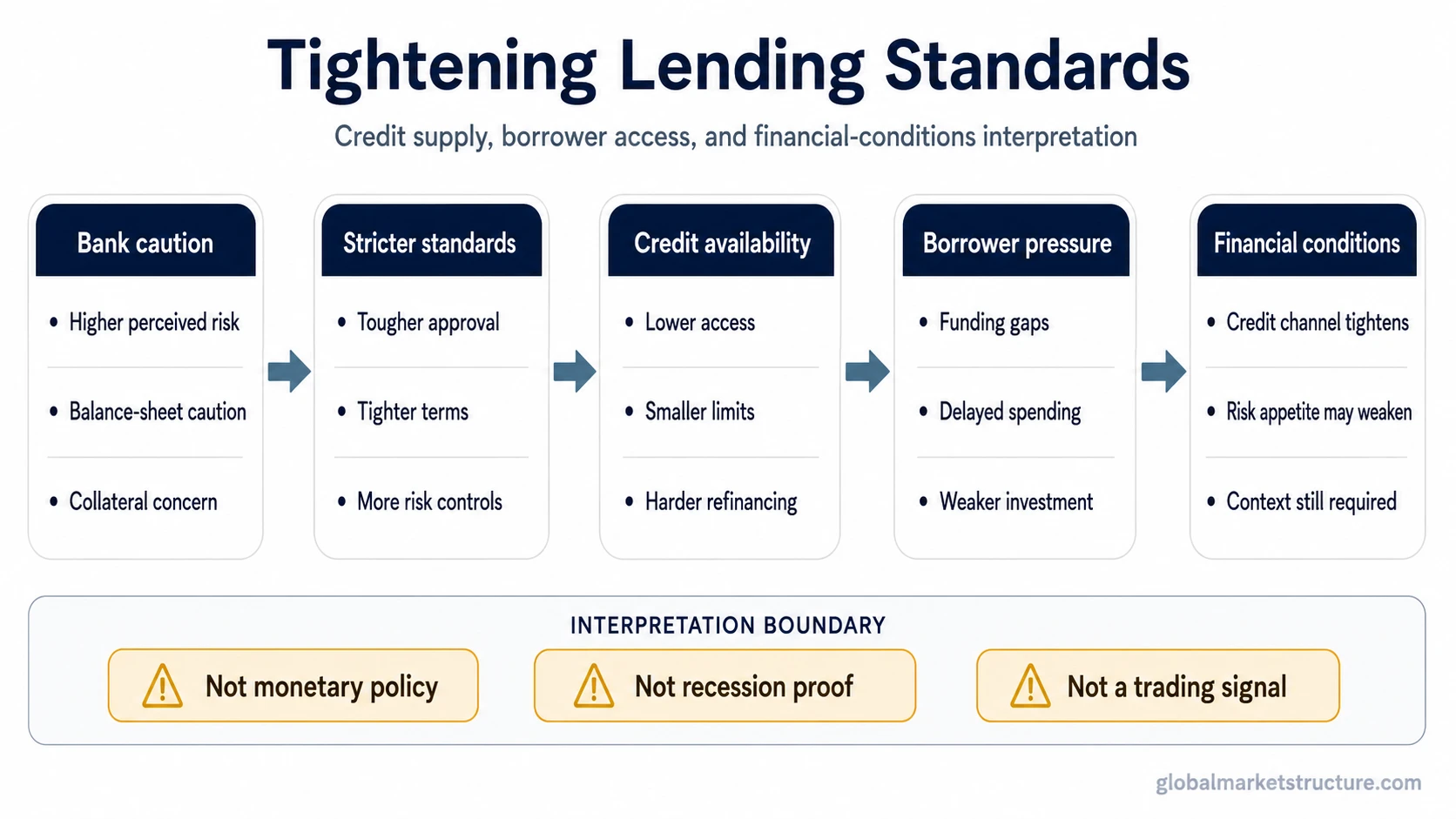

Tightening lending standards means banks are becoming stricter about extending credit through approval criteria, collateral requirements, loan terms, pricing, or risk controls. The financial-conditions reading depends on whether stricter standards reflect reduced credit supply, weaker borrower demand, or banks reacting to higher perceived risk. Tightening standards can matter for credit availability and refinancing pressure, but they are not the same as tighter monetary policy, recession evidence, or a market-timing tool.

