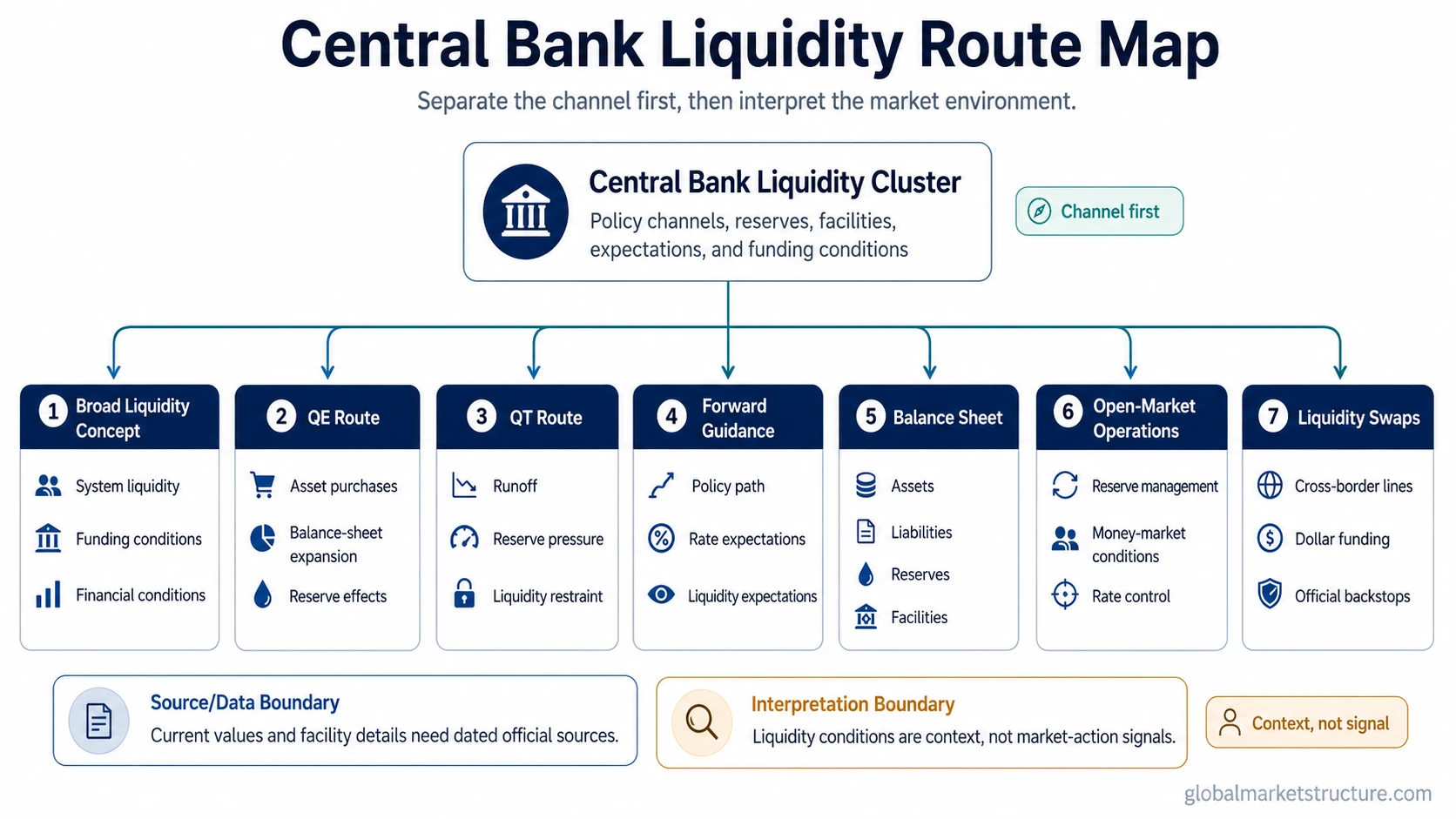

Central bank liquidity describes the channels central banks use to add, drain, backstop, signal, or route liquidity through balance sheets, policy operations, guidance, and liquidity facilities.

The main distinction is channel selection. A broad liquidity question belongs with the central-bank-liquidity concept, while asset-purchase expansion, balance-sheet reduction, policy communication, operational implementation, reserve mechanics, and cross-border liquidity facilities each need a narrower path.

Definition: Central bank liquidity is a cluster of policy and balance-sheet channels that can affect funding conditions, reserves, market functioning, expectations, and broad financial conditions. It is not one single tool, one chart, or one mechanical market signal.

Key Points

- Central bank liquidity includes QE, QT, balance-sheet mechanics, policy operations, forward guidance, and liquidity facilities.

- Each channel answers a different market-structure question, so the first step is separating the mechanism before interpreting conditions.

