The repo market is the secured short-term funding market where institutions borrow and lend cash against securities collateral through repurchase agreements. It matters because it connects cash demand, collateral availability, short-term financing costs, and funding liquidity across the financial system.

A repo transaction is not a market forecast by itself. Repo conditions can reveal pressure in funding markets, but they need to be read alongside reserves, collateral conditions, policy operations, credit, and broader financial conditions before they become useful for market-structure interpretation.

Key Points

- The repo market is a secured funding market built around repurchase agreements.

- Cash is lent against securities collateral, usually for a short period.

- The repo rate reflects the financing cost of that secured borrowing.

- Repo-market pressure can point to funding-liquidity stress.

- Repo conditions are not standalone buy, sell, or market-direction signals.

What Is the Repo Market?

The repo market is the market for repurchase agreements, often shortened to repos. In a repo, one party receives cash and provides securities as collateral, while agreeing to repurchase those securities later at a slightly higher price. The difference between the sale and repurchase price functions like an interest cost.

For the cash borrower, the repo market is a way to raise short-term funding without selling securities outright. For the cash lender, it is a way to lend against collateral rather than make an unsecured loan. This is why repo sits at the center of money-market plumbing, collateral financing, dealer balance sheets, and short-term liquidity conditions.

The concept is simple, but the interpretation can become misleading if the repo market is treated as only a Federal Reserve operations tool or as a direct market-timing signal. The broader repo market is a funding channel. Its meaning depends on who needs cash, what collateral is available, how much balance-sheet capacity exists, and whether financing costs are rising or falling for structural reasons.

Repo Market Boundary

| Repo market means | It does not mean |

|---|---|

| A secured short-term funding market based on repurchase agreements. | A simple forecast for equities, bonds, the dollar, or crypto. |

| A channel where cash demand and securities collateral meet. | Only a Federal Reserve data page or operations schedule. |

| A market that can reveal funding-liquidity pressure. | A standalone buy or sell signal. |

| A form of market plumbing linked to collateral, reserves, and balance sheets. | The same thing as reverse repo from every participant’s perspective. |

How Repo Transactions Work

A repo transaction begins with a need for cash. An institution that owns securities can use those securities as collateral to borrow cash for a short period. The borrower transfers the securities to the cash lender and agrees to buy them back later.

The repo rate is the financing cost embedded in the transaction. If cash is easy to obtain and collateral is readily accepted, the repo rate may stay close to normal short-term funding levels. If cash becomes scarce, balance-sheet capacity tightens, or certain collateral becomes harder to finance, repo funding costs can rise.

