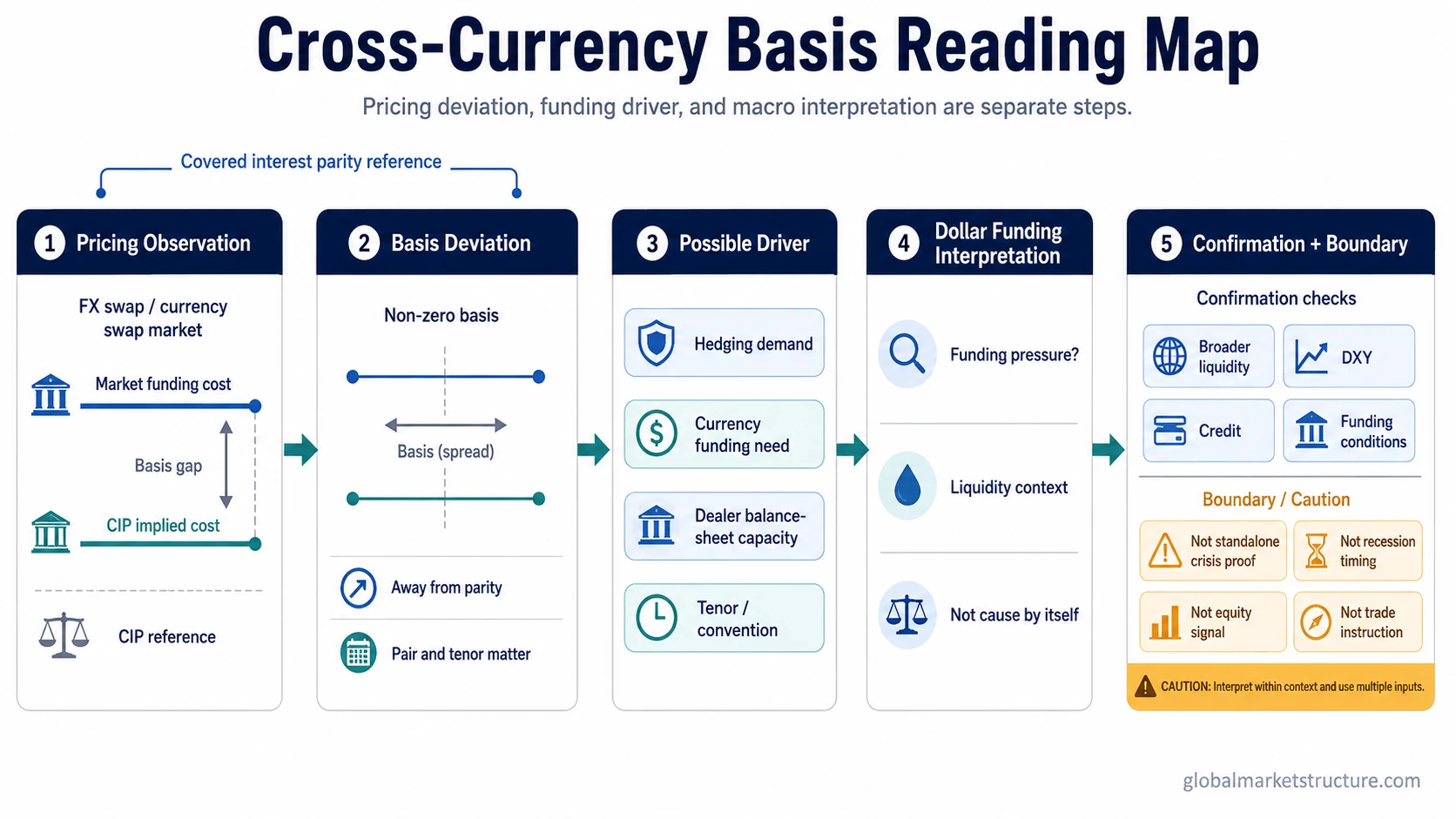

Cross-currency basis is the spread or deviation that appears when the market cost of obtaining one currency through FX swaps or cross-currency swaps differs from what covered interest parity would imply. It can help interpret dollar funding pressure, but it is not automatic proof of a dollar shortage, crisis, recession, equity move, or trade signal.

In simple terms: cross-currency basis compares real swap-market funding pricing with the theoretical relationship between spot exchange rates, forward exchange rates, and interest rates.

Why it matters: a persistent basis can show that currency funding is not being priced as if markets were frictionless. That gap may reflect hedging demand, funding pressure, balance-sheet constraints, tenor effects, market stress, or quote conventions.

What it does not prove: a basis move does not, by itself, identify the cause of the pressure or predict broader market direction.

