The global liquidity cycle is the expansion and contraction of financing, credit, and liquidity availability across the global financial system. It moves through central-bank liquidity, private credit creation, collateral and funding markets, and cross-border flows. It is a macro and liquidity-cycle concept, not a standalone asset-price forecast, recession timer, or trade signal.

At its simplest, the cycle describes whether the system is becoming easier or harder to finance. When liquidity expands, balance-sheet capacity, credit creation, and cross-border funding can support risk-taking. When liquidity contracts, refinancing, collateral use, wholesale funding, and credit extension can become more constrained.

The important distinction is that global liquidity is the broader condition, while the global liquidity cycle describes how that condition changes through time. The cycle is about movement, transmission, and constraint, not one fixed data series.

What the global liquidity cycle means

The global liquidity cycle describes the changing ease of financing across policy, bank and non-bank intermediation, collateral, wholesale funding, and cross-border dollar channels. It expands when financing is easier to obtain and contracts when balance sheets, funding markets, or credit channels become more restrictive.

- It is broader than money supply: money aggregates can matter, but they do not capture every credit, collateral, funding, and cross-border channel.

- It is broader than central-bank balance sheets: central banks influence liquidity, but private balance sheets and credit intermediaries also transmit or restrict financing.

- It is broader than a proxy: a liquidity proxy can summarize one measurement approach, but the proxy is not the whole concept.

- It is not a market signal by itself: liquidity conditions can affect the background environment, but market direction still depends on yields, credit, earnings, dollar pressure, positioning, and risk appetite.

How liquidity enters or leaves the system

Liquidity enters the system when financing channels become easier, balance sheets can expand, collateral is accepted more readily, and cross-border funding becomes more available. Liquidity leaves when the same channels tighten, become more expensive, or become less reliable.

