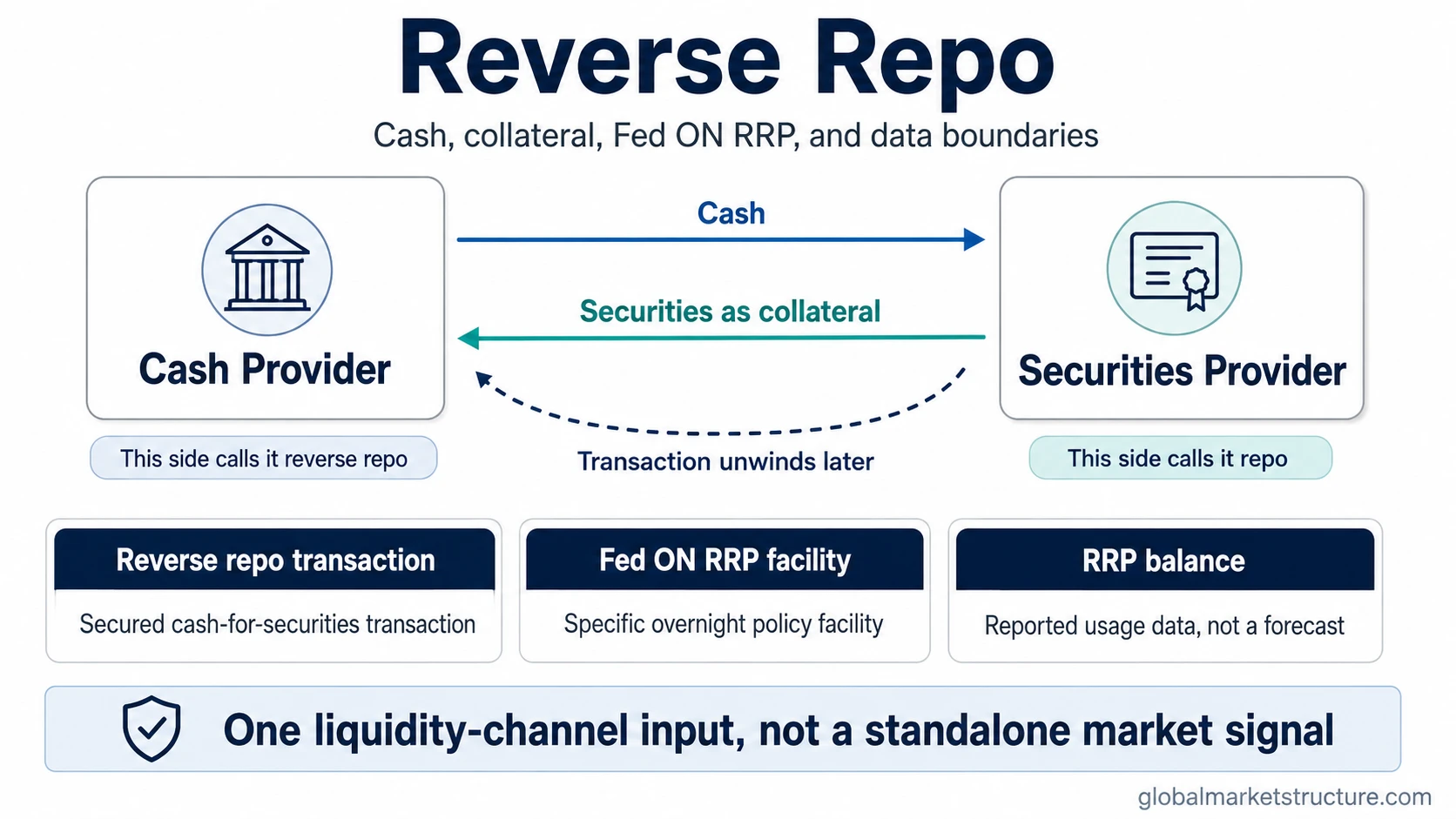

A reverse repo is a secured money-market transaction where one party sells securities for cash and agrees to buy them back later. From the cash provider’s side, it is a way to place cash against collateral. From the securities provider’s side, the same transaction is a repo.

