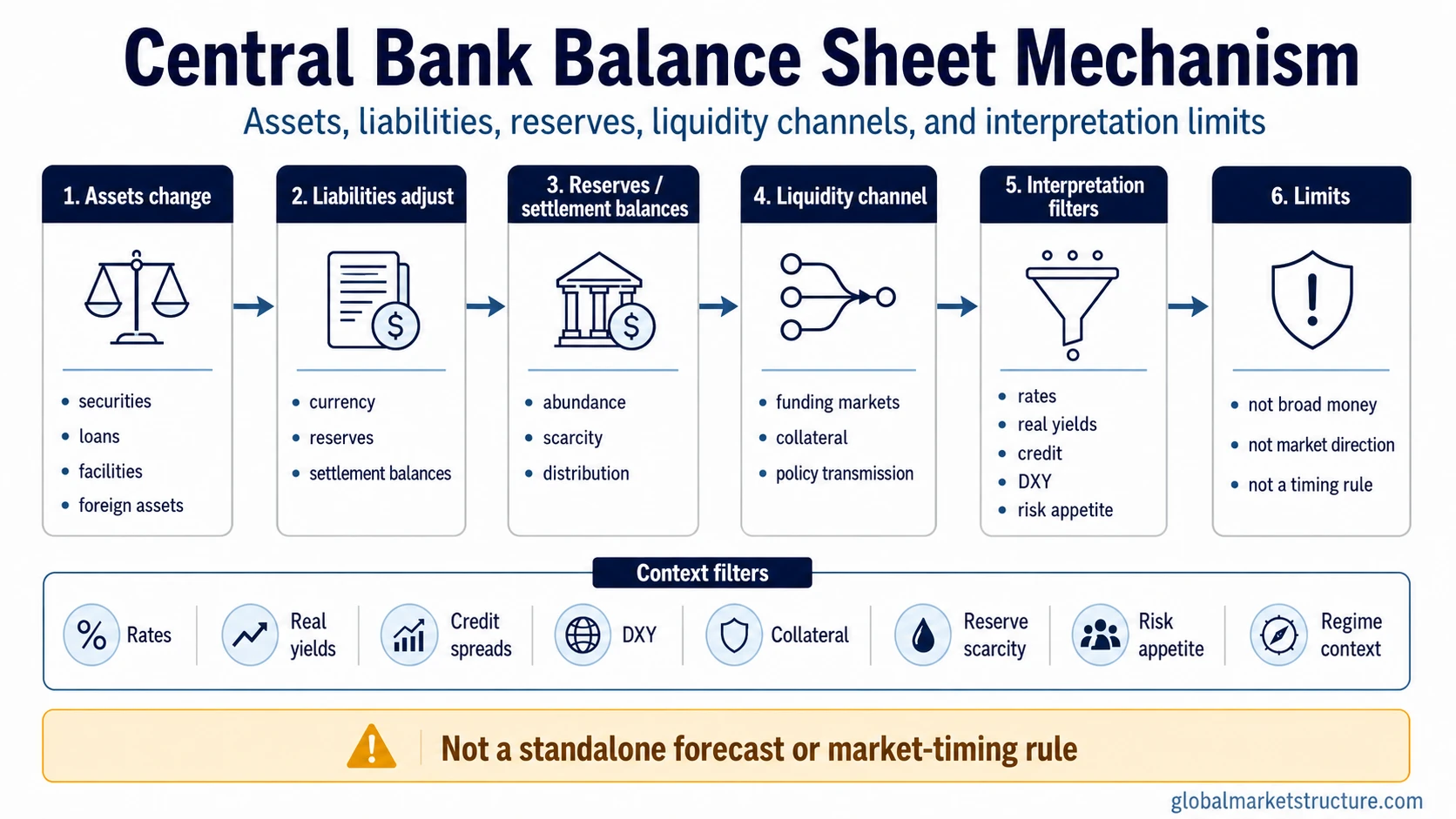

A central bank balance sheet records the assets and liabilities of a central bank. For market interpretation, it matters because changes in the balance sheet can affect reserves, settlement balances, liquidity plumbing, and policy transmission, but it does not create a standalone market forecast or trading signal.