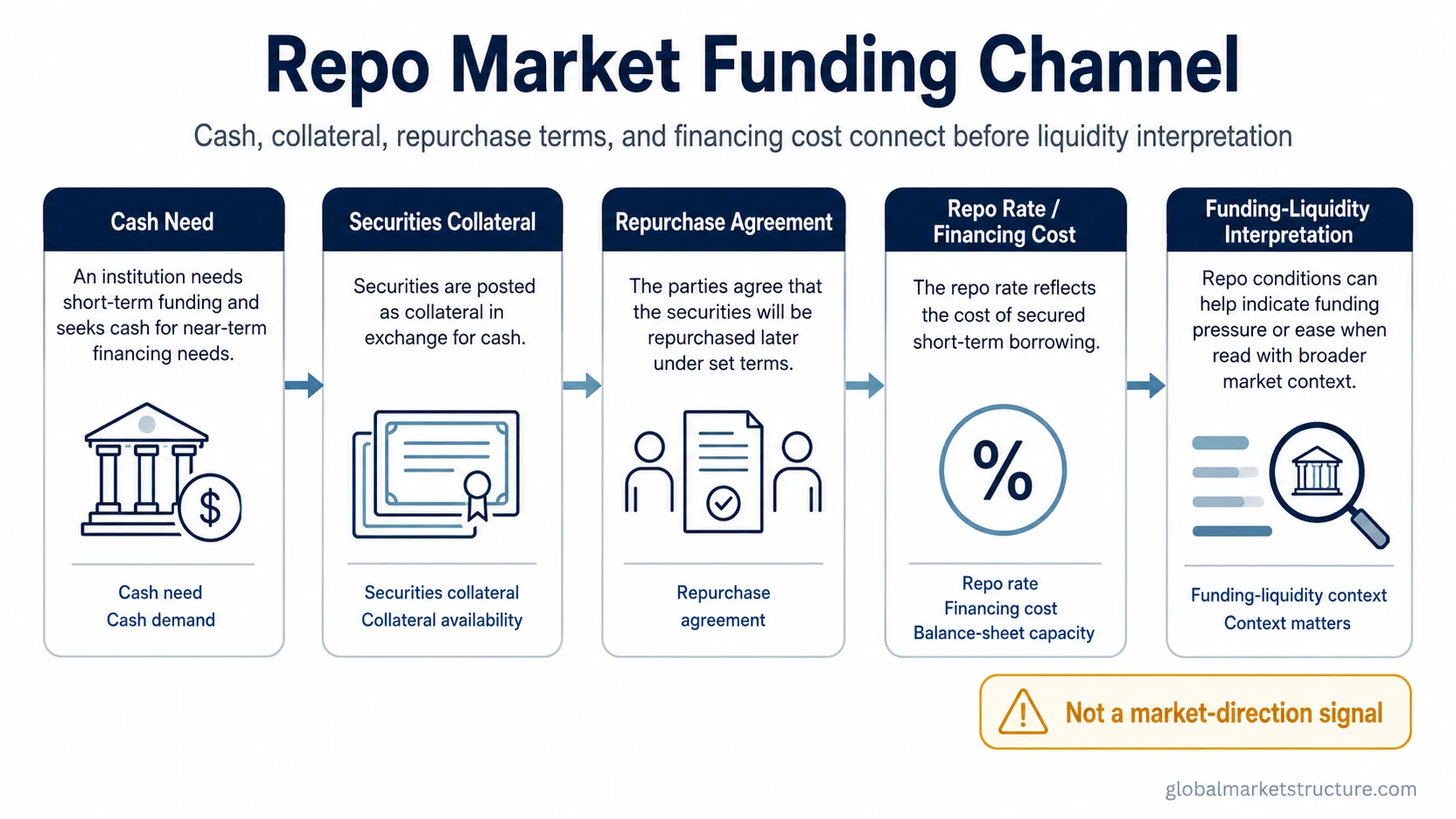

Repo Mechanism Sequence

- Cash is needed: an institution wants short-term funding.

- Collateral is posted: securities are used to secure the cash loan.

- A repurchase agreement is set: the borrower agrees to repurchase the collateral later.

- The repo rate prices the financing: the rate reflects the cost of secured short-term borrowing.

- Liquidity interpretation becomes possible: changes in repo conditions can show pressure in cash demand, collateral financing, or balance-sheet capacity.

Why the Repo Market Matters for Liquidity

The repo market matters because it helps large financial institutions finance securities, manage short-term cash needs, and transform collateral into temporary funding. When repo markets function smoothly, cash and collateral can move through the system with less friction.

That makes repo relevant to funding liquidity. Funding liquidity is about whether participants can obtain financing when they need it. A market can look stable on the surface while financing conditions are becoming less flexible underneath.

Repo conditions can also reflect balance-sheet pressure. Dealers and other intermediaries do not have unlimited capacity to absorb collateral, extend financing, or intermediate cash demand. When balance-sheet capacity is constrained, repo rates can become more sensitive to changes in collateral supply, reserves, quarter-end positioning, or demand for cash.

The important point is interpretation, not prediction. A change in repo conditions can show that money-market plumbing is under pressure, but it does not automatically define the direction of risk assets or the next move in yields.

Repo Market vs Reverse Repo

Repo and reverse repo describe opposite sides of related secured funding transactions. A repo is usually described from the perspective of the party borrowing cash and providing securities as collateral. A reverse repo is described from the perspective of the party lending cash and receiving securities as collateral.

