Forward guidance is central-bank communication about the likely future path of monetary policy. Its main market channel is expectations: guidance can influence how investors price future rates, yield curves, funding costs, and financial conditions before a policy rate or balance sheet actually changes. The concept belongs to policy communication and expectations, not direct liquidity provision.

Key Points

- Forward guidance communicates how a central bank expects policy to evolve.

- The main transmission channel is expectations, not direct money creation.

- Markets may reprice short-rate paths, yield curves, funding conditions, credit risk, and broader financial conditions.

- Forward guidance differs from balance-sheet tools such as quantitative easing and quantitative tightening.

- Its effect depends on credibility, economic data, inflation conditions, and whether markets believe the guidance can be maintained.

What Forward Guidance Means

Forward guidance is a monetary-policy communication tool. A central bank uses speeches, statements, projections, press conferences, or policy minutes to shape expectations about future interest rates, asset purchases, reinvestment policy, or the conditions that could change the policy path.

The guidance can be explicit, such as a stated condition for keeping rates low, or more qualitative, such as language that signals patience, caution, restrictiveness, or future easing risk. The purpose is not only to describe current policy. It also influences how markets price the future path of policy.

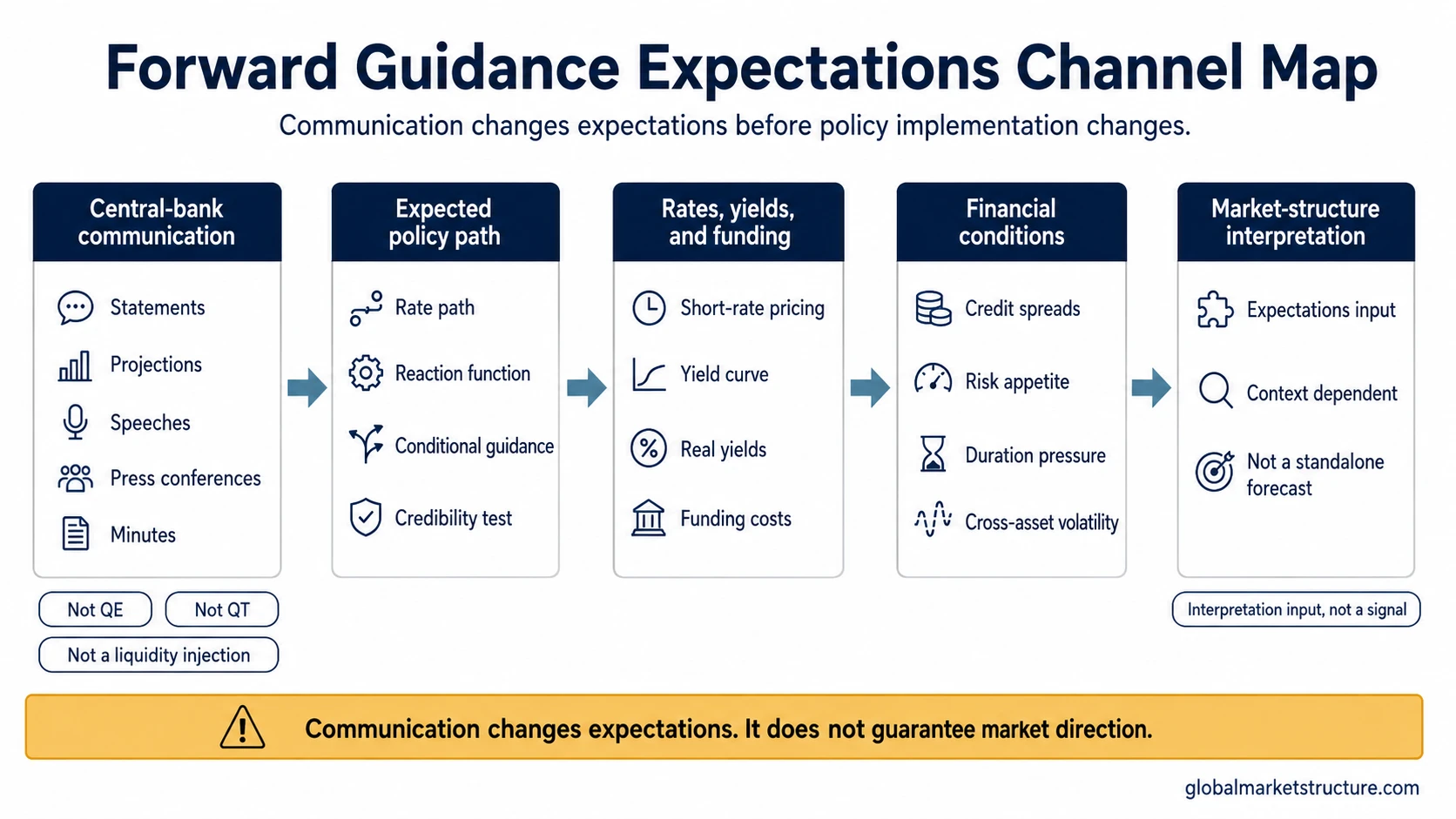

How the Expectations Channel Works

The forward-guidance channel begins with communication and moves through expectations before it reaches markets. A central bank does not need to change its policy rate on the same day for guidance to matter. If the communication changes the expected policy path, markets may adjust before the actual decision arrives.

| Step | What changes | Market-structure relevance |

|---|---|---|

| Central-bank communication | Policy statement, projection, speech, minutes, or press conference language changes expectations. | Markets interpret whether the central bank sounds more restrictive, patient, flexible, or concerned. |

| Expected policy path | Investors adjust expectations for future rates, balance-sheet policy, or reaction function. | Short-rate pricing and policy-path assumptions may move before a formal decision. |

| Rates, yields, and funding | Yields, term structure, real-rate assumptions, and funding costs can reprice. | The shift can tighten or loosen perceived financial conditions. |

| Credit and risk appetite | Credit spreads, duration-sensitive assets, and risk appetite may respond to the new policy path. | The reaction helps show whether markets see the guidance as supportive, restrictive, or uncertain. |

