A liquidity crisis is a stress condition in which access to cash, funding, or liquid markets becomes insufficient relative to immediate obligations or liquidity demand. It can appear through weaker financing access, thinner market depth, forced selling, collateral pressure, and feedback loops. It is not automatically the same as insolvency, a recession forecast, or a market-direction signal.

Definition: A liquidity crisis occurs when participants need usable liquidity faster than they can obtain it through cash reserves, borrowing, asset sales, or normally liquid markets.

Category: Liquidity-stress condition within broader market structure and monetary conditions.

Core boundary: Liquidity stress concerns access and transaction capacity. Insolvency concerns whether assets or expected cash flows are insufficient to cover liabilities.

Key Points

- A liquidity crisis is not just a shortage of cash. It can involve funding access, market depth, collateral demands, and forced selling pressure.

- Funding liquidity and market liquidity can reinforce each other when financing becomes harder and asset sales meet weaker trading depth.

- High trading volume does not prove strong liquidity if price impact is large, depth is thin, or participants are selling because they must raise cash.

- A liquidity crisis can create systemic pressure, but it is not automatically insolvency, recession, or a trading signal.

What a Liquidity Crisis Means

A liquidity crisis means usable liquidity becomes scarce relative to immediate demand. The pressure may come from borrowers needing cash, institutions needing funding, investors needing to sell assets, or markets losing the depth needed to absorb transactions without large price moves.

The concept is broader than a company simply running out of cash. In market-structure terms, the important question is where liquidity becomes constrained: financing access, collateral capacity, trading depth, or the ability to convert assets into cash without forcing large price concessions.

Liquidity stress can remain localized, or it can spread when many participants need cash at the same time. The risk becomes more serious when the normal channels for obtaining liquidity weaken together.

How a Liquidity Crisis Develops

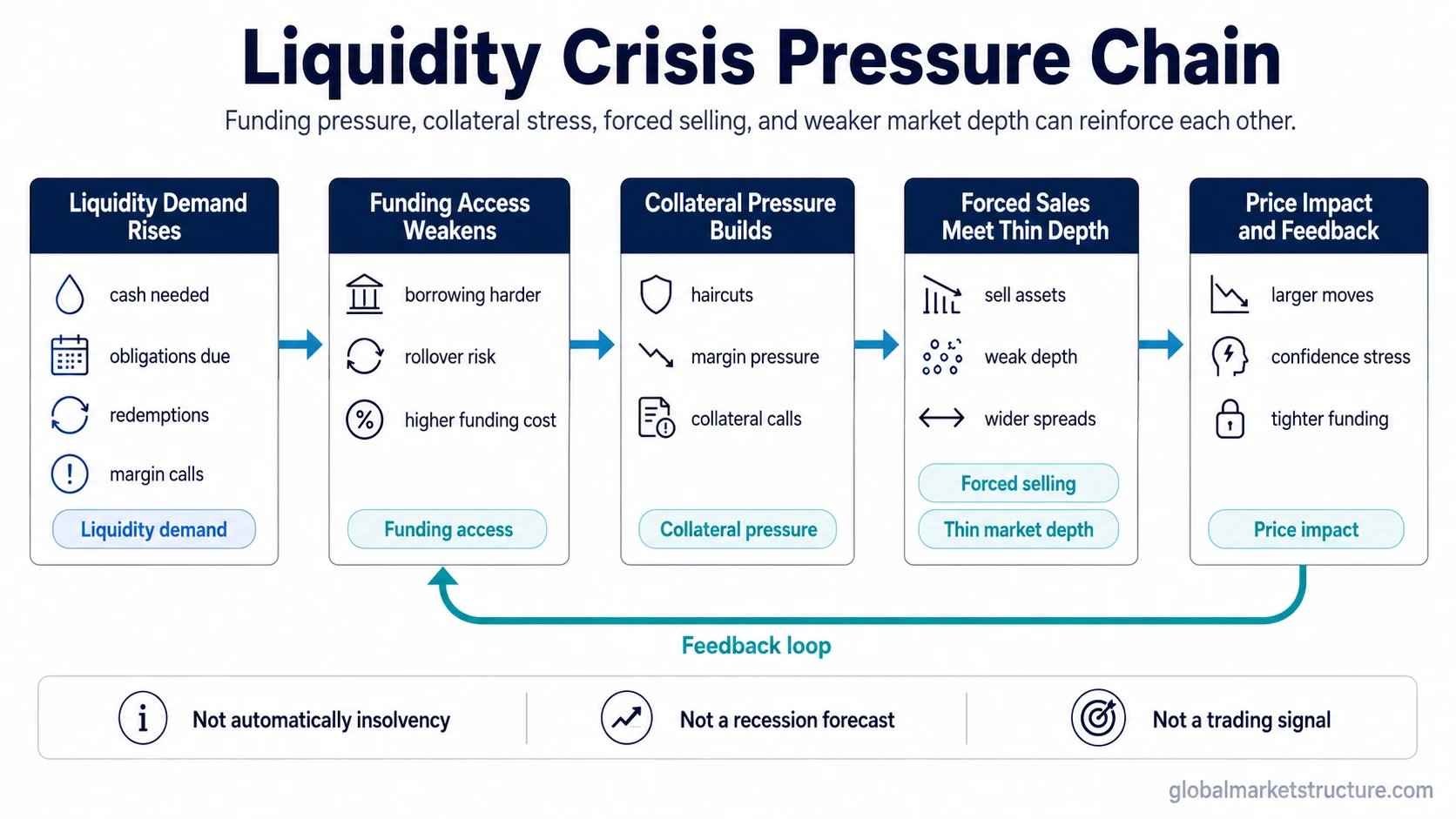

A liquidity crisis usually develops through a sequence rather than a single event. The sequence matters because the stress can begin in funding markets, trading markets, collateral channels, or several places at once.