What Cross-Currency Basis Measures

Cross-currency basis measures the difference between a market-implied currency funding cost and the funding cost implied by covered interest parity. Covered interest parity is the relationship that should connect the spot exchange rate, forward exchange rate, and interest-rate difference between two currencies when arbitrage is frictionless.

When real FX swap or cross-currency swap pricing does not line up with that parity relationship, the difference is expressed as basis. A non-zero basis means that obtaining one currency through the swap market is cheaper or more expensive than a simplified parity condition would suggest.

The useful interpretation is not only that a spread exists. The stronger question is why the spread exists: hedging flows, currency demand, balance-sheet usage, tenor, collateral conditions, funding access, and market stress can all change the reading.

How Covered Interest Parity Fits Into Cross-Currency Basis

Covered interest parity links three pieces of pricing: the spot exchange rate, the forward exchange rate, and the interest rates available in each currency. In a simplified frictionless setting, borrowing in one currency, converting it, investing in another currency, and locking the exchange-rate path with a forward should not create a free funding advantage.

Cross-currency basis appears when market pricing does not perfectly match that relationship. The gap can exist because the real market is not frictionless. Banks have balance-sheet limits, collateral costs matter, hedgers are not always balanced on both sides, and demand for one currency can be stronger than demand for another.

The parity relationship is the starting reference point. Macro interpretation comes later, after checking which currency pair, tenor, quote convention, and market conditions are involved.

Why Cross-Currency Basis Exists

Cross-currency basis can exist because the demand to borrow or hedge one currency is not evenly matched by the supply of that currency. When many participants want to obtain dollars through swap markets, the cost of accessing dollars can move away from the level implied by covered interest parity.

Hedging demand is one driver. A foreign investor holding dollar assets may need to hedge currency exposure back into a home currency. A borrower with liabilities in one currency and revenues in another may need to transform cash flows through the swap market. These flows can push swap pricing away from a clean theoretical parity line.

Balance-sheet capacity is another driver. Even when an apparent arbitrage exists, banks and dealers may not be able or willing to absorb unlimited positions. Capital rules, funding costs, collateral requirements, year-end balance-sheet pressure, and risk limits can allow basis to persist.

Tenor and convention also matter. A short-tenor move may reflect near-term funding pressure or balance-sheet date effects. A longer-tenor basis can reflect persistent hedging demand, structural funding preference, or benchmark and curve construction differences. The same sign does not carry the same meaning across every pair and tenor.

How to Read Cross-Currency Basis

The safest reading starts with separation. First identify the observed basis move. Then ask which mechanical driver could explain it. Only after that should the move be connected to dollar funding, liquidity pressure, or broader risk conditions.

| Observed basis move | Possible mechanical driver | Macro interpretation | Confirmation needed | Misread risk |

|---|---|---|---|---|

| Basis moves further from parity in a dollar-related pair | Higher demand to obtain dollars through swaps | Possible tightening in dollar funding conditions | Funding spreads, repo conditions, DXY behavior, credit spreads, and broader liquidity evidence | Reading every move as a dollar shortage without checking pair, tenor, or convention |

| Basis changes sharply around a short date or quarter-end | Balance-sheet or reporting-date pressure | Possible temporary funding or dealer-capacity pressure | Tenor comparison, date effects, money-market pricing, and persistence after the date passes | Treating a short-lived technical pressure as a structural regime shift |

| Longer-tenor basis remains persistent | Structural hedging demand or currency funding imbalance | Possible ongoing preference for one currency funding channel | Cross-tenor curve shape, hedging flows, bank balance-sheet capacity, and related liquidity indicators | Assuming persistence alone proves crisis conditions |

| Basis normalizes toward parity | Improved funding supply, reduced hedging imbalance, or balance-sheet relief | Potential easing in the specific funding channel | Confirmation from broader dollar funding liquidity signals | Assuming one normalized pair means all liquidity stress is gone |

| Basis differs across pairs or tenors | Pair-specific demand, benchmark convention, market depth, or hedging flow | Fragmented funding pressure rather than a single global signal | Comparison across currency pairs, tenor buckets, and adjacent liquidity measures | Using one pair as a universal global liquidity proxy |

Cross-Currency Basis and Dollar Funding

Cross-currency basis is often watched because dollar funding sits at the center of global market plumbing. Many institutions outside the United States borrow, invest, hedge, and fund positions in dollars, even when their home currency is different. Swap markets become one route for transforming one currency exposure into another.

A more expensive route into dollars can point toward stronger dollar demand or tighter dollar funding access. That is why cross-currency basis can belong in a broader funding review. The reading strengthens only when it is confirmed by other evidence, such as funding spreads, credit conditions, dealer balance-sheet pressure, DXY behavior, and broader risk-environment signals.

