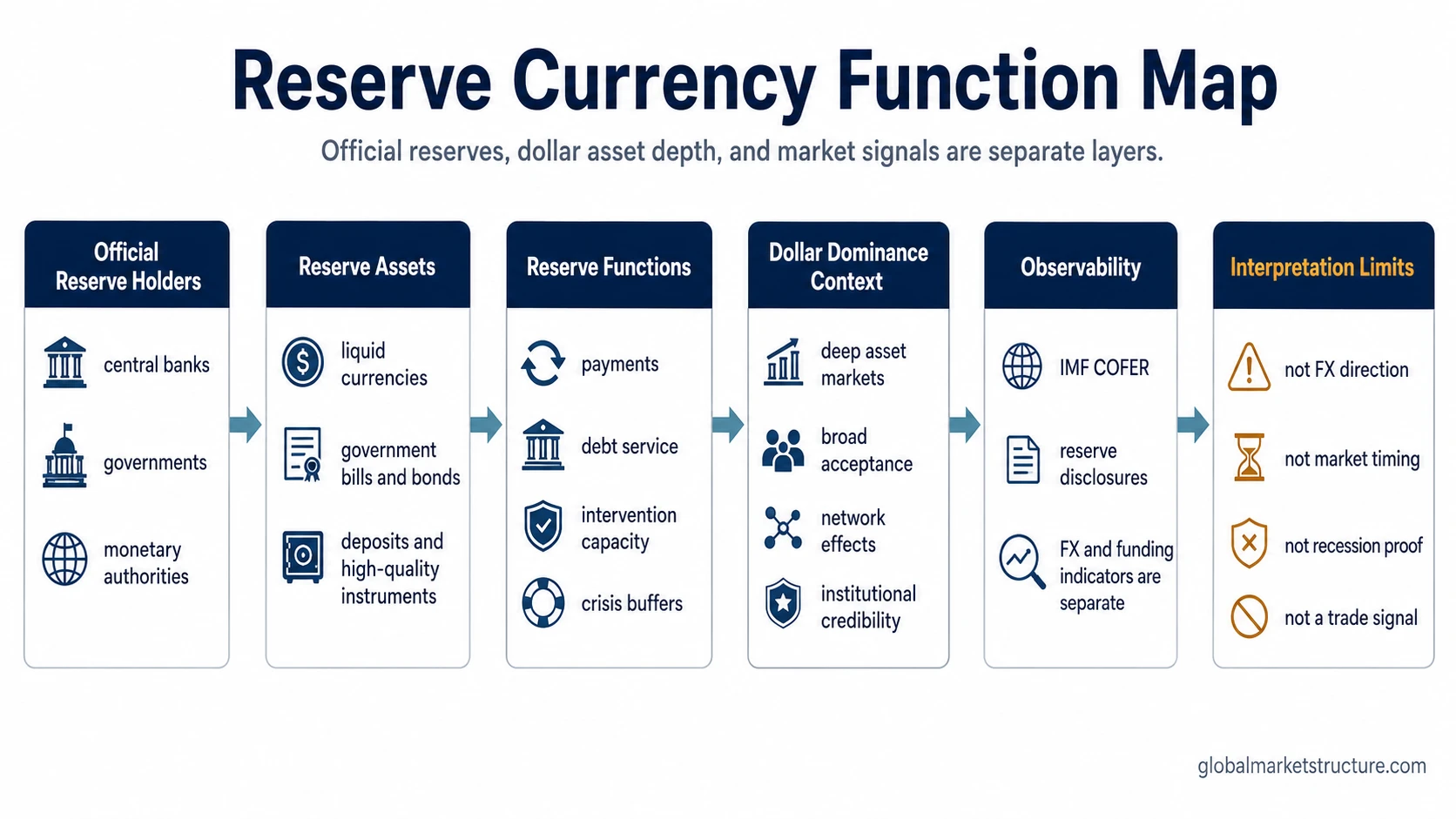

A reserve currency is a currency held by governments, central banks, or monetary authorities as part of their foreign-exchange reserves. It is used because it is liquid, widely accepted, and practical for international payments, debt service, intervention, and crisis buffers.

In IMF COFER data for 2025Q4, the U.S. dollar still held the largest share of allocated official foreign-exchange reserves. That dominance is best read as a structural reserve-system fact, not as a dollar exchange-rate forecast.

