Liquidity affects markets by changing how easily money, credit, and risk can move through the system. Easier financing, stronger trading depth, wider credit availability, tighter spreads, and higher balance-sheet capacity can support risk-taking. Tighter liquidity can weaken depth, raise volatility, restrict leverage, and reduce confidence. The effect is conditional: liquidity shapes the market environment, but it does not mechanically predict asset prices.

Liquidity is not one market force. A liquid market, an easy financing environment, central-bank balance-sheet support, and loose financial conditions can all affect prices differently. The useful question is not only whether liquidity is high or low. The useful question is which liquidity channel is changing and what market process it affects.

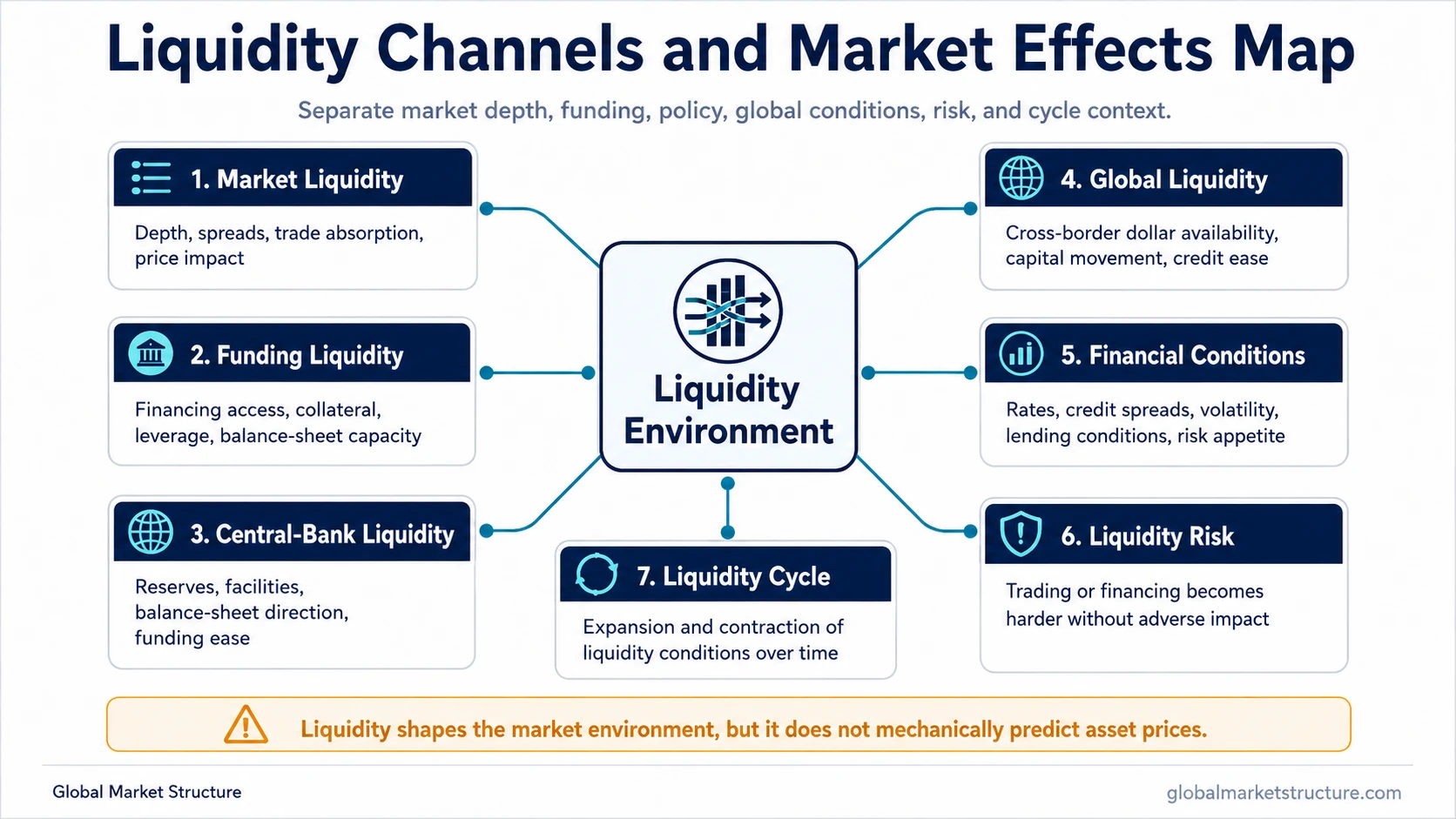

Liquidity Is Not One Market Force

In market-structure analysis, liquidity can describe several related but different conditions. Broad liquidity describes the ease with which cash, credit, and risk capacity move through the financial system. Market liquidity is narrower: it describes the ability to transact without causing large price impact.

Funding liquidity describes access to financing, collateral, leverage, and balance-sheet capacity. Central-bank liquidity describes the policy and balance-sheet channel. Global liquidity and financial conditions describe broader system-wide pressure across credit, rates, asset prices, and risk appetite.