The balance sheet connects accounting to monetary conditions. Assets show what the central bank holds, buys, lends against, or receives as collateral. Liabilities show the claims issued by the central bank, including currency in circulation and reserve or settlement balances used inside the financial system.

Definition: A central bank balance sheet is the statement of a central bank’s assets and liabilities. Its market relevance comes from the channels that connect those items to reserves, settlement money, funding conditions, policy implementation, and expectations.

Key Points

- A central bank balance sheet shows what the central bank owns or lends against and what it owes.

- Assets can include securities, loans, foreign assets, or policy-related holdings, depending on the central bank.

- Liabilities commonly include currency and reserve or settlement balances held by banks.

- Balance-sheet expansion or contraction can change liquidity plumbing, but it does not automatically predict market direction.

- The interpretation depends on rates, real yields, credit conditions, DXY, collateral, reserve scarcity, risk appetite, and regime context.

What a Central Bank Balance Sheet Shows

The asset side shows the instruments and claims held by the central bank. These may include government securities, loans to banks, foreign reserves, repo-related assets, or other holdings created by policy operations. The exact mix depends on the institution, legal framework, and policy tools in use.

The liability side shows claims on the central bank. Currency in circulation is one liability. Bank reserves or settlement balances are another important liability because they are used by banks to settle payments, meet regulatory needs, and interact with the central bank’s operating framework.

The accounting statement becomes market-relevant only when asset and liability changes affect the financial system’s operating conditions. A larger asset total may matter differently depending on which assets were purchased, which liabilities expanded, where reserves sit, and whether the banking system is reserve-abundant or reserve-constrained.

Assets, Liabilities, and Reserves

Assets and liabilities should not be compressed into one liquidity label. A central bank can expand assets while the practical market effect depends on how reserves, settlement balances, collateral, and private credit conditions respond.

| Balance-sheet item | What changes | Liquidity channel | What it can suggest | What it cannot prove |

|---|---|---|---|---|

| Securities holdings | The central bank buys, sells, or allows securities to mature. | Purchases can add reserve balances; runoff or sales can reduce them. | Policy implementation may be adding or removing balance-sheet support. | It cannot prove that risk assets will rise or fall. |

| Loans and liquidity facilities | The central bank lends against eligible collateral or receives repayment. | Temporary lending can ease funding pressure in specific parts of the system. | Stress or precautionary liquidity demand may be present. | It cannot prove that the broader market regime has changed. |

| Foreign assets or swap-related claims | Cross-border liquidity tools or foreign-reserve positions change. | Foreign-currency funding conditions may be affected. | Global dollar or reserve-currency pressure may deserve attention. | It cannot prove a durable currency trend by itself. |

| Currency in circulation | Physical currency demand changes. | Currency demand can affect reserve balances when cash moves out of the banking system. | Payment preferences or cash demand may be shifting. | It cannot be treated as the same thing as broad money or credit creation. |

| Bank reserves or settlement balances | Banks hold more or fewer balances at the central bank. | Reserve abundance or scarcity can affect funding markets and policy transmission. | Liquidity plumbing may be easier or tighter for the banking system. | It cannot prove that private credit, market liquidity, or risk appetite is strong. |

How Balance-Sheet Changes Affect Liquidity

Balance-sheet expansion often begins with an asset-side action. A central bank may buy securities, lend to banks, or use another facility that increases assets. The liability side usually adjusts as reserves, settlement balances, or other central-bank claims increase.

The operational path matters. Securities purchases and sales usually belong to the same policy-operation family as open market operations. Those operations can change reserves, but the market interpretation still depends on the broader policy setting and financial conditions.

Quantitative easing is one way a balance sheet can expand when the central bank purchases assets at scale. Quantitative tightening is one way a balance sheet can shrink when securities mature, run off, or are sold. The balance sheet is broader than either tool because it includes the full asset and liability structure, not only QE or QT programs.

Liquidity channel: The useful reading is not only whether the balance sheet is larger or smaller. The stronger question is which liability changed, whether reserves became more abundant or scarcer, and whether funding markets, credit spreads, collateral conditions, and risk appetite confirm the same message.