- Cash or funding need rises: participants need liquidity to meet obligations, roll financing, cover withdrawals, post collateral, or reduce exposure.

- Financing access tightens: lenders become more cautious, funding terms worsen, haircuts rise, or credit availability weakens.

- Liquid assets become more valuable: cash and highly liquid securities become more important because they can meet obligations quickly.

- Market depth weakens: buyers become less willing to absorb supply at previous prices, and larger trades move prices more sharply.

- Forced selling can appear: participants sell not because they want to change long-term views, but because they need liquidity or must meet constraints.

- Feedback loops may develop: falling prices can reduce collateral values, raise margin pressure, and force more selling.

Funding Liquidity vs Market Liquidity in a Crisis

Funding liquidity and market liquidity describe different stress channels, even when both appear during the same crisis.

| Channel | What it measures | How it can appear in a crisis | Boundary |

|---|---|---|---|

| Funding liquidity | Access to cash or financing | Borrowers face worse terms, tighter credit, higher collateral demands, or difficulty rolling funding. | It is about obtaining liquidity, not the ease of trading an asset. |

| Market liquidity | Ability to transact without large price impact | Bid-ask spreads widen, depth thins, and large orders move prices more sharply. | It is about trading capacity, not whether a borrower is solvent. |

| Collateral pressure | Ability to support borrowing or margin requirements | Falling collateral values or higher haircuts increase the need for cash or asset sales. | It can amplify funding pressure, but it is not the same as default. |

| Forced selling | Asset sales driven by liquidity need | Sellers accept weaker prices because cash is needed quickly or constraints must be met. | It can move prices, but price decline alone does not prove a liquidity crisis. |

What a Liquidity Crisis Is Not

Not automatically insolvency: an illiquid institution may have assets that exceed liabilities but still struggle to access cash quickly. An insolvent institution has a deeper balance-sheet problem.

Not simply low volume: volume measures activity, not necessarily depth, resilience, or price impact. High volume can also appear during forced selling.

Not automatically a recession forecast: liquidity stress can raise financial-system risk, but it does not mechanically determine the path of the economy.

Not a market-direction signal: liquidity crisis language should not be converted into a direct equity, bond, currency, or crypto trading instruction.

Liquidity Crisis, Liquidity Risk, and Liquidity Spiral

Liquidity crisis, liquidity risk, and liquidity spiral are related, but they do not describe the same thing.

| Concept | Meaning | Relationship to a liquidity crisis |

|---|---|---|

| Liquidity risk | Exposure to the possibility that liquidity may not be available when needed. | Risk can exist before a crisis. A crisis is the stress state where the risk becomes active. |

| Liquidity crisis | A stress condition where liquidity demand exceeds practical access to cash, funding, or liquid markets. | The central state connecting funding pressure, market depth deterioration, and forced selling. |

| Liquidity spiral | A reinforcing loop where funding pressure, asset sales, price declines, and collateral stress feed on each other. | A possible escalation path during crisis conditions, not every liquidity crisis by default. |

Practical Scenario

A common liquidity-stress scenario begins when funding terms worsen and collateral demands rise. Participants that need cash may sell assets into thinner markets. If those sales create larger price impact, collateral values can fall further, which may increase margin pressure and force additional selling.

The important interpretation is not that every price decline is a liquidity crisis. The stronger signal is the combination of funding pressure, weaker trading depth, rising price impact, and liquidity-driven selling.

Why the Distinction Matters

Liquidity crisis analysis helps separate price movement from market functioning. A market can fall for many reasons, including growth expectations, valuation changes, policy repricing, or risk aversion. Liquidity stress becomes a separate concern when participants struggle to obtain funding or transact without unusually large price impact.

The distinction also prevents overreading single indicators. Volume, volatility, spreads, funding terms, market depth, collateral pressure, and forced selling each describe part of the liquidity picture. A stronger interpretation usually requires several channels to point in the same direction.

Related Concepts

Funding liquidity describes access to financing and cash when obligations need to be met.

Market liquidity describes whether assets can trade without large price impact.

Liquidity risk describes exposure to the possibility that liquidity will not be available when needed.

Liquidity spiral describes the reinforcing feedback loop that can develop when funding pressure and market liquidity deterioration interact.

How to measure market liquidity separates spreads, depth, volume, price impact, and resiliency.

FAQ

Is a liquidity crisis the same as insolvency?

No. A liquidity crisis concerns access to cash, funding, or liquid markets under stress. Insolvency concerns whether assets or expected cash flows are insufficient to cover liabilities. The two can interact, but they are not the same concept.

Does a liquidity crisis always mean a recession is coming?

No. Liquidity stress can increase financial-system risk, but it does not automatically forecast a recession. The broader interpretation depends on credit conditions, policy response, balance-sheet strength, and whether stress spreads across markets.

Can high trading volume still occur during weak liquidity?

Yes. High volume can occur when many participants are forced to transact. Liquidity is stronger when trades can be absorbed with limited price impact, enough depth, and resilient order flow.

When does a liquidity crisis become a liquidity spiral?

A liquidity crisis can become a liquidity spiral when funding pressure, asset sales, falling prices, collateral pressure, and margin demands reinforce one another. Not every liquidity crisis reaches that feedback-loop stage.