Liquidity risk is the risk that funding needs or asset sales cannot be handled without meaningful loss, stress, or price impact. In market-structure terms, it usually appears through two channels: market liquidity risk, where assets become harder to trade efficiently, and funding liquidity risk, where participants have trouble obtaining cash, financing, or collateral when they need it.

Liquidity risk is not a direct forecast and it is not a trading signal. It describes a condition where the ability to transact, finance positions, or absorb selling pressure may become weaker than it appears under normal conditions.

What Is Liquidity Risk?

Liquidity risk is a financial risk and market-structure stress concept. It concerns the possibility that a participant, institution, fund, dealer, or market cannot meet funding needs or convert assets into cash without a meaningful loss, wider spread, larger price impact, or forced adjustment.

The useful distinction is between general liquidity as a broad concept and liquidity risk as the vulnerability that appears when liquidity is needed but becomes costly, unreliable, or unavailable.

A market can look orderly during normal conditions and still contain liquidity risk. The risk is easier to see when transaction costs rise, market depth fades, collateral becomes harder to finance, or sellers must accept worse prices to raise cash.

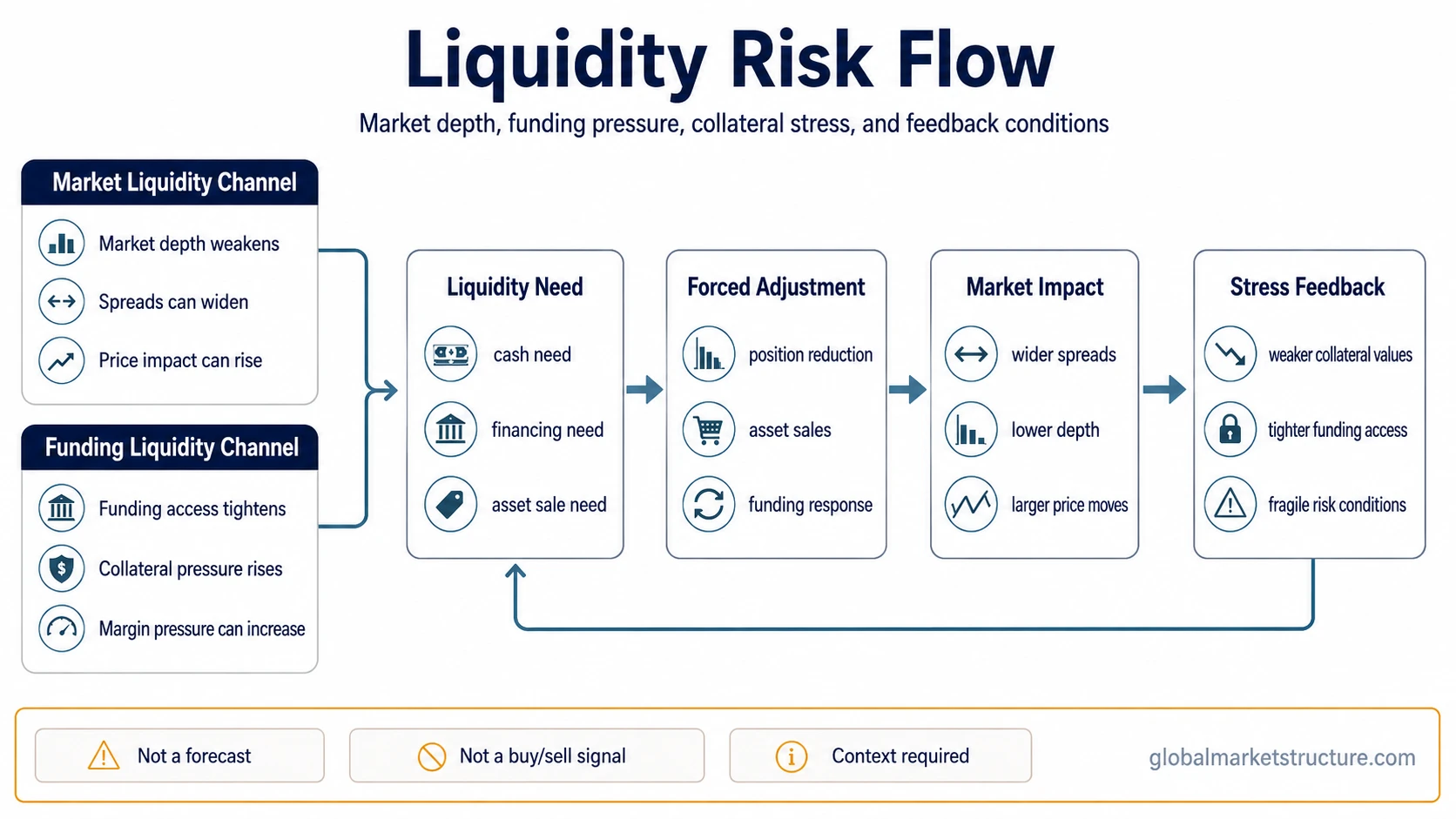

Market Liquidity Risk vs Funding Liquidity Risk

The most important split is between the ability to trade an asset and the ability to fund a position. These channels can exist separately, but they can also reinforce each other under stress.

| Type | What deteriorates | How it can appear | Why it matters | Limitation |

|---|---|---|---|---|

| Market liquidity risk | The ability to trade without large price impact | Wider bid-ask spreads, lower depth, thinner order books, larger price moves for the same trade size | Asset sales can become more expensive exactly when participants need to transact | High volume alone does not always mean strong market liquidity |

| Funding liquidity risk | The ability to obtain financing, cash, or collateral | Tighter financing terms, collateral pressure, margin pressure, difficulty rolling funding | Participants may be forced to reduce positions or sell assets to meet cash needs | A solvent participant can still face funding stress if timing or collateral access breaks down |

