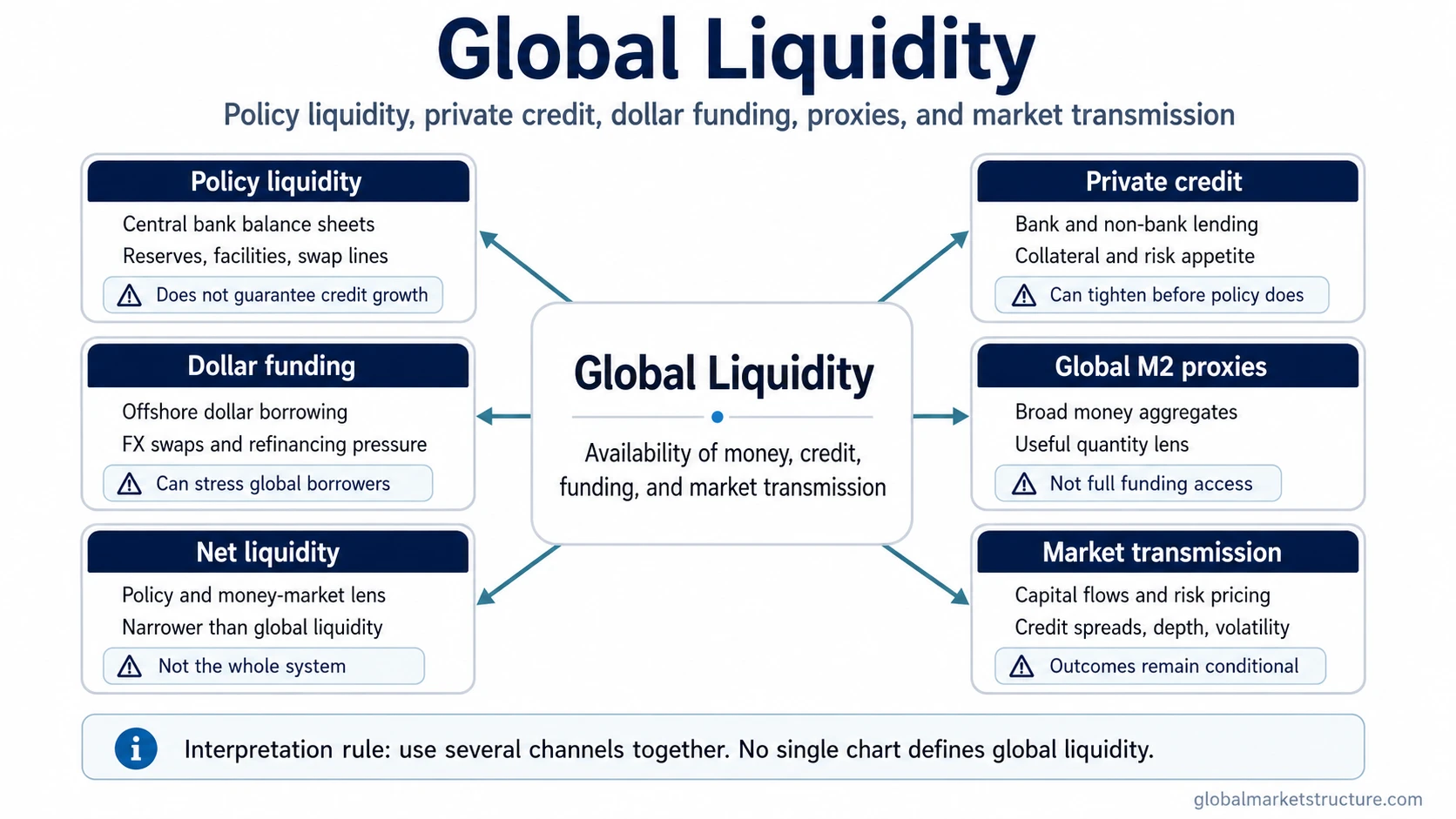

Global liquidity means the broad availability of financing, credit, and usable money across the world economy. For market interpretation, it includes policy liquidity, private credit creation, dollar funding conditions, cross-border bank balance sheets, and the way those channels reach asset markets. It is not one metric, a DXY reading, a global M2 chart, or a mechanical risk-asset signal.