The main mistake is treating basis as a single crisis gauge. A basis move can reflect dollar pressure, but it can also reflect hedging flows, technical tenor effects, dealer balance-sheet constraints, or pair-specific conventions. Macro interpretation requires confirmation, not just a negative number.

Sign, Pair, Tenor, and Convention Matter

A positive or negative cross-currency basis cannot be interpreted safely without knowing the currency pair, quote convention, tenor, and borrowing or lending direction. The sign tells the reader that pricing is away from a parity reference, but it does not automatically explain who is under pressure or why the pressure exists.

Important limitation: negative basis is often discussed in dollar funding context, but negative does not mean the same thing in every market. The interpretation depends on the pair, the side of the transaction, the maturity, and the convention used to quote the basis.

Practical reading rule: identify the instrument and convention first, then interpret the move inside a broader liquidity framework.

What Cross-Currency Basis Is Not

Cross-currency basis is related to swap markets, but it is not the same thing as a cross-currency swap. A cross-currency swap is an instrument. Cross-currency basis is the pricing spread or adjustment that can appear inside the funding and hedging relationship between currencies.

It is also not a full FX swap pricing tutorial or a basis-curve construction manual. Curve construction can matter for practitioners, but the basic interpretation only needs enough calculation context to show what the basis compares.

| Concept | Main meaning | Boundary |

|---|---|---|

| Cross-currency basis | Pricing deviation from a covered-interest-parity reference | Useful for funding interpretation, not a standalone forecast |

| Cross-currency swap | Instrument used to exchange cash flows across currencies | The instrument can contain basis pricing, but the instrument is broader than the basis itself |

| FX swap pricing | Market pricing for exchanging currencies across spot and forward legs | Pricing mechanics should not replace the macro interpretation boundary |

| Dollar funding liquidity | Access to dollar funding across markets and institutions | Cross-currency basis can inform it, but does not fully define it |

| Eurodollar system | Offshore dollar credit, deposits, and funding relationships | Cross-currency basis is one signal inside a much larger offshore dollar structure |

Illustrative Scenario

Suppose a group of non-dollar institutions needs more dollar funding while natural dollar supply through the swap market is limited. The cost of obtaining dollars through swaps can move away from the covered-interest-parity-implied level. That basis move may suggest tighter dollar funding conditions, but it still needs confirmation from other funding and risk indicators.

If credit spreads are calm, DXY is stable, and other funding measures do not show stress, the basis move may be more technical or pair-specific. If several liquidity measures deteriorate at the same time, the interpretation becomes more macro-relevant.

How Cross-Currency Basis Fits With Related Liquidity Concepts

Cross-currency basis is most useful when it sits inside a broader liquidity map. It can show stress or imbalance in a specific currency funding channel, while other measures help determine whether that pressure is isolated or part of a broader funding environment.

For funding access: connect the basis reading to dollar funding liquidity, where the focus is the ability of institutions to obtain and roll dollar funding.

For offshore dollar structure: connect the signal to the eurodollar system, where offshore dollar credit and funding relationships shape global liquidity transmission.

For broader liquidity context: compare basis conditions with net liquidity, credit conditions, central-bank balance-sheet context, and risk-asset behavior.

Common Misreads

Misread 1: treating cross-currency basis as the same thing as dollar shortage. Basis can reflect dollar funding pressure, but it can also reflect hedging demand, balance-sheet constraints, tenor effects, or convention differences.

Misread 2: assuming a negative basis always has the same meaning. Sign interpretation depends on the pair, quote convention, tenor, and transaction direction.

Misread 3: using basis as a market-timing signal. Cross-currency basis can inform liquidity interpretation, but it does not predict recession timing, equity direction, or trade outcomes by itself.

FAQ

What is cross-currency basis?

Cross-currency basis is the spread or deviation between the market cost of obtaining one currency through swap markets and the cost implied by covered interest parity.

Does negative cross-currency basis always mean dollar shortage?

No. A negative basis can be consistent with stronger dollar funding demand in some contexts, but interpretation depends on the currency pair, tenor, quote convention, transaction direction, and broader liquidity evidence.

How is cross-currency basis related to covered interest parity?

Covered interest parity describes the relationship that should connect spot exchange rates, forward exchange rates, and interest-rate differences. Cross-currency basis appears when real swap-market pricing deviates from that relationship.

Is cross-currency basis a trading signal?

No. Cross-currency basis is a funding and liquidity interpretation input. It can support broader market analysis, but it does not provide buy, sell, entry, exit, recession, or equity-direction signals by itself.