Market liquidity risk focuses on transaction conditions. Funding liquidity risk focuses on access to cash, financing, and collateral. Liquidity risk becomes more serious when weakness in one channel starts pressuring the other.

How Liquidity Risk Spreads Through Markets

Liquidity risk often spreads through a chain rather than a single event. A funding constraint can force asset sales. Asset sales can weaken prices or collateral values. Weaker collateral can reduce financing access. Reduced financing access can create more selling pressure.

Mechanism sequence:

- A liquidity channel weakens, either through trading conditions or funding access.

- Participants become less able to transact, finance positions, or absorb shocks.

- Market depth may fall and bid-ask spreads may widen.

- Collateral pressure or margin pressure may force position reductions.

- Forced selling can increase price impact and reinforce stress conditions.

The key point is conditional reinforcement. Liquidity risk does not always become a crisis. It matters most when market depth, funding access, leverage, collateral needs, and counterparty confidence weaken together.

Why Liquidity Risk Matters Most Under Stress

Liquidity risk can stay hidden while conditions are calm because participants may assume that normal transaction and funding conditions will remain available. Stress changes that assumption. The same position that looked manageable in normal conditions can become harder to finance or exit when spreads widen, depth falls, or lenders demand better collateral.

This is why liquidity risk is different from ordinary volatility. Volatility describes price movement. Liquidity risk describes whether participants can transact or finance positions without turning the need for liquidity into an additional source of stress.

In broader market interpretation, liquidity risk can help explain why pressure can move from funding markets into asset markets, or from asset markets back into funding conditions. It can also help separate a normal price decline from a more fragile environment where the ability to absorb selling pressure is deteriorating.

Illustrative Scenario

A market may appear liquid while trading is orderly and financing is easy. Spreads are narrow, buyers are present, and leveraged participants can roll funding without major difficulty.

Stress can change that structure. If financing becomes harder and collateral haircuts rise, some participants may need to sell assets to raise cash. If market depth is also weaker, those sales may move prices more than expected. Lower prices can then reduce collateral values and create additional funding pressure.