Definition: tightening lending standards describe a bank-side shift toward stricter credit approval, tougher terms, or more cautious risk controls. The phrase focuses on how willing banks are to supply credit under existing conditions, not simply on whether borrowers want loans.

Key Points

- Banks tighten lending standards when credit approval, collateral rules, pricing terms, or risk controls become stricter.

- Lending standards and loan demand are separate signals: one describes bank-side credit criteria, while the other describes borrower appetite.

- Tighter standards can restrict credit supply, but they can also reflect banks reacting to weaker conditions or higher perceived borrower risk.

- The reading belongs inside financial-conditions analysis, not standalone recession forecasting or short-term timing.

What Tightening Lending Standards Mean

Tightening lending standards usually means banks are applying more caution before approving new credit or extending existing credit. That caution can appear through stricter borrower-quality requirements, higher collateral demands, wider loan spreads, shorter maturities, lower credit limits, or more restrictive covenants.

The important distinction is supply versus demand. A bank can tighten standards even if borrowers still want credit. Borrowers can also reduce loan demand even if banks are willing to lend. Those two conditions can point to different parts of the macro environment.

Bank lending standards describe the broader survey and credit-criteria concept. Tightening lending standards isolate one directional condition: banks are becoming more selective or restrictive.

Standards, Demand, Policy Rates, and Credit Spreads

Tighter lending standards are often confused with nearby credit and macro signals. The distinction matters because each signal answers a different question about the credit environment.

| Signal | What it describes | Main interpretation boundary |

|---|---|---|

| Lending standards | Bank-side approval criteria, loan terms, collateral requirements, pricing, and risk controls. | Shows how willing banks are to supply credit under current perceived risk. |

| Loan demand | Borrower-side appetite for new credit or expanded credit use. | Weak demand can reflect lower investment appetite even if banks remain willing to lend. |

| Policy rates | Central-bank rate setting and the short-rate baseline that influences funding and borrowing costs. | Lower policy rates do not automatically mean banks loosen credit standards. |

| Credit spreads | Market pricing of credit risk above safer benchmark yields. | Spreads can reflect investor risk compensation, while lending standards reflect bank credit behavior. |

| Financial conditions | The broader environment across rates, credit, liquidity, asset prices, risk appetite, and financing access. | Lending standards are one input, not the entire conditions framework. |

Why Tighter Standards Change Financial Conditions

Tightening standards can make financial conditions feel tighter because they change the availability of credit, not only the price of credit. A borrower may face higher documentation hurdles, lower approved amounts, tougher collateral requirements, or a higher risk premium even when headline interest-rate expectations look easier.

The credit-supply chain is usually conditional. Banks perceive more risk, protect balance-sheet flexibility, or become less willing to extend marginal credit. Stricter standards then reduce access for weaker borrowers, make refinancing harder, and can pressure spending, investment, hiring plans, inventory financing, or real-estate activity.

That is why tighter standards belong inside financial conditions. They describe a transmission channel where credit availability can tighten before the effect is fully visible in broad market prices.

Condition, Interpretation, and Limitation

The same tightening reading can mean different things depending on demand, policy expectations, market pricing, and which loan category is affected. A useful interpretation separates the observed condition from the conclusion being drawn from it.

| Observed condition | Possible interpretation | Limitation |

|---|---|---|

| Standards tighten while loan demand weakens. | Credit supply and borrower appetite may both be deteriorating. | The reading still does not prove recession timing or asset-market direction. |

| Standards tighten while loan demand remains firm. | Banks may be restricting credit even though borrowers still want financing. | Credit pressure may build later if borrowers cannot refinance or obtain new credit. |

| Standards tighten while policy rates are falling or expected to fall. | Bank risk perception may be offsetting easier rate expectations. | Rate policy and bank credit supply are related, but they are not identical. |

| Standards tighten while credit spreads remain calm. | Bank credit behavior may be warning of caution not yet visible in market pricing. | Spreads can adjust later, or bank caution may remain category-specific. |

| Standards tighten in one loan category. | Stress may be concentrated in a narrow borrower group or collateral type. | Category-specific tightening should not be treated as economy-wide credit stress without broader evidence. |

| Standards tighten after economic data weakens. | Banks may be responding to higher perceived risk rather than creating the weakness alone. | The tightening can be a symptom, a cause, or a transmission channel depending on sequence and context. |

SLOOS and Net Tightening Context

In U.S. macro analysis, lending standards are often discussed through the Federal Reserve’s Senior Loan Officer Opinion Survey. The survey separates lending standards from loan demand and asks banks about changes in lending standards, lending terms, and demand conditions across different credit categories.