The distinction matters because the same transaction can look different depending on which side is being described. For one party, it is a repo because it raises cash against securities. For the other party, it is a reverse repo because it places cash against securities collateral.

| Term | Common perspective | Basic meaning |

|---|---|---|

| Repo | Cash borrower | Sells securities with an agreement to repurchase them later. |

| Reverse repo | Cash lender | Provides cash and receives securities with an agreement to reverse the transaction later. |

Fed Operations and the Repo Market

Central-bank repo and reverse repo operations are one part of the broader repo-market picture. They can help implement monetary policy, manage short-term interest-rate control, or provide a facility where eligible participants exchange cash and securities under defined terms.

That does not mean the Federal Reserve is the entire repo market. The broader market includes private secured funding transactions among dealers, money-market participants, asset managers, banks, and other institutions. Fed operations are best understood as policy and plumbing context inside a larger secured funding system.

This is why repo-market analysis should avoid two extremes. One extreme treats repo as only a technical central-bank tool. The other treats every repo-rate movement as a direct risk-asset signal. A more useful reading asks what repo conditions say about cash demand, collateral financing, reserves, and the ability of institutions to fund positions.

For broader policy-implementation context, open market operations and the central bank balance sheet explain how central-bank actions interact with short-term funding conditions.

Practical Scenario: Repo Pressure and Funding Liquidity

A common funding scenario begins when several institutions need cash at the same time. They may try to borrow in the repo market by posting securities collateral. If cash lenders become more selective, collateral supply rises, or dealer balance-sheet capacity becomes constrained, repo funding costs can increase.

That increase can suggest tighter funding liquidity. It may show that cash is becoming more valuable, collateral is harder to finance, or intermediaries are less willing to expand balance sheets. The signal becomes more meaningful when it appears alongside other signs of stress, such as tighter reserves, wider credit spreads, weaker market depth, or broader financial-condition pressure.

The scenario still has a boundary. Higher repo rates do not automatically mean that stocks must fall, bonds must rally, or the dollar must move in one direction. Repo pressure is an input into market-structure interpretation, not a complete market-regime reading by itself.

Common Misreadings

- Repo market pressure is not a standalone crash signal. It can indicate funding stress, but broader confirmation is needed.

- Repo is not identical to reverse repo. They are related perspectives, not interchangeable labels in every context.

- Fed operations are not the whole market. Policy facilities sit inside a broader secured funding system.

- Repo data is not a complete liquidity dashboard. Reserves, collateral conditions, credit spreads, funding markets, and broader financial conditions also matter.

- A repo-rate move is not trading advice. It should not be treated as a buy, sell, or allocation instruction.

Related Concepts

The repo market connects most directly to reverse repo, because the two terms describe opposite sides of related secured funding transactions. It also connects to funding liquidity, because repo conditions can show whether market participants can finance positions efficiently.

For central-bank context, open market operations and the central bank balance sheet explain the policy side of short-term funding conditions. For broader interpretation, repo conditions can also be read alongside financial conditions.

FAQ

What is the repo market in simple terms?

The repo market is a secured short-term funding market where institutions borrow and lend cash against securities collateral through repurchase agreements.

How does a repo transaction work?

One party receives cash and provides securities as collateral, while agreeing to repurchase those securities later. The repo rate reflects the financing cost of that transaction.

Why does the repo market matter?

It matters because it helps show funding-liquidity conditions, cash demand, collateral financing pressure, and balance-sheet capacity in short-term funding markets.

Is repo the same as reverse repo?

No. Repo and reverse repo describe opposite sides of related secured funding transactions. The repo side usually refers to borrowing cash against securities, while the reverse repo side refers to lending cash against securities collateral.

Does repo-market stress predict market direction?

No. Repo-market stress can indicate funding pressure, but it does not automatically predict the direction of equities, bonds, currencies, or crypto. It should be read with broader liquidity and financial-condition evidence.

Are Federal Reserve repo operations the whole repo market?

No. Federal Reserve operations are one policy-implementation context inside a broader secured funding market that also includes private institutional repo transactions.