Open market operations are central-bank transactions used to implement monetary policy by influencing reserves, liquidity conditions, and short-term interest-rate pressure. They matter for market structure because they can affect funding pressure and the broader policy transmission environment, but the operation alone does not forecast market direction.

- They work through reserves, settlement liquidity, or similar operating-framework channels.

- They help central banks influence short-term rate conditions.

- They can affect funding pressure and broader financial conditions when the liquidity effect is large enough to matter.

The useful boundary is simple: an open market operation is a policy-implementation action, not a standalone market forecast.

Key Points

- Open market operations are one of the main ways central banks implement monetary policy in financial markets.

- Liquidity-providing operations can add reserves or ease short-term funding pressure under the relevant operating framework.

- Liquidity-draining operations, sales, reverse operations, or similar tools can absorb reserves or reduce excess liquidity pressure.

- The effect changes with the central bank’s framework, the instrument used, the policy stance, and the surrounding market environment.

- An open market operation is not automatically quantitative easing, quantitative tightening, or a direct risk-asset signal.

What Open Market Operations Mean

An open market operation is a central-bank action carried out in financial markets to influence the conditions under which money, reserves, or short-term funding are supplied. In many frameworks, the operation involves buying securities, selling securities, lending against collateral, absorbing liquidity, or using related instruments to keep short-term rates aligned with policy objectives.

The concept is operational rather than predictive. It describes how a central bank transmits policy into money-market conditions. Market participants may care because these operations can affect liquidity, funding pressure, and rate expectations, but they still need to interpret the operation alongside policy stance, yields, credit conditions, the dollar, inflation, growth, and risk appetite.

Simple Definition

Open market operations are central-bank market operations used to implement monetary policy by affecting reserves, liquidity conditions, and short-term interest-rate pressure.

They are best understood as a transmission mechanism. The operation changes a funding or reserve condition first. Broader market interpretation comes later and remains conditional.

How Open Market Operations Work

The basic mechanism starts with a central bank conducting a market operation with eligible counterparties. Across different operating frameworks, the operation may involve securities purchases, securities sales, repurchase agreements, reverse repurchase agreements, refinancing operations, or another official-market tool.

When the operation provides liquidity, counterparties receive cash or reserves against securities or through another eligible structure. That can ease reserve scarcity, reduce short-term funding pressure, or help keep market rates near the desired policy setting. When the operation drains liquidity, cash can move back toward the central bank or reserves can be absorbed, which can reduce excess liquidity pressure.

The market-structure impact is indirect. The central bank operation may influence short-term rates and funding conditions, which may then affect broader financial conditions. Asset prices can respond to that environment, but the response depends on expectations, risk appetite, credit, yields, currency conditions, and whether the operation is temporary or persistent.