SLOOS-based data series are often expressed as a net percentage of banks reporting tighter standards, meaning tightening responses are compared with easing responses for the same credit category. A positive net tightening reading generally means more banks reported tighter standards than easier standards during the survey period.

Measurement note: SLOOS is a survey of reported bank lending behavior and demand conditions. It is not monetary policy itself, a complete lending-volume dataset, or a direct forecast. Current readings require a dated official source check before publication.

When the Reading Can Mislead

Tightening lending standards can mislead when the reading is treated as a single-direction forecast. A stricter lending environment can pressure credit availability, but the reason for the tightening matters. Banks may tighten because they expect weaker borrower quality, because collateral values are less reliable, because funding conditions changed, or because balance-sheet caution increased.

The common mistake is reading tighter standards as proof of one outcome. It is usually better to ask whether the tightening is broad or category-specific, whether loan demand is also weakening, whether credit spreads confirm the stress, and whether refinancing pressure is increasing.

Important limitation: tightening lending standards are not standalone recession evidence, a direct stock-market forecast, or a trading signal. The condition becomes more informative when it appears alongside weaker demand, wider credit spreads, tighter liquidity, rising default concern, or deteriorating market breadth.

Example of a False Reading

Scenario: policy-rate expectations move lower and broad asset prices remain stable, so credit appears easier on the surface. At the same time, banks become more cautious with borrowers that depend on refinancing, variable-rate debt, or cyclical revenue. Lending standards tighten even though the headline rate story looks easier.

The false reading is assuming that lower expected rates automatically create easier credit. A cleaner interpretation separates rate policy from bank risk appetite. Credit may still be harder to obtain if banks are concerned about collateral values, borrower cash flow, funding pressure, or balance-sheet protection.

How to Read Tightening Standards Without Turning Them Into a Forecast

A disciplined reading starts with classification. First, identify whether the tightening is broad or concentrated. Second, compare standards with loan demand. Third, check whether market credit pricing confirms or contradicts the bank-side reading. Fourth, place the condition inside the broader financial-conditions environment.

The strongest interpretation does not come from one survey line alone. It comes from the sequence: standards tighten, borrower access weakens, refinancing pressure rises, credit spreads or funding stress confirm the pressure, and broader risk appetite starts to respond.

If that sequence is incomplete, the reading remains useful but unresolved. A narrower interpretation is more appropriate when tightening is category-specific, loan demand is still resilient, spreads are calm, refinancing pressure is contained, and other liquidity indicators do not confirm stress.

Related Credit and Conditions Concepts

Tightening lending standards are easiest to interpret after the broader survey concept is clear. Bank lending standards define the wider bank-credit framework, including how standards can differ by loan type, borrower group, and lending terms.

Financial conditions provide the wider market setting around the reading. Credit standards, policy rates, credit spreads, liquidity, asset prices, and risk appetite can all point in the same direction, or they can send mixed messages that require a more cautious interpretation.

FAQ

What does tightening lending standards mean?

Tightening lending standards mean banks are applying stricter credit approval criteria, terms, collateral requirements, pricing, or risk controls before extending credit.

Are tighter lending standards the same as lower loan demand?

No. Tighter lending standards describe bank-side credit restrictions. Lower loan demand describes weaker borrower appetite for credit. Both can happen together, but they are different signals.

Can lending standards tighten while policy rates fall?

Yes. Policy rates and bank lending behavior can move differently. Banks may tighten credit standards if borrower risk, collateral uncertainty, funding pressure, or balance-sheet caution rises.

Do tightening lending standards predict recession?

No. Tightening lending standards can be an important credit-supply warning, but they are not standalone recession evidence. Interpretation depends on demand, credit spreads, refinancing pressure, liquidity, and broader financial conditions.