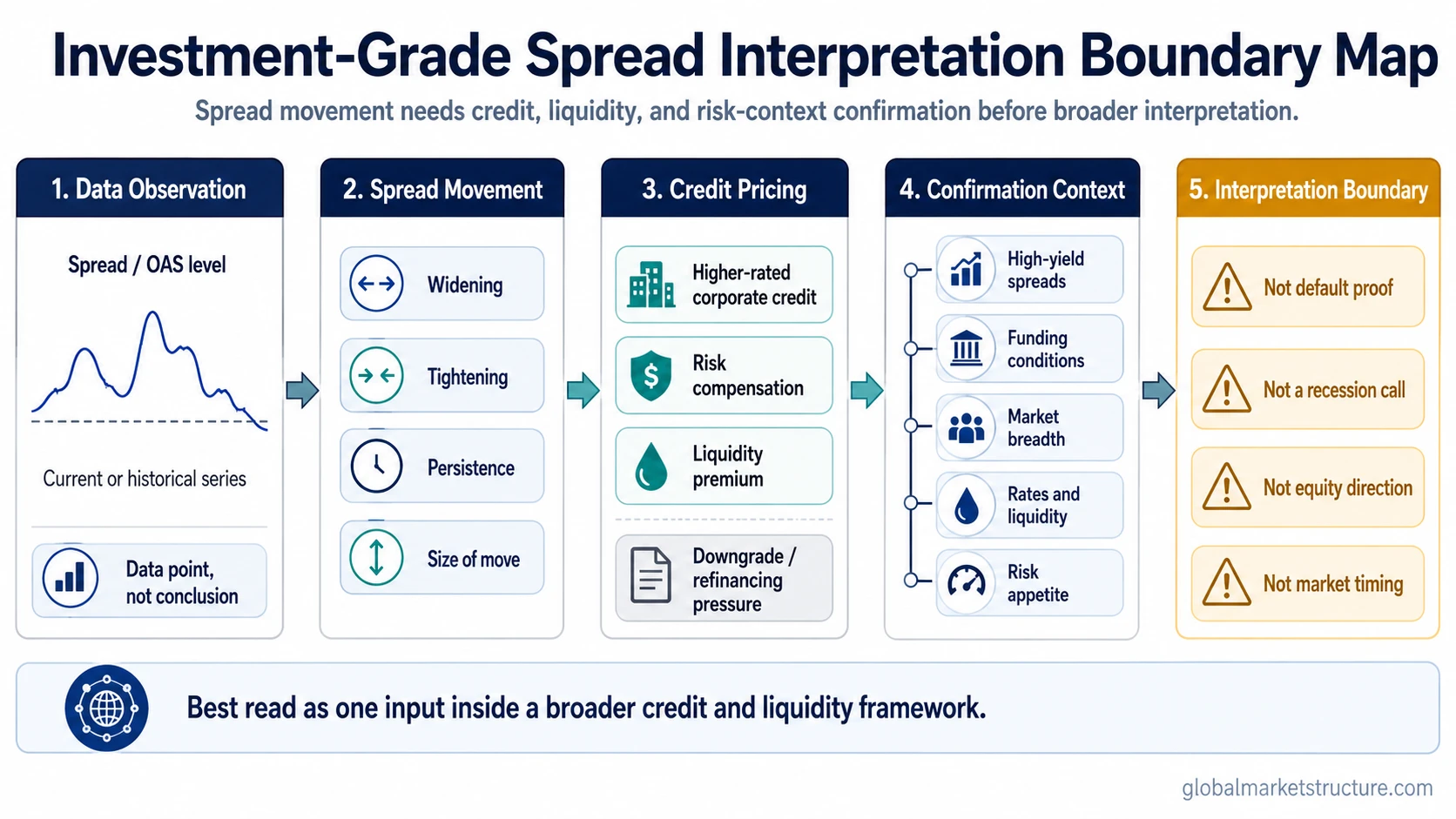

Investment-grade credit spreads are the extra yield compensation associated with higher-rated corporate debt relative to a safer benchmark, often measured as a spread or option-adjusted spread. Wider spreads can reflect higher demanded compensation for credit risk or tighter credit conditions, while tighter spreads can reflect easier credit pricing. The signal is an input, not a standalone default forecast, recession call, equity-market call, or trade instruction.

Definition: An investment-grade credit spread measures the yield difference between investment-grade corporate debt and a safer benchmark, such as a Treasury or comparable risk-free reference. The spread represents compensation for credit risk, liquidity conditions, and other bond-market risks attached to higher-rated corporate borrowers.

Classification: Investment-grade spreads sit inside the broader family of credit spreads, but they focus on higher-rated corporate debt rather than speculative-grade debt, options strategies, or all forms of corporate borrowing.

What investment-grade credit spreads measure

Investment-grade spreads focus on how much extra yield investors demand to own higher-rated corporate bonds instead of safer benchmark debt. The spread is not the full bond yield. It is the extra compensation above the benchmark.

That distinction matters because benchmark yields can move for reasons unrelated to corporate credit risk. Treasury yields may rise because of inflation expectations, policy-rate repricing, term premium changes, or growth expectations. The investment-grade spread isolates the corporate-risk premium more directly than the full yield alone.