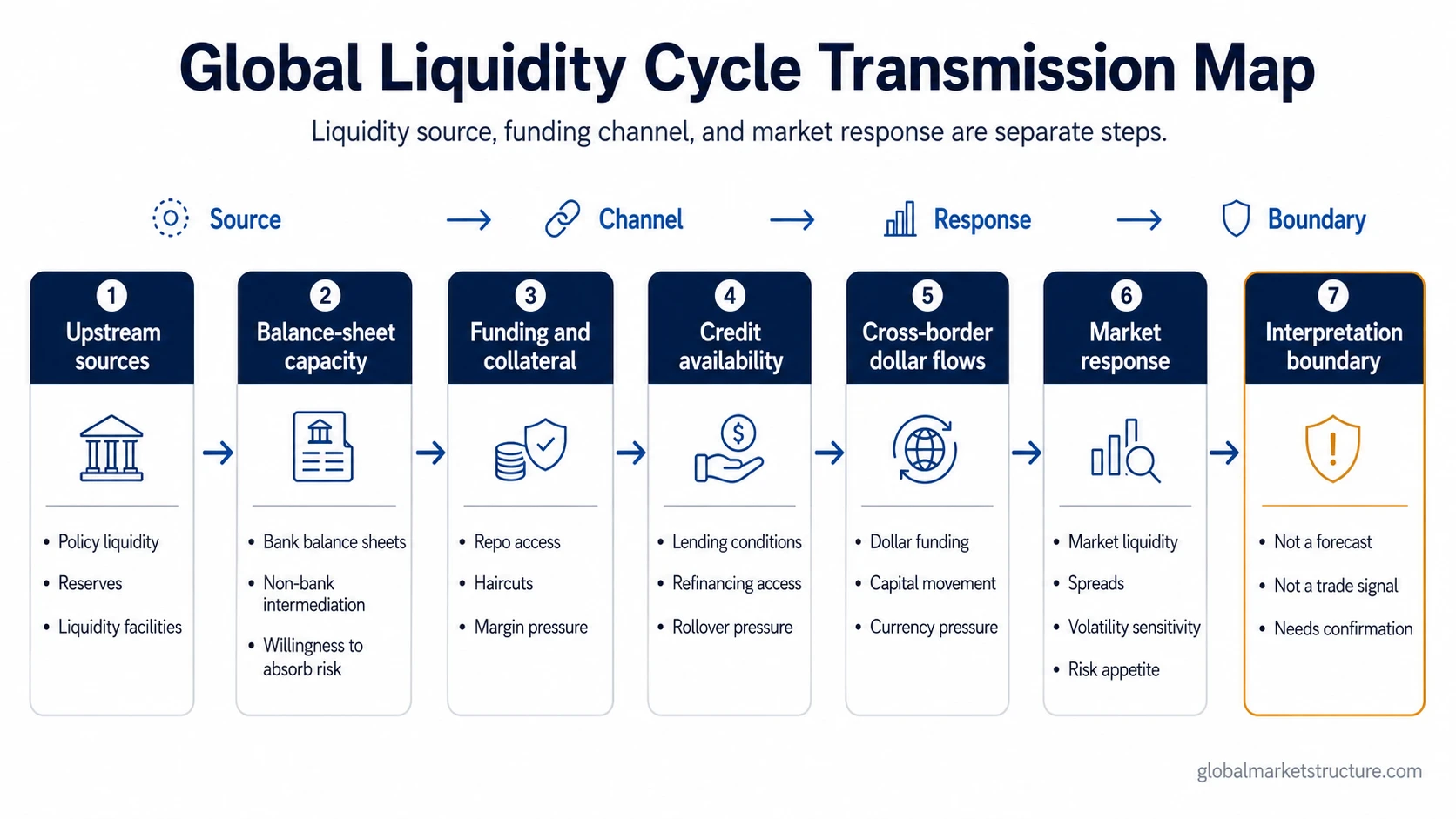

Main transmission channels

- Central-bank and policy liquidity: balance-sheet operations, reserves, liquidity facilities, and policy stance can alter the amount and price of financing available to the system.

- Private credit creation: banks and non-bank lenders can expand or restrict credit depending on capital, risk appetite, regulation, and borrower demand.

- Collateral and repo markets: financing can become easier when collateral is accepted smoothly and harder when haircuts, margin needs, or collateral scarcity rise.

- Wholesale funding and refinancing: borrowers can face pressure when short-term funding, rollover access, or refinancing terms deteriorate.

- Cross-border flows: global dollar availability, currency funding needs, and international balance-sheet flows can transmit liquidity pressure across regions.

- Risk appetite and balance-sheet willingness: even when policy liquidity is present, intermediaries must still be willing and able to take balance-sheet risk.

Source, channel, and false-reading boundaries

Liquidity interpretation becomes cleaner when the source, transmission channel, likely effect, and false reading are kept separate. A liquidity source can improve financing conditions without creating a mechanical asset-price outcome.

| Source or channel | What expands or contracts | What it can affect | False reading to avoid |

|---|---|---|---|

| Central-bank liquidity | Reserves, liquidity facilities, policy balance-sheet conditions | System funding backdrop, reserve availability, confidence in liquidity backstops | Assuming central-bank expansion automatically means risk assets rise |

| Private credit creation | Bank lending, non-bank credit, leverage capacity | Borrower financing, credit availability, balance-sheet growth | Treating policy liquidity as enough when private credit is still tightening |

| Collateral and repo funding | Collateral acceptance, haircuts, margin needs, repo access | Leveraged balance sheets, refinancing pressure, forced deleveraging risk | Reading calm asset prices as proof that funding pressure is absent |

| Wholesale refinancing | Rollover access, funding cost, maturity pressure | Credit stress, liquidity preference, risk appetite | Ignoring maturity walls or refinancing terms because headline liquidity looks supportive |

| Cross-border dollar flows | Dollar funding availability, capital movement, foreign balance-sheet demand | Global financing conditions, currency pressure, international risk transmission | Assuming domestic liquidity measures capture the full global funding condition |

| Market risk appetite | Willingness to intermediate, lend, hold risk, or provide depth | Market liquidity, spreads, volatility sensitivity, asset correlation | Confusing a supportive backdrop with a timing signal |

Upstream liquidity is not the same as downstream market response

The global liquidity cycle has an upstream and downstream side. Upstream liquidity describes where financing becomes easier or tighter. Downstream market response describes how that financing condition moves through credit, funding, currencies, volatility, and asset markets.

The two sides can diverge. Policy liquidity may expand while lenders remain cautious. Cross-border dollar pressure may rise even when a domestic liquidity measure looks stable. Funding markets may tighten before broad equity indices reflect stress. The cycle matters because it identifies pressure or relief inside the financing system, not because it gives a complete market forecast.

A stronger interpretation usually requires confirmation from credit spreads, funding stress, dollar conditions, volatility behavior, breadth, and risk appetite. Liquidity is one part of the regime map, not the whole map.

Why global liquidity proxies can disagree

Global liquidity proxies can disagree because they measure different parts of the system. One proxy may emphasize central-bank balance sheets. Another may emphasize money aggregates, credit growth, dollar liquidity, foreign exchange reserves, financial conditions, or market-based stress. Each proxy can be useful, but none should be treated as the complete global liquidity cycle.