- Current facility details, operation schedules, and data values require dated primary-source checks.

- Liquidity interpretation and market action are separate questions. A liquidity condition is not a mechanical market-action signal or an asset-price guarantee.

Choose the Liquidity Channel

Central-bank liquidity questions become clearer when the question is matched to the right channel. A chart question, a QE question, a swap-line question, and a balance-sheet question may all belong to the same liquidity cluster, but they do not ask for the same explanation.

| Reader question | Liquidity channel | Best next concept | What it answers |

|---|---|---|---|

| What does central bank liquidity mean at the broad level? | Cluster definition and market-structure context | central bank liquidity | How the broad liquidity concept connects policy channels, funding conditions, reserves, and financial conditions. |

| How does asset-purchase expansion add liquidity? | Balance-sheet expansion | quantitative easing | How central-bank asset purchases can expand the balance sheet and affect reserves, yields, and financial conditions. |

| How does balance-sheet reduction drain or restrain liquidity? | Balance-sheet runoff or reduction | quantitative tightening | How runoff or asset reduction can change reserve conditions, duration supply, and liquidity expectations. |

| How do policy statements shape liquidity expectations? | Communication and expected policy path | forward guidance | How policy communication affects expected rates, expected liquidity, and the market’s view of future policy settings. |

| What does the central-bank balance sheet show? | Assets, liabilities, reserves, and balance-sheet composition | central bank balance sheet | How asset holdings, liabilities, reserves, and facilities appear in the accounting structure. |

| How are day-to-day policy operations implemented? | Market operations and liquidity implementation | open-market operations | How central banks use operations to manage reserves, short-term rates, and money-market conditions. |

| How does liquidity move through central-bank swap or liquidity lines? | Cross-border funding backstops | central bank liquidity swaps | How central banks can provide foreign-currency or dollar liquidity through official arrangements. |

Central Bank Liquidity Routes

Each liquidity route keeps a different question separate. That separation reduces the risk of treating one policy tool, one facility, or one data series as the whole liquidity environment.

- Central bank liquidity: Broad system-level liquidity conditions, policy channels, funding conditions, reserves, and financial-condition transmission.

- Quantitative easing: Asset purchases, balance-sheet expansion, reserve creation, yield pressure, and the financial-conditions effects of large-scale purchases.

- Quantitative tightening: Balance-sheet runoff, reserve drainage, duration supply, and the liquidity effects of reducing central-bank holdings.

- Forward guidance: Central-bank communication, expected rates, expected liquidity settings, and the future policy path.

- Central bank balance sheet: Assets, liabilities, reserves, facilities, and the accounting structure behind liquidity conditions.

- Open-market operations: Policy implementation through money-market operations, reserve management, and short-term rate control.

- Central bank liquidity swaps: Cross-border liquidity lines, dollar funding backstops, and official arrangements designed to ease foreign-currency funding pressure.

Official Sources, Data, and Market Interpretation

Central-bank liquidity often touches official data and operational details. Current values, facility terms, counterparty arrangements, and operation schedules require dated official sources or primary data endpoints because those details can change.

Data boundary: A central-bank-liquidity chart can answer what a specific series did over a specific period. It cannot, by itself, explain whether liquidity is broad, narrow, precautionary, stress-related, mechanically risk-supportive, or risk-negative for markets.

The stronger market-structure question is which channel changed, why it changed, whether it affects reserves or funding conditions, and whether other cross-asset evidence confirms or contradicts the liquidity read.

What Central Bank Liquidity Does Not Prove

Central-bank liquidity can influence financial conditions, funding pressure, rate expectations, and risk appetite, but it does not automatically predict asset prices. The same liquidity observation can mean different things depending on inflation, growth, credit spreads, real yields, dollar pressure, bank funding conditions, and market positioning.

Limitation: Central-bank liquidity is not a direct market-action signal, an asset-price guarantee, or a complete risk-on/risk-off model. Liquidity interpretation and market action are separate questions.

Common mistake: Treating QE as the whole liquidity picture can blur the difference between asset purchases, open-market operations, balance-sheet reserves, forward guidance, swap lines, and bank-level liquidity conditions.

Bank liquidity and central-bank liquidity can interact, but they are not identical. Bank liquidity focuses on the liquidity position and funding resilience of banks. Central-bank liquidity focuses on policy channels, balance-sheet tools, reserve conditions, and official facilities that can affect the wider financial system.

Central Bank Liquidity Route Example

A market observer looking at a central-bank liquidity chart may first need a data endpoint and a source date. A question about how liquidity enters the system points toward the balance-sheet or open-market-operations route. A question about dollar funding pressure points toward the liquidity-swaps route.

The practical distinction is channel first, interpretation second. Once the channel is clear, the liquidity read can be compared with rates, credit, DXY pressure, risk appetite, and broader market-structure evidence.