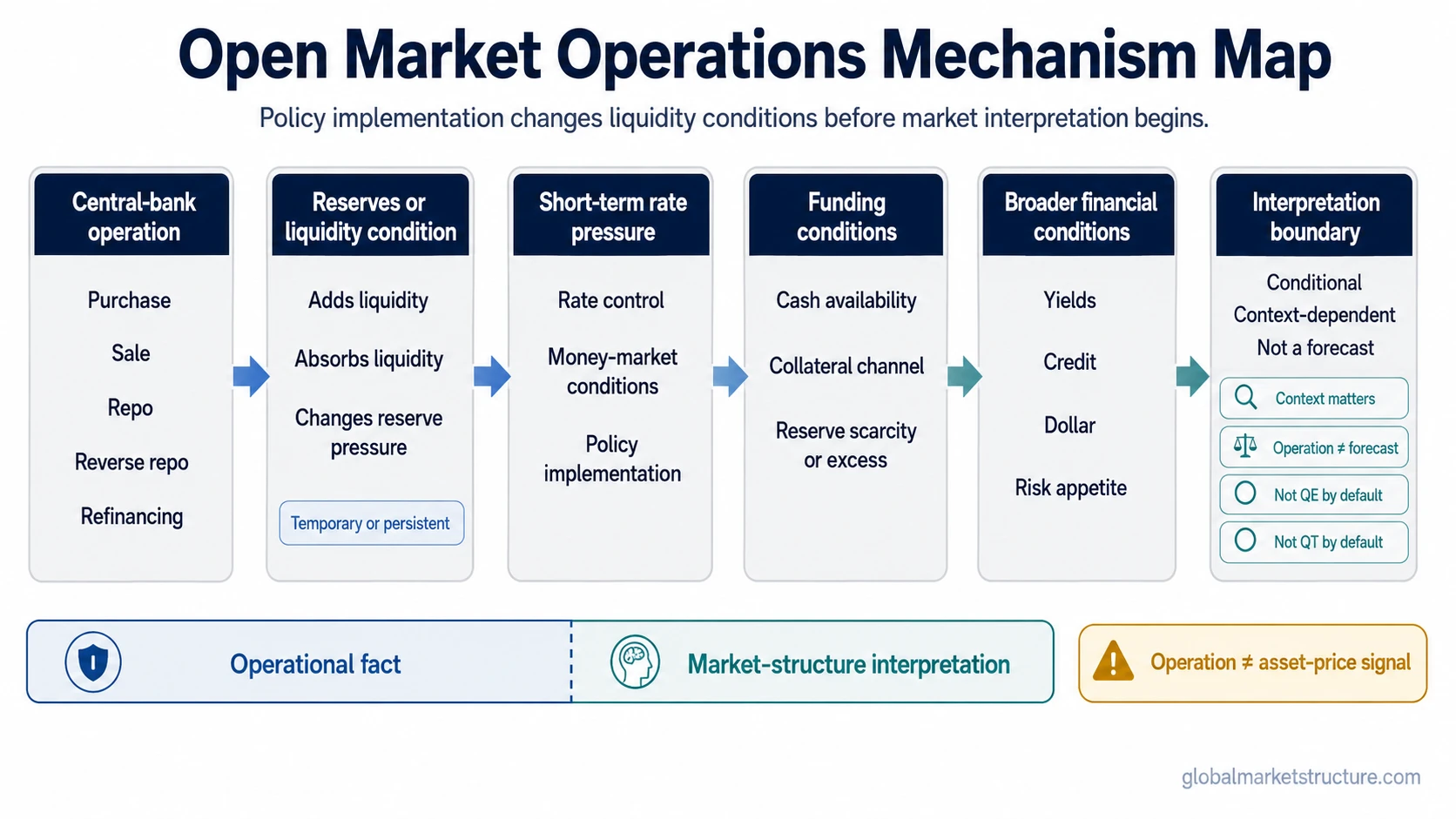

Open Market Operations Mechanism Map

Central-bank operation → reserves or liquidity condition → short-term rate pressure → funding conditions → broader financial conditions → market-structure interpretation boundary

Interpretation is conditional. The operation does not automatically forecast asset prices.

Temporary vs Permanent Open Market Operations

Open market operations can be temporary or permanent. The distinction matters because a short-term liquidity adjustment does not carry the same market-structure meaning as a persistent balance-sheet action.

Temporary operations are designed to add or absorb liquidity for a limited period. Across central-bank operating frameworks, these can include repos, reverse repos, refinancing operations, or other short-term instruments. Their purpose is often to manage short-term rate control, money-market conditions, or temporary reserve needs.

Permanent operations involve outright purchases or sales that can change the central bank’s asset holdings more durably. These operations are closer to the stock of the central bank balance sheet because they can affect the size or composition of assets and liabilities over time.

The same label can behave differently across central banks. A Federal Reserve operation, an ECB operation, and another central bank’s liquidity facility may share a policy-implementation purpose while using different instruments, counterparties, and reserve frameworks.

Open Market Operations vs Related Concepts

Open market operations are often confused with nearby liquidity concepts. The cleanest way to avoid that mistake is to separate the action from the instrument, the balance-sheet stock, and the broader liquidity regime.

| Concept | What it means | Relationship to open market operations | Boundary |

|---|---|---|---|

| Open market operation | Central-bank market transaction used for policy implementation. | Core subject. | Operational mechanism, not the whole liquidity regime. |

| Repo | A secured transaction involving securities and cash, often structured with a later repurchase. | Can be used in temporary open market operations. | Not all open market operations are repos. |

| Reverse repo | A transaction that can absorb cash or reserves from the system under some frameworks. | Can be used as a liquidity-draining operation. | Instrument, not the full policy category. |

| Quantitative easing | A large-scale asset-purchase policy normally associated with balance-sheet expansion. | May use open-market purchases. | Not every open-market purchase is QE. |

| Quantitative tightening | A balance-sheet reduction or liquidity-withdrawal process. | Can overlap with liquidity-draining operations. | Not every draining operation is QT. |

| Central bank liquidity | The broader set of official liquidity channels, facilities, reserves, and balance-sheet effects. | Open market operations are one part of the broader channel. | Broader category than any single operation. |

How Open Market Operations Affect Liquidity

Liquidity effects depend on whether the operation supplies funds, absorbs funds, changes reserves, changes collateral availability, or supports short-term rate control. A liquidity-providing operation can ease money-market pressure if reserves or cash become more available. A liquidity-draining operation can reduce excess liquidity or raise the opportunity cost of holding cash outside the central bank.