Proxy disagreement often reflects a real analytical problem: liquidity is not one pipe. It moves through multiple balance sheets and funding channels. A single chart can simplify the picture, but it can also hide whether the main change is coming from policy liquidity, private credit, collateral pressure, or cross-border dollar demand.

Illustrative scenario

Consider a period when central-bank liquidity is becoming more supportive, but private lenders remain cautious and cross-border dollar funding is still tight. A headline liquidity proxy may look better because the policy side has improved. At the same time, credit conditions may remain restrictive because lenders are not expanding balance sheets and borrowers face higher refinancing costs.

The tempting read is that improving liquidity should immediately support broad risk appetite. The incomplete part is transmission. If funding, collateral, credit, or cross-border channels are still constrained, the market response can remain uneven. The stronger case appears only when policy liquidity, private credit, funding conditions, and risk appetite begin to improve together. The weaker case persists when only one channel improves while the others remain tight.

Common misconception

The most common mistake is treating the global liquidity cycle as “liquidity up equals assets up.” That shortcut skips the channels between liquidity source and market response. A supportive liquidity backdrop can reduce pressure, improve refinancing conditions, or increase willingness to take risk, but it does not remove valuation risk, earnings risk, credit stress, dollar pressure, or positioning risk.

The opposite mistake also matters. Tight liquidity can increase pressure, but it does not prove immediate recession timing or a single asset-market direction. Markets can absorb tightening for a time if earnings are resilient, credit remains calm, or risk appetite stays firm. Liquidity changes the background condition; confirmation decides whether the background condition is becoming the dominant market driver.

How the global liquidity cycle differs from nearby concepts

The global liquidity cycle is easiest to separate from nearby concepts by asking what each term is trying to describe.

| Concept | Main question | Boundary |

|---|---|---|

| Global liquidity | How easy or difficult are global financing conditions? | Broader condition, not necessarily the movement through a cycle |

| Global liquidity cycle | How are global financing conditions expanding or contracting over time? | Cycle and transmission concept, not a standalone forecast |

| Market liquidity | How easily can assets trade without large price impact? | Market-trading condition, not the entire financing system |

| Funding liquidity | How easily can participants obtain financing? | Funding access channel, not the full global cycle |

| Liquidity proxy | What measurement can represent part of liquidity conditions? | Measurement input, not the concept itself |

Why dollar conditions matter

Global liquidity is often connected to dollar conditions because the dollar sits at the center of many funding, trade, reserve, and cross-border balance-sheet relationships. When dollar funding becomes scarce or expensive, global borrowers and intermediaries can face tighter financing even if local liquidity conditions look more stable.

Dollar smile theory adds a separate lens because it focuses on how the dollar can behave during both strong U.S. growth and global stress. That matters for liquidity interpretation because dollar strength can reflect different regimes: growth confidence in one case, funding pressure or safety demand in another.

Clean interpretation sequence

A disciplined read separates four steps:

- Source: identify whether the change is coming from policy liquidity, private credit, collateral markets, wholesale funding, or cross-border flows.

- Transmission: check whether the source is actually moving through balance sheets, lending, refinancing, funding spreads, or currency channels.

- Market response: compare credit, yields, dollar conditions, volatility, breadth, and risk appetite.

- Boundary: avoid converting a liquidity condition into a forecast, recession clock, or trade trigger without confirmation.

The global liquidity cycle becomes more useful when it is read as a financing-regime backdrop. It becomes less useful when it is compressed into one chart, one policy action, or one directional market call.

FAQ

Is the global liquidity cycle the same as money supply?

No. Money supply can be one input, but the global liquidity cycle also involves credit creation, bank and non-bank balance sheets, collateral, repo, wholesale funding, cross-border dollar flows, and risk appetite.

Does the global liquidity cycle predict stock-market direction?

No. It can influence the background environment for risk-taking, but it does not determine asset direction by itself. Credit, yields, earnings, dollar pressure, positioning, and risk appetite can change the market response.

How is the global liquidity cycle different from global liquidity?

Global liquidity describes the broader availability of financing and liquidity. The global liquidity cycle describes how that availability expands or contracts over time and how the change moves through policy, credit, funding, and cross-border channels.

Can global liquidity proxies disagree?

Yes. Proxies can disagree because they measure different parts of the system, such as central-bank balance sheets, money aggregates, credit growth, dollar liquidity, reserves, or financial conditions. A proxy is a measurement input, not the full concept.