What a reserve currency means

A reserve currency is not simply a popular currency or a strong exchange rate. It is a currency that official reserve managers can hold and use when they need reliable access to international purchasing power.

- Holder: governments, central banks, monetary authorities, and reserve managers.

- Function: foreign-exchange reserves, payment capacity, intervention capacity, and stability buffers.

- Required qualities: liquidity, convertibility, credibility, and access to deep asset markets.

- Market relevance: reserve status supports structural demand for safe and liquid assets, especially when global institutions need dependable collateral and settlement capacity.

The important distinction is that reserve-currency status describes monetary infrastructure. It does not automatically describe the next move in the exchange rate, the next equity-market trend, or the timing of a recession.

Why reserve currencies exist

Countries hold foreign-exchange reserves because they may need to settle international obligations, stabilize currency markets, service external debt, or preserve confidence during stress. The reserve asset must be usable when liquidity matters most.

A currency becomes useful in that role when other participants are willing to accept it, when large liquid asset markets exist in that currency, and when official holders can transact without severely disrupting prices. This is why reserve-currency status is closely tied to safe-asset demand and financial-market depth.

How reserve-currency status works

- Official reserve holders need liquid foreign assets. Central banks and governments hold reserves to support payments, intervention, and confidence.

- Reserve assets need safety and market depth. A reserve currency becomes more useful when there are deep markets for government bonds, bills, deposits, and other high-quality instruments.

- Usability reinforces demand. The more widely a currency is used in trade, finance, debt issuance, and settlement, the more useful it becomes as a reserve asset.

- Dollar asset depth supports dollar reserve demand. The U.S. Treasury market and broader dollar financial system give reserve managers a large pool of liquid dollar assets.

- Reserve demand becomes part of dollar-liquidity structure. Official reserve demand can support the role of dollar assets in global balance sheets, collateral, and liquidity management.

- Interpretation still needs context. Reserve status must be read alongside funding conditions, FX moves, policy, credit, and cross-asset behavior.

Why the U.S. dollar is the main reserve currency

The dollar’s reserve role is not explained by one factor. It reflects a combination of asset-market depth, global acceptance, institutional credibility, payment use, financial contracts, and network effects.

Official reserve managers do not only need a currency label. They need instruments that can absorb large holdings, trade in size, remain liquid in stress, and connect to the global financial system. Dollar assets have historically been treated as one of the deepest and most usable reserve-asset pools, which helps explain why reserve status changes slowly.

This does not make dollar dominance permanent. It means reserve status changes slowly because the alternatives must compete not only with the dollar exchange rate, but with the depth and usability of the wider dollar asset system.

What reserve currency is and is not

| Reserve-currency concept | What it means | What it does not mean |

|---|---|---|

| Official reserve infrastructure | A currency used by reserve managers for foreign-exchange reserves and official liquidity needs. | It is not a guarantee that the currency price must rise. |

| Safe and liquid asset demand | Reserve holders need assets that can be held, sold, pledged, or used in size. | It is not proof that every dollar asset is risk-free or always liquid in every market condition. |

| Dollar reserve dominance | In IMF COFER data for 2025Q4, the dollar held the largest share of allocated official foreign-exchange reserves. | It is not proof that the dollar cannot weaken in FX markets. |

| Reserve-share data | Data such as IMF COFER can show currency composition in official FX reserves. | It is not a live trading signal and does not by itself prove allocation intent. |

| Macro and liquidity structure | Reserve status helps explain global demand for dollar liquidity and safe assets. | It is not the whole of global liquidity, private funding stress, or market timing. |

Reserve currency versus the dollar exchange rate

Reserve-currency status and exchange-rate direction are separate questions. A currency can remain dominant in official reserves while its exchange rate weakens for cyclical reasons such as changing rate expectations, valuation pressure, improving foreign growth, or shifting risk appetite.

A generic scenario makes the boundary clear: the dollar can decline against other major currencies while still remaining the largest reserve currency if official reserve managers continue to hold deep, liquid dollar assets. The FX move may describe relative price pressure. It does not automatically describe a structural loss of reserve status.

Reserve currency versus dollar funding liquidity

Reserve-currency status concerns official reserve holdings and the role of a currency in the international monetary system. Dollar funding liquidity concerns whether banks, borrowers, dealers, and leveraged participants can obtain dollar financing when they need it.