Balance-Sheet Policy, Expectations, and Forward Guidance

Balance-sheet policy changes the accounting and liquidity plumbing of the central bank. Policy communication changes expectations about future rates, asset purchases, runoff pace, and the reaction function. The two can interact, but they are not the same mechanism.

A central bank can communicate future policy intentions before the balance sheet changes materially. That communication channel is closer to forward guidance, where market expectations adjust through stated policy path, reaction function, or conditional guidance.

The distinction matters because markets may react to expected balance-sheet policy before the accounting statement changes. A balance-sheet release shows what has happened to the statement. Communication can move expectations about what may happen next. Neither channel removes the need to compare rates, real yields, credit conditions, DXY, and risk appetite.

What the Balance Sheet Can and Cannot Tell You

A central bank balance sheet can show whether a policy authority is adding assets, allowing assets to run off, increasing lending, shrinking facilities, or changing the liability mix. It can also show whether reserves or settlement balances are rising or falling.

Interpretation limit: Balance-sheet size alone is not a complete liquidity reading. It does not automatically show broad money growth, private credit creation, risk appetite, market depth, asset-price direction, or recession risk. The same balance-sheet change can carry a different market meaning when policy rates, real yields, credit spreads, DXY, collateral conditions, and reserve scarcity are different.

A larger balance sheet can still sit alongside tight financial conditions when policy rates are high, credit spreads are widening, collateral is scarce, or risk appetite is deteriorating. Balance-sheet reduction is also not automatically disruptive if reserves remain abundant and private funding conditions stay stable.

Central Bank Balance Sheet Example in Context

A central bank buys securities from the market. Its assets rise because it now holds more securities. The liability side also changes because the banking system receives additional reserve or settlement balances.

The first-order liquidity reading is that reserves have increased. The market-structure reading is still conditional. If policy rates remain restrictive, credit spreads widen, DXY strengthens, and risk appetite weakens, the balance-sheet expansion may not translate into broad risk-on conditions. If reserves were scarce and funding markets were under pressure, the same expansion may ease a specific plumbing problem without becoming a full market forecast.

The useful diagnostic sequence is accounting change first, liquidity channel second, market interpretation third, and limitation last.

Common Misreadings

The central-bank balance sheet is often misread when the accounting number is treated as a complete macro signal. The balance sheet can be an important input, but it is not the whole financial-conditions map.

- Balance sheet equals liquidity: liquidity depends on reserves, funding markets, collateral, credit, and market depth, not only total assets.

- Reserves equal broad money: reserve balances are central-bank liabilities used inside the banking system, while broad money and credit depend on private-sector behavior as well.

- QE equals risk-on: asset purchases can ease some conditions, but valuation, real yields, credit, and risk appetite still matter.

- QT equals crisis: runoff can drain reserves, but stress depends on reserve scarcity, funding conditions, policy stance, and market structure.

- Fed data equals the whole concept: Fed balance-sheet data is important, but other central banks can have different asset mixes, liabilities, mandates, and operating frameworks.

Related Concepts

The balance sheet connects most directly to securities purchases, securities sales, maturities, reserve management, and policy communication. Operating actions change the statement itself, while communication changes expectations about future policy paths.

QE, QT, QE vs QT, central bank liquidity, and central-bank liquidity swaps are adjacent concepts, but each one explains a different policy tool, liquidity channel, or facility structure.

FAQ

What is a central bank balance sheet?

A central bank balance sheet is the statement of a central bank’s assets and liabilities. It shows what the central bank holds, lends against, or receives, and what claims exist against it, including currency and reserve or settlement balances.

Does a larger central bank balance sheet mean more liquidity?

Not always. A larger balance sheet can add reserves or settlement balances, but liquidity conditions also depend on policy rates, credit spreads, collateral, funding markets, reserve scarcity, DXY, and risk appetite.

How do QE and QT affect a central bank balance sheet?

QE can expand the balance sheet when a central bank purchases assets and creates reserve or settlement balances. QT can reduce the balance sheet when assets mature, run off, or are sold, depending on the policy design.

Can the central bank balance sheet predict markets?

No. Balance-sheet changes can influence liquidity plumbing and policy transmission, but they do not predict market direction by themselves. Market interpretation still depends on rates, real yields, credit, DXY, positioning, and regime context.