The eurodollar system is the offshore U.S. dollar banking network: dollar deposits, liabilities, and lending channels held outside the domestic U.S. banking perimeter. Eurodollar does not mean euro currency. The system matters because it can support or strain global dollar funding, but it is not standalone proof of a crisis, recession, equity direction, or trade timing.

Definition: The eurodollar system is offshore dollar funding infrastructure: U.S. dollar liabilities and lending channels outside the domestic U.S. banking perimeter. It is not the euro currency, eurodollar futures, or a standalone market signal.

What Is the Eurodollar System?

The eurodollar system is a network of dollar-denominated deposits, liabilities, loans, and wholesale funding relationships outside the domestic U.S. banking perimeter. A bank outside the United States can accept dollar deposits, create dollar liabilities, lend dollars, or intermediate dollar funding without those balances being simple domestic U.S. bank deposits.

The core idea is jurisdictional and balance-sheet based. The dollars are U.S. dollars, but the banking activity sits offshore or outside the direct domestic deposit framework. That makes the system important for global dollar funding because many non-U.S. borrowers, banks, and market participants still need dollars to finance trade, debt, collateral, and cross-border balance sheets.

The eurodollar system is funding plumbing rather than a single exchange, data series, or instrument. Its conditions can affect how dollar liquidity moves through the global financial system, but the broader interpretation depends on confirming evidence from related funding and risk markets.

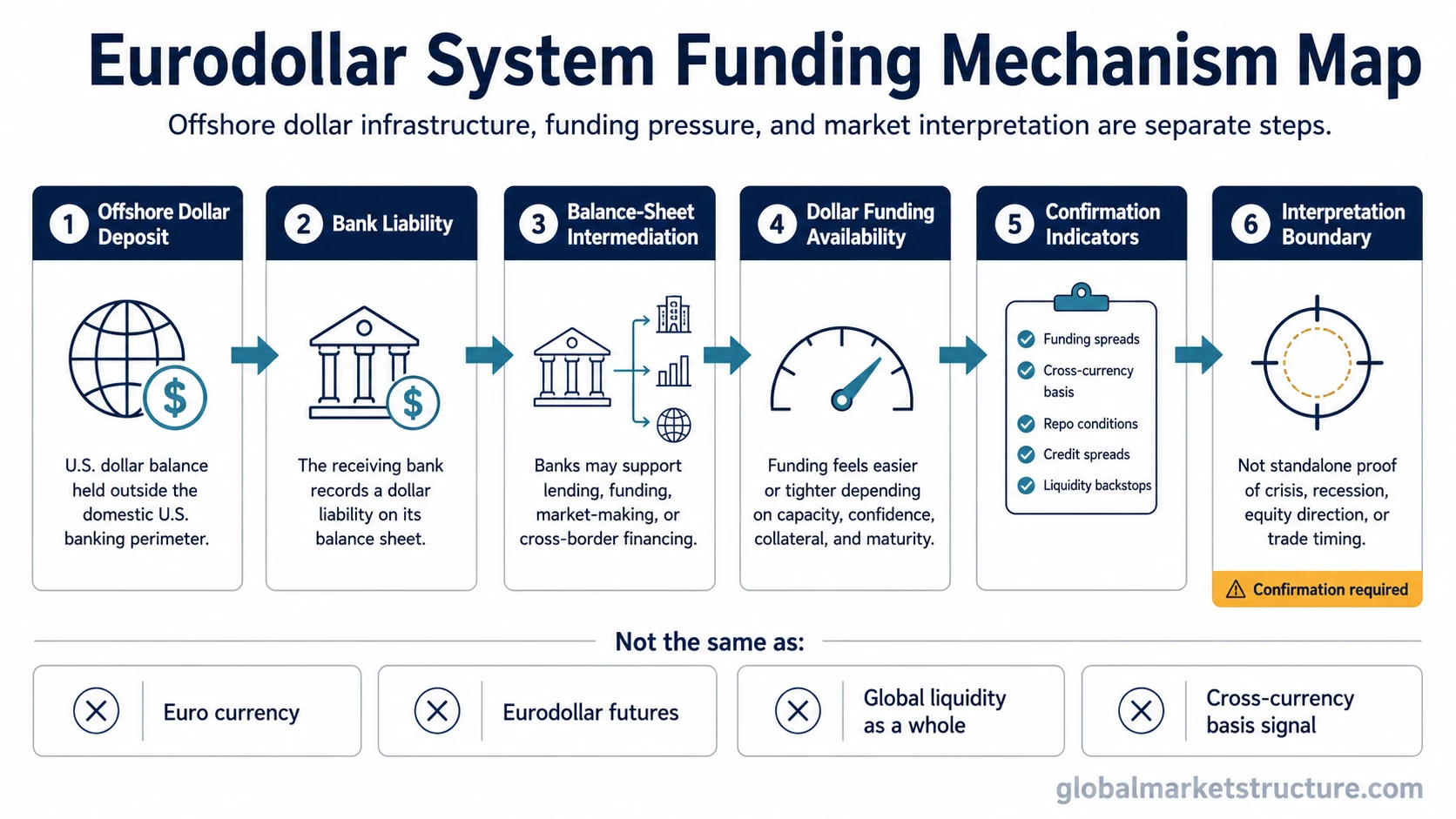

What the Eurodollar System Is Not

| Term | What it means | Boundary against the eurodollar system |

|---|---|---|

| Euro currency | The official currency used by euro-area countries. | Eurodollars are U.S. dollar liabilities outside the domestic U.S. banking perimeter, not euro-denominated money. |

| Eurodollar futures | A legacy interest-rate futures market linked to expectations for short-term dollar rates. | The futures contract was a market instrument. The eurodollar system is the broader offshore dollar banking and funding network. |

| Dollar funding liquidity | The ease, cost, and availability of obtaining dollar funding. | The eurodollar system is part of the infrastructure through which dollar funding can be supplied or strained. |

| Cross-currency basis | A pricing deviation that can reflect pressure in swapping one currency into dollars. | Cross-currency basis can be a related funding-pressure signal, not the offshore dollar banking system itself. |

| Global liquidity | A broader condition shaped by central banks, credit creation, collateral, funding markets, and risk appetite. | The eurodollar system is one important dollar-funding channel inside the wider liquidity environment. |

| Reserve currency status | The role of a currency in reserves, trade invoicing, debt, and global settlement. | Dollar reserve status helps explain dollar demand, but the eurodollar system describes offshore dollar intermediation. |