| Interpretation boundary | Market behavior reflects expectations, credibility, and positioning, not guaranteed outcomes. | Forward guidance is an interpretation input, not a trading signal or forecast. |

Forward Guidance Versus QE, QT, and Balance-Sheet Policy

The most important boundary is that forward guidance is communication. It can influence expectations about future liquidity conditions, but it is not the same thing as changing the size or composition of the central bank balance sheet.

| Concept | What it is | Main channel | What it is not |

|---|---|---|---|

| Forward guidance | Communication about the likely or conditional future policy path. | Expectations, rate-path pricing, credibility, and financial conditions. | Not a direct liquidity injection or a guaranteed policy promise. |

| Quantitative easing | Central-bank asset purchases that expand or alter the balance sheet. | Balance-sheet expansion, portfolio effects, term-premium pressure, and liquidity conditions. | Not just communication about future policy. |

| Quantitative tightening | Balance-sheet reduction or runoff after an expansion phase. | Reserve dynamics, liquidity withdrawal, and balance-sheet contraction. | Not a verbal signal by itself. |

| Central bank balance sheet | The stock of central-bank assets and liabilities. | Reserves, settlement balances, asset holdings, and liabilities. | Not the same as guidance about the future policy path. |

| Open-market operations | Operational purchases or sales used to implement policy and manage money-market conditions. | Policy implementation and short-term market operations. | Not a broad communication framework by itself. |

Markets may react to guidance even when no reserves have been added and no assets have been purchased. In that case, the first effect is a repricing of expectations, not a completed change in liquidity supply.

Why Credibility and Conditionality Matter

Forward guidance is conditional, not automatic. Central banks usually guide markets through a reaction function: if inflation, employment, growth, financial stability, or credit conditions evolve in a certain way, policy may follow a certain path. If the data changes, the guidance can change too.

Forward guidance is not a binding promise. The market reaction depends on whether investors believe the central bank can and will follow the communicated path. Credibility is stronger when the message is consistent with the economic outlook and the central bank’s mandate. Credibility weakens when guidance conflicts with inflation pressure, financial stress, or incoming data.

An expectations gap can open when markets price one policy path while the central bank is trying to communicate another. That gap can create volatility around speeches, inflation reports, labor-market data, and policy meetings because each new input may confirm or challenge the expected path.