In market-structure analysis, reverse repo usually matters because of the Federal Reserve’s overnight reverse repo facility, often called ON RRP. That facility can absorb cash from eligible money-market participants and leave securities with them temporarily. The resulting balances can help frame liquidity conditions, but they are not a standalone forecast for stocks, bonds, or risk assets.

- A reverse repo is a collateralized transaction that reverses at agreed terms.

- The same deal can be called a repo or reverse repo depending on which side of the transaction is being described.

- Fed ON RRP is a specific policy-implementation facility, not the whole reverse repo market.

- RRP balances can affect liquidity interpretation, but they do not function as a direct market-direction signal.

What Is a Reverse Repo?

A reverse repo, or reverse repurchase agreement, is the cash-provider side of a repurchase agreement. One party provides cash and receives securities as collateral. The other party receives cash and agrees to repurchase the securities later, usually with an interest component embedded in the terms.

Short definition: A reverse repo is a secured transaction where cash is placed with a counterparty in exchange for securities that are returned when the transaction unwinds.

The term is perspective-based. If a dealer receives cash and delivers securities, that dealer may describe the transaction as a repo. If a money-market fund provides cash and receives securities, that fund may describe the same transaction as a reverse repo.

| Question | Answer | Market-structure meaning |

|---|---|---|

| What type of instrument is it? | A secured money-market transaction | Cash and collateral move temporarily between counterparties. |

| Why is the term confusing? | Repo and reverse repo describe opposite sides of the same deal. | The label depends on whether the observer is following the cash borrower or the cash lender. |

| Why do macro traders watch it? | Fed ON RRP can absorb excess cash from eligible participants. | Large balances may reveal where short-term cash is being parked inside the monetary system. |

| What does it not prove? | It does not prove a market direction by itself. | RRP must be read beside reserves, Treasury cash balances, rates, credit, and risk appetite. |

How a Reverse Repo Works

The mechanics are simple, but the interpretation depends on the institution involved. A cash-rich participant places cash with another party. In return, it receives securities as collateral. At the agreed maturity, the securities go back and the cash returns with the agreed rate effect.

| Step | Cash provider | Securities provider | Interpretation |

|---|---|---|---|

| Opening leg | Provides cash | Provides securities | Cash is temporarily exchanged for collateral. |

| During the transaction | Holds securities as collateral | Uses the cash for the term of the agreement | The transaction is secured rather than unsecured lending. |

| Closing leg | Receives cash back | Receives securities back | The transaction unwinds at the agreed terms. |

| Label used | Reverse repo | Repo | The same transaction is described from two opposite perspectives. |

Illustrative scenario: A money-market fund has excess overnight cash. It places that cash with a counterparty and receives Treasury collateral. The next day, the transaction reverses. The fund has used a secured overnight placement, while the counterparty has temporarily financed securities with cash.

Repo vs Reverse Repo

Repo and reverse repo are not two unrelated markets. They are two sides of secured financing. A repo describes the side that sells securities and agrees to repurchase them. A reverse repo describes the side that provides cash and receives securities as collateral.

Practical distinction: The repo side is usually associated with borrowing cash against securities. The reverse repo side is usually associated with placing cash against securities.

The broader repo market includes many participants, collateral types, maturities, dealer relationships, and funding pressures. Reverse repo is the specific opposite-side label inside that secured-financing structure.

How the Fed Uses Reverse Repos

The Federal Reserve’s overnight reverse repo facility is a specific policy-implementation tool. Eligible counterparties can invest cash overnight with the New York Fed through a reverse repo transaction, receiving Treasury securities temporarily under an agreement that unwinds later. From the Fed’s perspective, the transaction temporarily absorbs cash from eligible money-market counterparties and creates an offsetting liability structure on the central-bank balance sheet.

The facility is closely watched because it can reveal how much cash certain institutions prefer to park at the Fed rather than deploy elsewhere in short-term money markets. High usage can reflect abundant cash, relative rate incentives, money-market fund behavior, collateral conditions, or limited private-market alternatives.