The balance-sheet effect also matters. A temporary repo-style operation may reverse after a short period, while an outright purchase or sale can alter the central bank’s asset holdings more persistently. That is why open market operations should be interpreted through operation type, maturity, scale, persistence, and the central bank’s operating framework.

Why Open Market Operations Matter for Market Structure

Open market operations matter because funding markets sit close to the center of the financial system. When short-term funding pressure changes, the effect can pass into money markets, bank reserves, collateral conditions, credit availability, and the discount-rate environment. Those channels can influence the broader risk environment even when the central bank is not directly targeting asset prices.

The market-structure question is not whether an operation is automatically bullish or bearish. The better question is whether the operation changes the liquidity environment, whether that change is temporary or persistent, and whether other markets confirm the same pressure through yields, credit spreads, the dollar, volatility, and risk appetite.

Common Misreads

- Treating every purchase as QE: A purchase can be an implementation operation without being a full quantitative easing program.

- Treating every drain as QT: A liquidity-draining operation is not automatically a broad quantitative tightening regime.

- Reading the operation as a market signal: Open market operations can affect conditions, but they do not provide direct buy or sell instructions.

- Ignoring the operating framework: The same action can have a different meaning under reserve-scarce, reserve-abundant, corridor, floor, or other policy frameworks.

- Ignoring persistence: A one-day liquidity operation does not carry the same market-structure weight as a persistent balance-sheet program.

Practical Scenario

A central bank may conduct a temporary liquidity-providing operation when short-term funding pressure rises. The immediate effect is not a guaranteed asset-price move. The first question is whether the operation eases the funding stress it was designed to address.

If the operation is small, short-lived, and isolated, broader markets may treat it as routine policy implementation. If similar operations become persistent, funding pressure remains elevated, and credit or currency markets confirm stress, the same category of operation can become more important for market-structure interpretation.

How to Interpret Open Market Operations

A useful interpretation process separates operational facts from market conclusions. The operational fact is the instrument, direction, size, maturity, and counterparty structure of the central-bank action. The market conclusion requires additional evidence from funding markets, policy expectations, credit, yields, the dollar, volatility, and asset-market breadth.

Open market operations are strongest as a liquidity and policy-transmission input. They become weaker when treated as standalone market timing tools. The operation can change the environment, but the market’s response still depends on the surrounding regime.

Related Liquidity Concepts

- Central bank liquidity covers the broader official liquidity channel.

- Quantitative easing explains persistent asset purchases and balance-sheet expansion.

- Quantitative tightening explains balance-sheet reduction and liquidity withdrawal.

- Central bank balance sheet separates the stock of assets and liabilities from individual operations.

- Repo market explains the secured funding market often connected to temporary operations.

- Reverse repo explains the reverse structure used in some liquidity-absorbing operations.

Interpretation Boundary

Open market operations should not be read as market forecasts by themselves. They identify a central-bank implementation channel. Market interpretation still requires policy context, liquidity persistence, credit conditions, yields, the dollar, market breadth, and risk appetite.

The operation is the starting point, not the conclusion. Open market operations affect the operating layer first. Broader risk interpretation depends on whether the liquidity effect persists and whether other macro and cross-asset signals confirm the change.

Open Market Operations FAQ

What are open market operations in simple terms?

Open market operations are central-bank market transactions used to influence reserves, liquidity conditions, and short-term interest-rate pressure. They are a way to implement monetary policy through financial markets.

Are open market operations the same as quantitative easing?

No. Quantitative easing can use open-market purchases, but not every open market operation is QE. QE is usually a larger and more persistent asset-purchase program linked to balance-sheet expansion.

How do open market operations affect liquidity?

They can add liquidity when the central bank provides cash or reserves, and they can absorb liquidity when the operation drains cash or reserves. The exact effect depends on the instrument and operating framework.

Are repos and reverse repos open market operations?

Repos and reverse repos can be used as temporary open market operations in some central-bank frameworks. They are instruments that can provide or absorb liquidity, but they do not represent every type of open market operation.

Do open market operations predict market direction?

No. They can influence funding conditions and financial conditions, but they do not by themselves predict asset prices. Market interpretation depends on policy stance, liquidity persistence, credit, yields, currency conditions, and broader risk appetite.