This scenario is illustrative, not a historical case. It shows how liquidity risk can build through the interaction between transaction conditions and funding constraints without turning the concept into a forecast.

What Liquidity Risk Is Not

Liquidity risk is not the same as insolvency. Solvency concerns whether assets and obligations can ultimately be honored. Liquidity risk concerns whether cash, financing, or tradable market depth is available when needed. A solvent participant can still face liquidity stress if timing, collateral access, or funding access breaks down.

Liquidity risk is not the same as volatility. Volatility is about price movement. Liquidity risk is about the ability to transact or fund positions without severe cost, loss, or market impact.

Liquidity risk is not a standalone crash forecast. It can describe vulnerability, but it does not prove that a crisis, crash, or forced-selling episode will occur.

Liquidity risk is not a buy or sell signal. It is a structural risk condition that needs context from funding access, market depth, collateral pressure, leverage, and broader financial conditions.

Liquidity Risk, Liquidity Crisis, and Liquidity Spiral

Liquidity risk is the vulnerability. A liquidity crisis is a more severe state where normal liquidity conditions break down and stress becomes harder to contain.

A liquidity spiral describes the feedback loop that can form when falling prices, tighter funding, weaker collateral values, and forced selling reinforce one another. Liquidity risk does not always become a spiral, but the spiral concept explains why liquidity stress can accelerate when both transaction liquidity and funding liquidity weaken together.

How Liquidity Risk Can Be Observed

Liquidity risk cannot be reduced to one indicator. Market participants often look at transaction conditions, funding conditions, and stress behavior together.

| Observation area | What it can show | Why it should be interpreted carefully |

|---|---|---|

| Bid-ask spreads | Whether transaction costs are widening | Spreads can widen for temporary or market-specific reasons |

| Market depth | Whether larger trades can be absorbed | Visible depth can change quickly under stress |

| Price impact | Whether trades move prices more than expected | Price impact depends on asset type, trade size, and market conditions |

| Funding access | Whether participants can finance or roll positions | Funding stress may appear before it is obvious in asset prices |

| Collateral pressure | Whether lower collateral values can tighten financing | Collateral pressure can be specific to certain assets or participants |

| Forced selling | Whether liquidity needs are turning into position reductions | Forced selling needs context from funding pressure, leverage, and market depth |

For a narrower measurement path, how to measure market liquidity focuses on spreads, depth, volume, price impact, and related market-liquidity indicators.

Related Liquidity Concepts

Liquidity risk sits inside a larger liquidity cluster. The broad concept is liquidity. Market liquidity explains the trading channel. Funding liquidity explains the financing channel. Liquidity crisis and liquidity spiral explain escalation and feedback behavior.

| Concept | Use it for | Destination |

|---|---|---|

| Liquidity | Broad liquidity meaning and market context | Liquidity |

| Market liquidity | Trading depth, spreads, and price impact | Market Liquidity |

| Funding liquidity | Financing access, collateral, and funding pressure | Funding Liquidity |

| Liquidity crisis | Breakdown of normal liquidity conditions | Liquidity Crisis |

| Liquidity spiral | Feedback loops between forced selling, prices, collateral, and funding | Liquidity Spiral |

For broader transmission beyond the risk concept itself, how liquidity affects markets connects liquidity conditions to wider market behavior.

FAQ

Is liquidity risk the same as solvency risk?

No. Liquidity risk concerns the ability to obtain funding or sell assets when needed without severe cost or stress. Solvency risk concerns whether obligations can ultimately be honored. A participant can be solvent but still face liquidity stress if funding access, collateral availability, or timing breaks down.

What is the difference between market liquidity risk and funding liquidity risk?

Market liquidity risk concerns trading without large price impact. Funding liquidity risk concerns access to cash, financing, or collateral. The two can reinforce each other when weaker prices reduce collateral value and tighter funding forces asset sales.

Can liquidity risk predict a market crash?

No. Liquidity risk can show vulnerability, but it does not predict a crash by itself. Its meaning depends on market depth, funding access, leverage, collateral pressure, and broader stress conditions.