Definition: Global liquidity is the overall ease or tightness of money, credit, and funding conditions across major economies and cross-border markets. It helps describe whether capital can move, financing can roll, credit can expand, and risk can be priced without severe funding pressure.

Liquidity can enter markets through more than one channel. A central bank balance sheet may expand while private lenders remain cautious. Global money supply may rise while offshore dollar funding becomes more expensive. A broad liquidity reading can therefore look supportive on one surface and restrictive on another.

What Global Liquidity Means

Global liquidity is a market-structure concept, not a single official balance. It combines central-bank money, private credit creation, dollar funding access, collateral conditions, and the ease with which capital moves across borders.

Markets do not respond only to how much money exists. They respond to whether that money can be borrowed, transformed into credit, used as collateral, moved across jurisdictions, and absorbed without forced deleveraging or abrupt repricing.

This is why global liquidity sits close to the liquidity cycle. Liquidity can expand, circulate unevenly, become trapped inside specific institutions, or tighten through credit and funding channels before the broad macro story looks obvious.

What Belongs Inside Global Liquidity

A useful global liquidity framework separates the source of liquidity from the channel that transmits it. The source may be a central bank, a commercial bank, a non-bank lender, an offshore dollar market, or a cross-border capital flow. The channel determines how that liquidity reaches borrowers, asset markets, or risk pricing.

| Liquidity source or lens | Main channel | Common observable | Main limitation |

|---|---|---|---|

| Central-bank liquidity | Policy balance sheets, reserves, asset purchases, and liquidity facilities | Central-bank balance sheets, reserves, repo operations, swap lines | Policy liquidity does not automatically become private credit or asset-market buying power. |

| Private credit creation | Bank lending, non-bank lending, collateral reuse, and risk appetite | Credit growth, lending standards, credit spreads, issuance conditions | Private credit can tighten even when headline money supply or policy liquidity looks stable. |

| Dollar funding system | Offshore dollar borrowing, bank balance sheets, FX swaps, and global collateral demand | Funding spreads, FX swap stress, dollar scarcity indicators | Dollar funding pressure can matter even when domestic liquidity measures look benign. |

| Global M2 and money-supply proxies | Broad money growth across major economies | Aggregated M2 measures, local currency money aggregates | M2 is a proxy for money quantity, not a complete measure of funding access or credit transmission. |

| Market transmission | Capital flows, collateral conditions, risk appetite, and balance-sheet capacity | Market depth, volatility, credit spreads, cross-asset correlations | Asset prices can react differently depending on growth, inflation, earnings, policy expectations, and positioning. |

The dollar channel is especially important because the U.S. dollar is a dominant funding and settlement currency. A reserve currency role means dollar liquidity can affect borrowers and institutions outside the United States, not only domestic U.S. markets.

Global Liquidity Is Not One Metric

The most common mistake is treating one chart as the full answer. Global M2, central-bank balance sheets, DXY, credit spreads, and funding indicators can each reveal part of the liquidity environment, but none of them fully defines global liquidity by itself.

Global M2 is not global liquidity. It can help show broad money growth, but it does not fully capture lending standards, offshore dollar stress, collateral conditions, cross-border funding access, or whether money is reaching risk markets.

DXY is not global liquidity. A rising dollar can reflect dollar demand, U.S. rate differentials, risk aversion, or relative growth expectations. It can point to pressure in the system, but it is not a complete liquidity measure.

QE is not a guarantee of rising asset prices. Quantitative easing can change reserves, duration supply, and risk perception, but market outcomes still depend on credit transmission, valuation, growth expectations, inflation, earnings, and investor positioning.

Net liquidity is narrower than global liquidity. Net liquidity usually focuses on selected policy balance-sheet and money-market adjustments. Global liquidity is broader because it also includes private credit, cross-border funding, dollar markets, and market transmission.

How Global Liquidity Reaches Markets

Global liquidity reaches markets through balance sheets. Central banks can influence reserves and funding backstops, but banks and non-bank lenders decide whether financing is actually extended. Investors then decide whether liquidity is used to absorb risk, refinance debt, support collateral, or retreat into safer assets.

