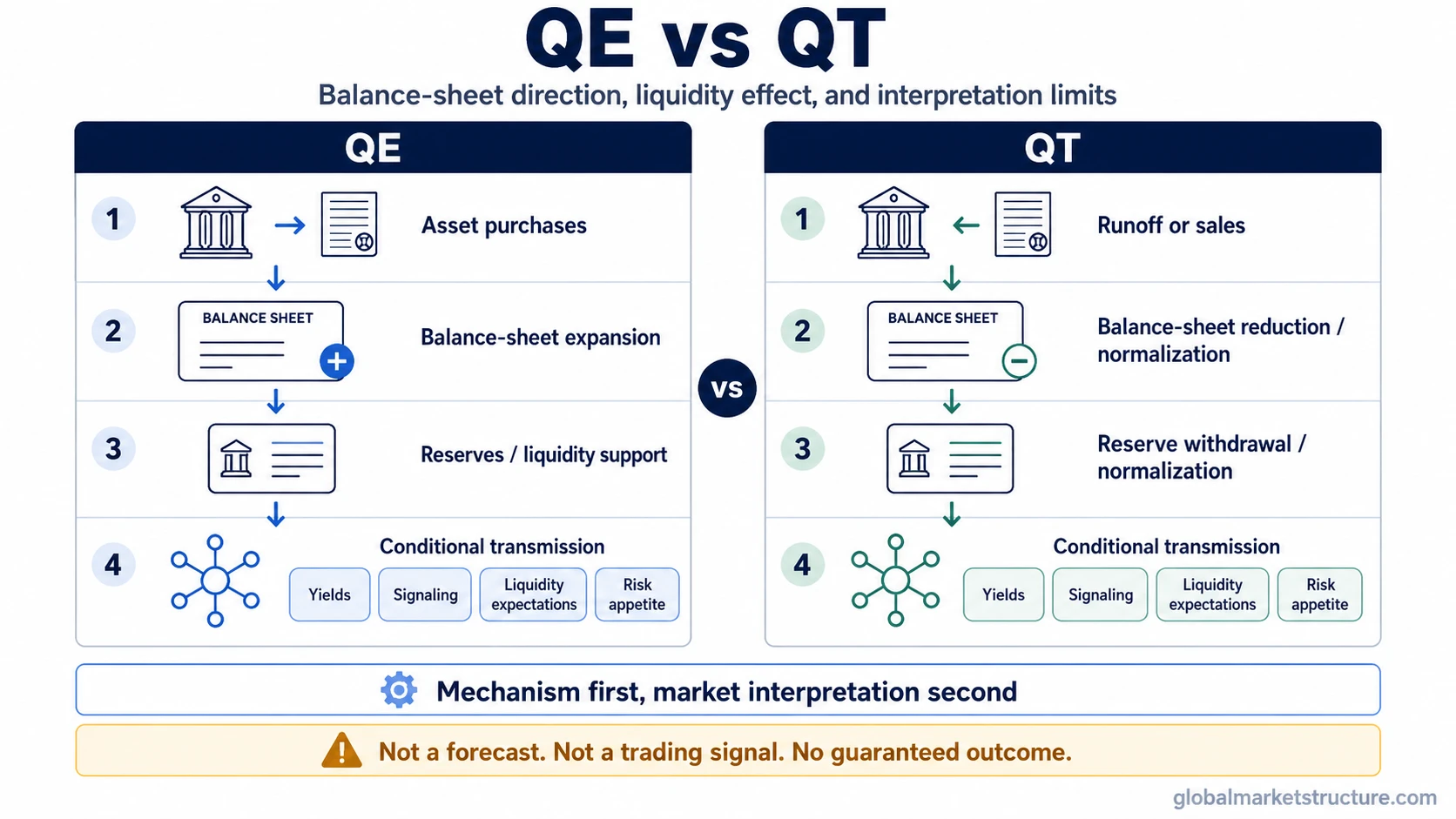

QE and QT describe opposite central-bank balance-sheet directions. Quantitative easing usually means asset purchases that expand the balance sheet and add reserve or liquidity support. Quantitative tightening usually means runoff or sales that reduce or normalize the balance sheet and withdraw part of that support. Neither label alone determines what bonds, equities, credit, the dollar, or risk assets must do.

Key Points

- QE expands a central-bank balance sheet through asset purchases.

- QT reduces or normalizes a central-bank balance sheet through runoff or sales.