What Markets May Watch After Guidance Changes

Forward guidance is most useful for market-structure interpretation when it is compared with the reaction across rates, credit, funding, and risk assets. A single headline is rarely enough. The surrounding market response shows whether the guidance is being treated as credible, restrictive, supportive, or uncertain.

| Market area | What may reprice | Interpretation boundary |

|---|---|---|

| Short-rate expectations | Expected cuts, hikes, pauses, or policy duration. | Shows whether markets accept the communicated path or price a different one. |

| Yield curve | Front-end yields, long-end yields, curve slope, and term-premium assumptions. | Different parts of the curve can respond to policy path, growth risk, inflation risk, or credibility risk. |

| Real yields | Inflation-adjusted discount-rate pressure. | Useful when guidance changes expected policy restrictiveness relative to inflation expectations. |

| Credit conditions | Credit spreads, issuance conditions, and risk compensation. | Helps show whether guidance is easing or tightening perceived financing pressure. |

| Funding and liquidity context | Money-market stress, funding spreads, reserve sensitivity, and broader central bank liquidity conditions. | Prevents confusing expectation-driven repricing with actual liquidity provision. |

| Risk appetite | Equities, credit beta, duration assets, commodities, and cross-asset volatility. | Risk response can change if markets doubt the guidance or see it as data-dependent. |

The safer interpretation is conditional: guidance may affect market pricing when it changes the expected policy path, but the final market response depends on data, credibility, positioning, and the broader financial-conditions backdrop.

Common Mistakes When Reading Forward Guidance

Mistake 1: treating guidance as a liquidity injection. Guidance can change expectations about future policy, but it does not itself add reserves or expand the balance sheet.

Mistake 2: treating guidance as a guaranteed forecast. Central banks can change guidance when inflation, growth, employment, credit, or financial stability conditions change.

Mistake 3: treating guidance as a binding promise. Forward guidance can describe a likely or conditional policy path, but incoming data and financial conditions can still change that path.

Mistake 4: reading one asset reaction in isolation. A risk-asset rally, yield drop, or dollar move may reflect several forces at once. The interpretation is stronger when rate expectations, curve behavior, credit, funding, and risk appetite point in a coherent direction.

How Expectations Can Reprice Markets

Imagine a central bank says policy may stay restrictive for longer unless inflation slows more clearly. Even before the next policy meeting, front-end yields may rise, real-yield pressure may increase, credit spreads may stop tightening, and risk appetite may weaken. The guidance did not directly remove liquidity. It changed the expected policy path, and markets adjusted the cost of money around that expectation.

The same words can produce a different reaction if investors already expected a restrictive stance, if inflation data begins to soften, or if funding stress forces markets to price future easing. Forward guidance works through expectations, and expectations are always filtered through context.

How Forward Guidance Fits Into Market Structure

Forward guidance belongs inside the central-bank-liquidity framework because it helps shape expectations around future policy conditions. It sits between communication and implementation: it can prepare markets for a path, but it is not the same as executing that path.

For market interpretation, the useful question is not whether the guidance is “bullish” or “bearish” by itself. The useful question is whether the communication changes the expected path of money, rates, funding, and financial conditions, and whether cross-asset behavior confirms that repricing.

FAQ

What is forward guidance in central banking?

Forward guidance is central-bank communication about the likely or conditional future path of monetary policy. It helps shape expectations for rates, liquidity conditions, and financial conditions before policy changes actually occur.

How does forward guidance affect markets?

Forward guidance can affect markets by changing expectations for future policy. Those expectations can influence short-rate pricing, yield curves, funding costs, credit conditions, and broader risk appetite.

Is forward guidance the same as quantitative easing?

No. Forward guidance is communication. Quantitative easing involves asset purchases that expand or alter the central bank balance sheet. Guidance may influence expectations about QE, but it is not QE itself.

Can forward guidance fail?

Yes. Forward guidance can fail or weaken if markets doubt the central bank’s credibility, if economic data changes, or if the guidance conflicts with inflation, growth, or financial-stability conditions.

Related Concepts

Forward guidance is clearer when communication, balance-sheet policy, and implementation tools are separated. Quantitative easing and quantitative tightening affect the balance sheet directly. Central bank balance sheet analysis explains the stock of assets and liabilities. Open-market operations explain implementation mechanics. Forward guidance sits before those actions by shaping expectations about the policy path.