One channel runs through the eurodollar system, where offshore dollar credit and bank balance sheets can affect global funding conditions. A borrower outside the United States may still depend on dollar financing, and that dependence can become important when dollar funding tightens.

Another channel appears through FX funding markets. The cross-currency basis can help show when borrowing dollars through swaps becomes more expensive or more strained. It is not the whole liquidity story, but it can be a useful pressure gauge inside the dollar-funding channel.

The market impact depends on the combination. Easy policy liquidity with weak private credit growth can produce a different environment from strong credit creation with rising funding stress. That is why global liquidity is better read as a set of channels rather than a single bullish or bearish label.

Illustrative Scenario: Stable Policy Liquidity, Tighter Funding

Consider a generic situation where central-bank liquidity looks stable, but offshore dollar funding becomes more expensive and credit spreads begin to widen. A broad money-supply chart may not show immediate stress, yet borrowers that rely on dollar funding may face tighter refinancing conditions.

The market interpretation is not that global liquidity has produced a direct trading signal. The more useful reading is that one channel of liquidity has tightened while another appears stable. If private credit also weakens and market depth deteriorates, the liquidity environment becomes more restrictive even without a simple one-metric confirmation.

A mixed-channel scenario separates where liquidity is created, where it is blocked, and how the blockage can move from funding markets into credit pricing and cross-asset behavior.

Common Misreadings of Global Liquidity

A broad liquidity label can become misleading when it is used as a market forecast. More liquidity can support risk-taking under some conditions, but it does not remove valuation risk, earnings risk, inflation risk, political risk, or positioning risk. Less liquidity can pressure markets under some conditions, but it does not guarantee immediate risk-off behavior.

| Misreading | Why it is incomplete | Better interpretation |

|---|---|---|

| Global liquidity is just global M2. | M2 measures money quantity more than funding access or credit transmission. | Use M2 as one proxy, then check credit, funding, and market transmission. |

| A stronger dollar proves liquidity is tight. | The dollar can rise for several reasons, including relative growth or rate expectations. | Use DXY as context, not as a complete liquidity diagnosis. |

| QE means risk assets should rise. | Policy liquidity does not always become private credit or risk-taking. | Check whether liquidity is moving through banks, credit markets, and investor balance sheets. |

| Credit spreads define the whole liquidity environment. | Credit spreads show risk pricing, not every liquidity source. | Read credit spreads alongside policy liquidity, funding markets, and capital flows. |

Related Liquidity Concepts

Global liquidity is the broad concept. Liquidity cycle, reserve-currency structure, net liquidity, offshore dollar credit, and FX funding indicators each describe narrower parts of the same liquidity environment.

The liquidity cycle explains how liquidity conditions expand, tighten, and transmit across time. Reserve-currency structure explains why dollar-based funding can matter globally. Net liquidity narrows the focus to selected policy and money-market balances. The eurodollar system explains offshore dollar credit creation, while cross-currency basis focuses on one observable inside FX funding markets.

Keeping those boundaries clear prevents global liquidity from becoming an overloaded label. The strongest use of the concept is to map the channels, compare their direction, and avoid turning any one proxy into a complete market signal.

FAQ

What is global liquidity?

Global liquidity is the broad availability of money, credit, and funding across major economies and cross-border markets. It includes policy liquidity, private credit creation, dollar funding conditions, and the way those channels reach markets.

Is global liquidity the same as global M2?

No. Global M2 can be a useful money-supply proxy, but it does not fully capture credit creation, lending standards, offshore dollar funding, collateral pressure, or market transmission.

Does higher global liquidity always push asset prices higher?

No. Easier liquidity can support risk-taking under some conditions, but asset prices also depend on growth, inflation, valuation, earnings, policy expectations, positioning, and risk perception.

How is global liquidity different from net liquidity?

Net liquidity is usually a narrower policy and money-market lens. Global liquidity is broader because it also includes private credit, cross-border funding, dollar liquidity, and market transmission channels.

Why does dollar funding matter for global liquidity?

Dollar funding matters because many borrowers, banks, and markets outside the United States rely on dollar financing. When dollar funding becomes harder or more expensive, global liquidity conditions can tighten through refinancing, collateral, and credit channels.