- QE and QT are balance-sheet tools, not the same thing as policy-rate changes.

- Market effects depend on transmission through yields, reserves, credit, policy signaling, Treasury supply, growth expectations, and risk appetite.

- The useful distinction is mechanism first, market interpretation second.

QE vs QT: The Core Difference

QE, or quantitative easing, is a balance-sheet expansion process. A central bank buys assets, commonly government bonds or other eligible securities, and those purchases increase the asset side of its balance sheet. The matching liability side usually shows up through higher reserves or settlement balances in the banking system.

QT, or quantitative tightening, is a balance-sheet reduction or normalization process. A central bank allows securities to mature without full reinvestment, or in some cases sells assets, so the balance sheet becomes smaller than it would otherwise be. That process can reduce reserve balances, liquidity support, and the policy signal that came with earlier asset purchases.

The comparison is not “stocks up” versus “stocks down.” QE and QT change the liquidity and policy-transmission backdrop. Asset prices still depend on the surrounding regime, including rates, inflation expectations, credit conditions, growth expectations, Treasury issuance, reserve scarcity, and market risk appetite.

QE vs QT Comparison Table

| Comparison point | QE | QT |

|---|---|---|

| Full term | Quantitative easing | Quantitative tightening |

| Policy stance | Usually associated with monetary accommodation when conventional rate cuts are limited or when liquidity support is needed. | Usually associated with balance-sheet normalization or liquidity withdrawal after a period of accommodation. |

| Balance-sheet direction | Expansion. | Reduction or normalization. |

| Central-bank action | Asset purchases increase the central bank’s holdings of securities. | Securities mature without full reinvestment, or assets are sold, reducing holdings over time. |

| Reserve or liquidity effect | Usually adds reserves or settlement balances and can support liquidity conditions. | Usually withdraws or normalizes reserve balances and can reduce liquidity support. |

| Policy-rate relationship | Separate from policy-rate cuts, though both can be used in accommodative settings. | Separate from policy-rate hikes, though both can appear in tighter policy settings. |

| Yield and signaling channel | Can influence longer-term yields, term premium, liquidity expectations, and policy signaling. | Can affect term premium, reserve availability, liquidity expectations, and the signal that emergency support is being reduced. |

| Market interpretation limit | QE is not an automatic asset-price forecast or buy signal. | QT is not an automatic bearish forecast or sell signal. |

| Deeper concept route | Use the dedicated quantitative easing explanation for deeper balance-sheet expansion mechanics. | Use the dedicated quantitative tightening explanation for deeper runoff, sales, and balance-sheet reduction mechanics. |

How QE and QT Change the Balance Sheet and Liquidity Conditions

QE starts with central-bank asset purchases. When the central bank buys securities, it increases its asset holdings. The other side of the balance sheet typically appears as more reserves or settlement balances in the banking system. That does not mean liquidity reaches every market equally, but it can ease liquidity pressure, change expectations around policy support, and influence the pricing of duration, credit, and risk assets.

QT works in the opposite balance-sheet direction. If securities mature and are not fully replaced, or if securities are sold, the central bank’s holdings decline. The liability side can shrink as reserves or settlement balances are drained from the system. The effect depends on how abundant reserves are, how Treasury issuance is absorbed, how money markets adjust, and whether investors view the process as predictable normalization or as a source of liquidity strain.

The policy-rate channel is related but separate. A central bank can change short-term policy rates without changing the size of its balance sheet. It can also adjust balance-sheet policy while holding policy rates steady. QE and QT matter because they affect the quantity, composition, and signaling of central-bank support, not because they are simply another name for rate cuts or rate hikes.

The central-bank balance sheet is the accounting surface where these changes become visible. The market interpretation then depends on how that accounting change moves through reserves, yields, collateral demand, credit conditions, and risk appetite.

Why QE and QT Are Often Confused

QE and QT are often described as opposites because one expands the balance sheet and the other reduces it. That shortcut is useful, but it can hide the real mechanism. The important distinction is not only the direction of the balance sheet. It is the way asset purchases, runoff, sales, reserves, policy signaling, and liquidity expectations interact.

QE is sometimes reduced to “money printing,” but that phrase is too blunt for market-structure analysis. Asset purchases can create reserves and influence liquidity conditions, but the market effect depends on banking-system behavior, collateral conditions, risk demand, and the broader policy setting. A reserve increase is not the same thing as a guaranteed increase in lending, spending, or asset prices.