Liquidity Channels and Market Effects

The same word can point to different market mechanisms. The table below separates the main liquidity channels so the interpretation does not collapse into a single “more liquidity means higher prices” shortcut.

| Liquidity channel | What changes | Market effect to watch | Deeper route | Misread to avoid |

|---|---|---|---|---|

| Market liquidity | Depth, bid-ask spreads, trade size absorption, and price impact. | Wider spreads, thinner order books, higher transaction costs, sharper price moves. | Market Liquidity | Assuming high volume always means a market is truly liquid. |

| Funding liquidity | Financing availability, collateral pressure, leverage, and balance-sheet capacity. | Reduced risk-taking, forced deleveraging pressure, weaker ability to hold positions. | Funding Liquidity | Confusing easy trading conditions with easy financing conditions. |

| Central-bank liquidity | Policy operations, reserves, balance-sheet direction, and liquidity facilities. | Changes in the broader financing environment and risk appetite. | Central-Bank Liquidity | Treating central-bank liquidity as an automatic asset-price signal. |

| Global liquidity | Cross-border liquidity, dollar availability, capital movement, and system-wide credit ease. | Pressure or support across global risk assets, currencies, commodities, and funding markets. | Global Liquidity | Reading one domestic indicator as the whole global liquidity picture. |

| Financial conditions | Credit spreads, rates, asset prices, volatility, lending standards, and risk appetite. | Whether the market environment is becoming easier or more restrictive. | Financial Conditions | Reducing financial conditions to only interest rates or only central-bank policy. |

| Liquidity risk | The chance that trading or financing becomes difficult without adverse market impact. | Sharp price gaps, weaker execution depth, funding stress, or sudden spread widening. | Liquidity Risk | Assuming calm prices mean liquidity risk is absent. |

| Liquidity cycle | The expansion and contraction of liquidity conditions over time. | Shifts in risk appetite, credit availability, leverage, and market resilience. | Liquidity Cycle | Treating a cycle backdrop as a short-term timing tool. |

How Market Liquidity Affects Prices and Volatility

Market liquidity affects how easily buyers and sellers can transact. When depth is strong and spreads are tight, large orders can be absorbed with less price impact. When depth is weak, the same order size can move prices more aggressively because fewer counterparties are available at nearby prices.

Low market liquidity can increase volatility because prices have to move farther to find willing buyers or sellers. That does not mean volatility always comes from poor liquidity. It means poor liquidity can make price movement less stable when order flow becomes one-sided.

How Funding Liquidity Affects Risk-Taking and Leverage

Funding liquidity affects markets through the ability of participants to finance positions, post collateral, maintain leverage, and use balance sheets. When financing is available on easier terms, risk-taking can expand because participants have more capacity to hold assets and absorb volatility.

When funding becomes harder, the pressure can move through markets even before a headline crisis appears. Higher collateral costs, tighter credit, lower leverage capacity, and weaker balance-sheet flexibility can force participants to reduce exposure or avoid new risk. That process can reduce demand for risk assets and weaken market depth at the same time.

A Simple Liquidity Pressure Scenario

A market may appear calm while funding conditions tighten beneath the surface. If collateral costs rise, credit spreads widen, and market depth falls, liquidity pressure can show up through wider bid-ask spreads and sharper price moves. That does not prove a crash is coming, but it changes the risk environment because participants have less flexibility to finance risk and absorb forced selling.

How Central-Bank Liquidity and Financial Conditions Affect the Environment

Central-bank liquidity can affect markets by changing the availability of reserves, the direction of balance-sheet policy, and the ease of short-term funding. It is usually better read as an environment channel than as a direct forecast for asset prices.

Financial conditions widen the lens. Credit spreads, interest rates, volatility, lending conditions, asset prices, and risk appetite can either reinforce or offset a liquidity impulse. A liquidity-positive policy backdrop may have a different effect if inflation pressure, valuation stress, or credit risk is also rising.

Why Liquidity Does Not Predict Markets Mechanically

Liquidity shapes the market environment, but it does not provide a standalone timing signal. More liquidity does not always mean risk assets rise, and less liquidity does not automatically mean a crash.

The source of liquidity matters. The transmission channel matters. Asset sensitivity matters. Valuation, earnings, inflation, rates, credit stress, policy reaction, and asset-specific flows can offset or reshape the effect of liquidity.

The useful question is not “is liquidity high or low?” The stronger question is “which liquidity channel is changing, and what market process does it affect?”

Where to Go Next

Need the base concept? Start with liquidity to separate broad liquidity from narrower market and funding concepts.

Need trading depth? Market Liquidity covers spreads, depth, price impact, and transaction conditions.

Need financing and leverage? Funding Liquidity covers collateral, financing access, leverage, and balance-sheet capacity.

Need stress conditions? Liquidity Risk covers conditions where trading or financing becomes difficult without adverse impact.

Need the policy channel? Central-Bank Liquidity covers reserves, balance sheets, facilities, and policy transmission.

Need the broad regime view? Global Liquidity, Financial Conditions, and Liquidity Cycle connect liquidity pressure with the wider market environment.

FAQ

How does liquidity affect markets?

Liquidity affects markets by changing financing conditions, trading depth, credit availability, spreads, volatility, risk appetite, and balance-sheet capacity. It shapes the environment in which assets trade, but it does not mechanically predict price direction.

Is market liquidity the same as funding liquidity?

No. Market liquidity is about the ability to trade without large price impact. Funding liquidity is about access to financing, collateral, leverage, and balance-sheet capacity. They can interact, but they are not the same concept.

Does central-bank liquidity always support asset prices?

No. Central-bank liquidity can ease the broader environment, but asset prices also depend on valuation, earnings, inflation, credit stress, risk appetite, and how liquidity is transmitted through the system.

Why can low liquidity increase volatility?

Low liquidity can increase volatility because fewer buyers or sellers may be available at nearby prices. When depth is thin, orders can move prices more sharply, especially if market participants are also reducing risk.

Can liquidity be used as a market-timing signal?

Liquidity should not be treated as a standalone market-timing signal. It is better used as an environment variable that must be read alongside rates, credit, inflation, valuation, earnings, and asset-specific flows.