How the Eurodollar System Works

- Offshore dollar deposit: A dollar balance is held outside the domestic U.S. banking system.

- Bank liability: The receiving bank records a dollar liability on its balance sheet.

- Dollar intermediation: The bank may use dollar liabilities to support lending, funding, market-making, or cross-border financing.

- Balance-sheet constraint: The system depends on bank willingness and capacity to expand or maintain dollar balance sheets.

- Funding pressure: Stress can appear when dollar demand rises faster than available funding, collateral capacity, or balance-sheet appetite.

- Market confirmation: Related indicators such as funding spreads, cross-currency basis, credit spreads, repo conditions, and central-bank liquidity facilities help confirm whether pressure is local or systemic.

The mechanism is not the same as a central bank printing domestic money. Offshore dollar intermediation depends on balance sheets, counterparties, collateral, maturity, regulation, and confidence. The system can expand when banks are willing to intermediate dollar claims and contract when balance-sheet capacity or funding confidence weakens.

Why the Eurodollar System Matters for Dollar Funding

Global borrowers often need dollars even when their revenues, assets, or banking relationships sit outside the United States. Corporates may use dollars for trade finance, banks may need dollars for wholesale funding, and investors may need dollars for collateral, settlement, or hedging. Offshore dollar banking helps connect that demand with dollar supply.

When the eurodollar system works smoothly, offshore dollar funding can appear abundant because banks and market participants are willing to intermediate dollar claims. When conditions tighten, the same network can transmit pressure through higher funding costs, shorter maturities, weaker credit availability, or greater demand for dollar liquidity backstops.

For market interpretation, the key issue is whether offshore dollar balance-sheet capacity is expanding, stable, or constrained, and whether related funding indicators point to the same pressure.

Interpretation note: A eurodollar signal is stronger when it appears alongside pressure in related funding markets. It is weaker when the evidence is isolated, temporary, or contradicted by credit, repo, swap, central-bank liquidity, or broader risk indicators.

How It Can Show Up in Market Interpretation

Practical scenario: A non-U.S. bank needs dollars to fund dollar assets and client activity. If offshore dollar funding becomes harder to obtain, the bank may shorten maturities, pay more for dollar funding, reduce balance-sheet activity, or seek alternative channels. That pressure matters more when related funding markets show the same strain.

This scenario does not automatically prove a crisis. It becomes more meaningful when multiple funding indicators move together. Offshore dollar pressure carries more weight if cross-currency basis becomes more strained, credit spreads widen, repo conditions tighten, and central-bank dollar facilities become more relevant at the same time.

The distinction matters because the eurodollar system is infrastructure, while market interpretation depends on evidence. Infrastructure can transmit pressure, but the pressure still needs to be observed through prices, spreads, funding costs, balance-sheet behavior, and policy responses.

Common Misreadings

Misreading 1: Treating eurodollar as euro currency. Eurodollars are U.S. dollar claims outside the domestic U.S. banking perimeter.

Misreading 2: Treating the eurodollar system as eurodollar futures. Futures are instruments. The system is broader dollar funding infrastructure.

Misreading 3: Treating offshore dollar pressure as automatic crisis proof. Funding stress can matter, but it needs confirmation from related markets and policy channels.

Misreading 4: Treating the eurodollar system as all global liquidity. Global liquidity also includes central-bank balance sheets, domestic credit creation, collateral conditions, fiscal flows, and risk appetite.

How to Avoid False Readings

Limit: The eurodollar system is an interpretation input, not a standalone forecast. It does not, by itself, prove recession timing, equity-market direction, credit-market breakdown, or the correct trade expression.

A safer interpretation separates three layers: the structure of offshore dollar banking, the funding conditions visible in market prices or balance sheets, and the broader macro conclusion. Collapsing those layers can turn a real funding concept into an unsupported market call.

| Reading layer | Question to ask | What can go wrong |

|---|---|---|

| Structure | Is the issue about offshore dollar liabilities, lending, and balance-sheet intermediation? | The concept gets confused with euro currency, futures, or a generic liquidity story. |

| Funding conditions | Are funding costs, spreads, collateral conditions, or swap markets confirming pressure? | One noisy signal is treated as a complete funding diagnosis. |

| Macro interpretation | Does the pressure connect with credit, rates, central-bank liquidity, DXY, or risk appetite? | A funding observation becomes an unsupported recession or equity-direction claim. |

Related Concepts

Dollar funding liquidity focuses on the availability, cost, and stress of obtaining dollars. It is the closest adjacent concept when the question shifts from offshore dollar infrastructure to funding pressure.

Cross-currency basis is useful when dollar demand is visible through the cost of swapping other currencies into dollars. It is a pricing signal, not the eurodollar system itself.

Global liquidity is broader than offshore dollar banking because it includes central-bank liquidity, credit creation, collateral conditions, and risk appetite across markets.

Reserve currency role explains why dollar demand is structurally important across trade, reserves, debt, and settlement, while the eurodollar system explains one major channel for offshore dollar intermediation.