QT is sometimes reduced to “market bearishness,” but that is also too blunt. Balance-sheet runoff can remove liquidity support, but the effect depends on the pace of runoff, whether reserves remain abundant, how Treasury supply is absorbed, whether credit spreads are calm or widening, and whether risk appetite is already fragile.

QT can also be active or passive. Passive QT usually means securities mature and are not fully reinvested. Active QT means assets are sold outright. Both can reduce the balance sheet, but the market impact can differ because outright sales may create a more direct supply and signaling effect than predictable runoff.

Same Central-Bank Setting, Different Signal

Scenario: A central bank has used its balance sheet during a period of market stress or weak demand. Later, conditions change. Inflation pressure, reserve abundance, or policy normalization becomes the dominant concern.

QE reading: If the central bank is buying assets and expanding its balance sheet, the signal is balance-sheet support. The mechanism runs through asset purchases, higher reserves or settlement balances, lower liquidity stress, and a stronger expectation that policy is leaning toward accommodation.

QT reading: If the central bank is allowing assets to run off or selling assets, the signal is balance-sheet reduction. The mechanism runs through smaller asset holdings, lower reserve or liquidity support, and a policy message that earlier accommodation is being reduced or normalized.

Diagnostic distinction: The label depends on the balance-sheet operation. Purchases that expand holdings point to QE. Runoff or sales that reduce holdings point to QT. Market interpretation comes after that classification, not before it.

What QE and QT Do Not Tell You by Themselves

False reading: QE does not automatically mean risk assets should rise, and QT does not automatically mean risk assets should fall.

QE can support liquidity expectations, reduce stress, and influence longer-term yields, but asset-price outcomes still depend on inflation, earnings expectations, credit spreads, fiscal supply, currency pressure, and investor positioning. QE in a weak growth environment can carry a different market message than QE during a temporary liquidity shock.

QT can reduce balance-sheet support, but its effect depends on the starting level of reserves, the speed of runoff, Treasury issuance, money-market conditions, bank balance-sheet constraints, and whether investors view the process as orderly. QT can be easier for markets to absorb when reserves remain abundant and risk appetite is stable. It can become more important when reserves are scarce, credit spreads widen, or funding conditions tighten.

The practical market-structure question is not whether QE or QT is “bullish” or “bearish” in isolation. The stronger question is how the balance-sheet signal interacts with yields, credit, DXY, liquidity demand, policy signaling, growth expectations, and cross-asset confirmation.

When to Read Quantitative Easing or Quantitative Tightening

Use the QE concept when the question is about asset purchases, balance-sheet expansion, reserve creation, liquidity support, or the policy signal created by central-bank buying. Quantitative easing is the deeper route for the expansion side of the comparison.

Use the QT concept when the question is about runoff, asset sales, balance-sheet reduction, reserve withdrawal, or the removal of earlier liquidity support. Quantitative tightening is the deeper route for the reduction side of the comparison.

Use the asset-price transmission angle only after the balance-sheet distinction is clear. QE and asset-price transmission depends on liquidity expectations, yields, portfolio rebalancing, policy signaling, credit conditions, and risk appetite rather than on the QE label alone.

FAQ

What is the main difference between QE and QT?

QE expands a central-bank balance sheet through asset purchases. QT reduces or normalizes a central-bank balance sheet through runoff or sales. The core difference is balance-sheet direction and the liquidity support attached to that direction.

Is QT just the opposite of QE?

QT is the opposite of QE in balance-sheet direction, but the market effect is not a simple mirror image. The effect depends on the starting level of reserves, the pace of runoff or sales, Treasury supply, credit conditions, policy signaling, and risk appetite.

Does QE always increase asset prices?

No. QE can support liquidity expectations and influence yields, but asset prices still depend on growth, inflation, earnings expectations, credit spreads, currency pressure, investor positioning, and broader market conditions.

Does QT always make markets fall?

No. QT can reduce liquidity support, but markets may absorb it differently depending on reserve abundance, runoff pace, funding conditions, Treasury issuance, credit spreads, and the strength of risk appetite.

Are QE and QT the same as interest-rate policy?

No. QE and QT are balance-sheet tools. Interest-rate policy changes the short-term policy-rate setting. A central bank can adjust one channel without changing the other, although the two channels often interact in the broader policy regime.