Data boundary: Current ON RRP balances and operational parameters belong to dated official data sources. A conceptual reverse repo explanation should not behave like a live tracker.

| Term | What it means | Boundary |

|---|---|---|

| Reverse repo transaction | A secured cash-for-securities transaction. | The label depends on which side of the transaction is being described. |

| Fed ON RRP facility | A specific Federal Reserve overnight facility. | It is a policy-implementation facility, not the entire reverse repo market. |

| RRP balance | A reported usage or data series. | It must be read as dated data, not as a full liquidity model. |

Does Reverse Repo Drain Liquidity?

Reverse repo can absorb cash from eligible participants while the transaction is outstanding. In that mechanical sense, Fed ON RRP can reduce the amount of cash immediately circulating through parts of the private money-market system.

The market interpretation is narrower than the phrase “drain liquidity” often suggests. RRP usage does not describe all liquidity. It does not fully describe bank reserves, Treasury cash balances, credit creation, bank balance-sheet capacity, collateral scarcity, money-market fund incentives, or risk appetite.

That is why reverse repo is better treated as one liquidity-channel input, not as a complete net liquidity model. A falling RRP balance may release cash from the facility, but the impact depends on where that cash goes and what is happening elsewhere in the monetary system.

What Reverse Repo Does Not Tell You

- It does not predict stocks by itself. RRP balances can influence liquidity interpretation, but they do not create a direct buy or sell signal.

- It is not the same as net liquidity. Net liquidity usually combines multiple balance-sheet and funding variables.

- It is not the whole repo market. It describes one side of secured financing and, in Fed context, one specific facility.

- It is not risk-free in every private setting. Collateral, counterparty quality, legal terms, and liquidity conditions still matter outside official facility context.

- It is not a complete monetary-policy stance. Policy rates, reserves, Treasury issuance, balance-sheet policy, and financial conditions all matter.

Reverse repo is most useful when it is read beside money-market rates, reserve balances, Treasury General Account movement, credit conditions, and safe-collateral demand. On its own, it is a plumbing signal, not a market forecast.

Why Reverse Repo Matters for Market Structure

Reverse repo connects cash, collateral, short-term rates, and central-bank implementation. When a large amount of cash moves into an overnight reverse repo facility, that cash is not being used in the same way as bank lending, private repo financing, or risk-asset allocation. It is being parked through a secured official channel.

The implication is not automatically bullish or bearish. The stronger question is what the balance reveals about the surrounding regime: excess cash, money-market incentives, reserve conditions, short-term rate floors, collateral demand, and the willingness of private markets to absorb liquidity.

For that reason, reverse repo belongs in liquidity and policy plumbing analysis rather than in direct market-call language.

Related Concepts

Repo market: Use the broader repo-market concept for secured funding structure, dealer financing, collateral, and systemic repo-market stress.

Central-bank balance sheet: Use the central-bank balance sheet concept for the broader relationship between assets, liabilities, reserves, and policy implementation.

Net liquidity: Use net liquidity for multi-variable liquidity frameworks that combine RRP with other monetary and funding indicators.

FAQ

What is a reverse repo in simple terms?

A reverse repo is a secured transaction where cash is placed with a counterparty in exchange for securities that are returned when the transaction reverses.

Is reverse repo the same as repo?

Repo and reverse repo describe opposite sides of the same transaction. The repo side receives cash and provides securities. The reverse repo side provides cash and receives securities.

What is Fed ON RRP?

Fed ON RRP is the Federal Reserve’s overnight reverse repo facility. Eligible counterparties can invest cash overnight with the New York Fed through a reverse repo transaction and receive Treasury securities temporarily under an agreement that unwinds later.

Does reverse repo drain liquidity?

Fed reverse repo usage can absorb cash while the transaction is outstanding, but it is only one part of liquidity interpretation. It must be read with reserves, Treasury cash balances, rates, credit, and broader funding conditions.

Does reverse repo predict the stock market?

No. Reverse repo balances can provide liquidity context, but they do not predict stocks or create a standalone market-direction signal.