The two can interact, but they are not the same. A currency can be dominant in official reserves while private dollar funding conditions tighten. Funding stress is usually read through financing spreads, swap markets, cross-currency basis, dealer balance-sheet conditions, and collateral pressure rather than reserve-share data alone.

Reserve currency versus the eurodollar system

The eurodollar system refers to offshore dollar banking, deposits, liabilities, and balance-sheet intermediation outside the domestic U.S. banking system. Reserve-currency status refers to official reserve holdings and the usability of a currency for reserve management.

Both concepts involve the global role of the dollar, but they describe different layers. Reserve currency focuses on official reserve assets. The eurodollar system focuses on offshore dollar credit and funding plumbing.

Reserve currency versus global liquidity

Global liquidity is broader than reserve-currency composition. It can include central-bank balance sheets, bank credit, funding conditions, collateral capacity, dollar availability, cross-border capital flows, and market liquidity.

Reserve-currency status is one part of the global dollar-liquidity structure, not the entire structure. A strong reserve role can support demand for dollar assets, but liquidity conditions can still tighten if funding markets, credit spreads, collateral availability, or policy conditions deteriorate.

How reserve-currency use can be observed

Reserve-currency use is most directly observed through official reserve-composition data, especially IMF COFER. COFER reports the currency composition of official foreign-exchange reserves at the aggregate level and is the main reference point for reserve-share claims.

Several observations can matter, but each has a limitation:

- COFER reserve shares: useful for official reserve composition, but exact values should be tied to a release date.

- Central-bank reserve disclosures: useful where available, but not all countries disclose the same level of detail.

- Treasury and dollar safe-asset depth: relevant to reserve usability, but market depth is not identical to reserve allocation.

- FX moves: useful for dollar price behavior, but not the same as reserve-status change.

- Funding indicators: useful for private dollar stress, but separate from official reserve composition.

What reserve-currency status does not prove

- It does not prove the currency must rise.

- It does not prove the currency cannot fall.

- It does not prove de-dollarization is happening.

- It does not prove a recession is near.

- It does not forecast equity, bond, commodity, or crypto prices.

- It does not replace funding, credit, policy, and cross-asset confirmation.

Reserve-currency status is better treated as a structural monetary condition. It can shape the background demand for dollar assets, but the market interpretation still depends on why the dollar is moving, whether liquidity is improving or tightening, and whether credit and cross-asset signals confirm the same regime.

How to read reserve-currency status in market structure

The reserve role of the dollar helps explain why dollar assets can remain central to global balance sheets even when the dollar exchange rate is under cyclical pressure. It also helps explain why changes in dollar availability, collateral demand, and safe-asset preference can matter beyond the United States.

The cleanest interpretation separates three layers:

- Structural role: whether a currency is widely held and usable as an official reserve asset.

- Funding condition: whether private participants can access the currency through banking and market channels.

- Market response: how FX, rates, credit, commodities, equities, and risk appetite react under current conditions.

When dollar behavior changes across regimes, dollar smile theory can help frame why the dollar may strengthen in different environments. That framework still does not turn reserve-currency status into a standalone forecast.

Related concepts

Reserve currency belongs inside the wider dollar and global liquidity structure. The most important related concepts are private dollar funding, offshore dollar banking, global liquidity, and dollar behavior across regimes.

- Dollar funding liquidity: explains access to dollar financing in private markets.

- Eurodollar system: explains offshore dollar deposits, liabilities, and bank balance-sheet plumbing.

- Global liquidity: explains broader liquidity conditions across central banks, credit, funding, collateral, and capital flows.

- Dollar smile theory: explains why the dollar may behave differently across growth, stress, and relative-strength regimes.

Reserve currency FAQ

Does reserve-currency status mean the dollar cannot fall?

No. Reserve-currency status describes official reserve use and monetary infrastructure. The dollar can weaken in FX markets while still remaining the dominant reserve currency.

Is reserve currency the same as dollar funding liquidity?

No. Reserve currency concerns official reserve holdings. Dollar funding liquidity concerns access to dollar financing in private markets.

Is the eurodollar system the same as reserve-currency status?

No. The eurodollar system describes offshore dollar banking and liabilities. Reserve-currency status describes the official use of a currency in foreign-exchange reserves.

Does reserve-currency status predict markets?

No. It can help explain structural dollar demand, but it does not by itself predict asset prices, recessions, or market timing.