Many data series use option-adjusted spread, or OAS, because some bonds contain embedded optionality or cash-flow features that can affect yield comparison. In plain terms, OAS attempts to make the spread comparison cleaner by adjusting for option-like bond features before interpreting the extra compensation demanded by the market.

How widening and tightening are interpreted

When investment-grade spreads widen, investors are demanding more compensation to hold higher-rated corporate credit relative to safer benchmarks. That can reflect rising concern about credit quality, weaker risk appetite, reduced market liquidity, or tighter financial conditions.

When investment-grade spreads tighten, investors are accepting less extra compensation for holding higher-rated corporate credit. That can reflect stronger demand for corporate bonds, easier risk pricing, calmer credit conditions, or a broader willingness to hold risk assets.

The direction is useful, but the interpretation is conditional. A modest widening in investment-grade spreads during a broad rate repricing does not carry the same message as persistent widening alongside weaker funding conditions, wider high-yield spreads, falling breadth, and deteriorating risk appetite.

Investment-grade spreads versus nearby credit concepts

Several credit-market terms sound similar, but they do not measure the same thing.

| Concept | What it refers to | Main boundary |

|---|---|---|

| Investment-grade credit spreads | Extra yield compensation on higher-rated corporate debt relative to a safer benchmark. | Focused on investment-grade corporate credit, not all credit risk. |

| BBB spreads | Spreads on the lower-rated part of the investment-grade universe. | BBB is a subset of investment grade, not the whole category. |

| High-yield spreads | Spreads on speculative-grade corporate debt. | High-yield spreads usually react more strongly to default risk and risk appetite than higher-rated credit. |

| Generic credit spreads | A broad category covering many forms of risk compensation above safer benchmarks. | Investment-grade spreads are one family inside the broader credit-spread category. |

| Options credit spreads | An options strategy involving sold and bought option legs. | Options credit spreads are not corporate bond credit spreads. |

Why investment-grade spreads matter for financial conditions

Investment-grade spreads help show how the market is pricing higher-quality corporate borrowing. When spreads widen, corporate financing can become less attractive even if benchmark yields are not the only driver. That can matter for refinancing decisions, balance-sheet planning, and broader financial-condition interpretation.

The signal is usually cleaner when spread movement aligns with other credit and liquidity indicators. For example, widening investment-grade spreads may carry more weight when speculative-grade spreads are also widening, funding markets look less flexible, equity breadth is weakening, and risk appetite is falling across assets.

Investment-grade spreads can also move before realized nonpayment appears. Credit markets may reprice compensation for default risk, downgrade pressure, liquidity risk, or refinancing strain before actual defaults are visible in reported data.

A practical interpretation scenario

Imagine investment-grade spreads begin widening while major equity indices remain stable. One possible reading is that credit investors are repricing risk before equities respond. That may be possible, but the observation is incomplete on its own.

A stronger credit-condition interpretation would need confirmation from nearby signals: high-yield spreads widening, weaker funding access, reduced market depth, softer breadth, or a broader move toward safer assets. A weaker reading would occur if investment-grade spreads widen only slightly while liquidity remains firm, high-yield spreads stay contained, and broader risk appetite remains stable.

The useful distinction is between early risk repricing and a complete market forecast. Investment-grade spread widening can raise the level of caution in a credit framework, but it does not automatically define the next move in equities, bonds, or the economy.

What investment-grade spreads do not prove

Investment-grade spread widening does not prove that defaults are about to rise. It shows that the market is demanding more compensation for holding higher-rated corporate credit. That compensation may reflect default concern, liquidity risk, downgrade risk, risk aversion, or a mix of those forces.

It also does not prove that a recession, equity drawdown, or immediate risk-off move is unavoidable. Credit spreads are part of a broader market-structure framework. Their value improves when they are compared with funding liquidity, high-yield credit, rates, market breadth, volatility, and cross-asset behavior.

The common mistake is treating one spread series as a complete macro signal. Investment-grade spreads are useful because they narrow the credit-quality lens, but that same narrowness means they need confirmation before carrying broader regime weight.

Investment-grade versus high-yield boundary

Investment-grade and high-yield spreads both measure compensation above safer benchmarks, but they represent different credit-quality zones. Investment-grade spreads focus on higher-rated issuers. High-yield spreads focus on speculative-grade issuers, where default sensitivity is usually more direct.

The boundary becomes important when the two signals diverge. If investment-grade spreads stay calm while high-yield spreads widen, lower-quality credit may be absorbing stress first. If both widen together, the credit repricing may be broader. The investment grade versus high yield distinction matters because the two groups answer different credit-quality questions.

How to use the signal without overreading it

Investment-grade spreads work best as a credit-pricing input. They help classify whether higher-rated corporate credit is being priced with more or less caution, and whether that pricing is consistent with other financial-condition signals.

A live data series can show the current level of investment-grade spreads, but interpretation depends on the size, persistence, credit-quality breadth, and confirmation from adjacent liquidity and risk signals.

A cleaner interpretation usually asks four questions:

- Are spreads widening or tightening relative to their recent range?

- Is the move specific to investment-grade credit, or is it also appearing in lower-quality credit?

- Are funding, liquidity, breadth, and risk-appetite signals confirming the move?

- Is the move large and persistent enough to change the broader credit-condition reading?

Those questions keep the spread reading inside its proper role. The signal can support a broader market-structure view, but it should not replace the full evidence stack.

Investment Grade Credit Spreads FAQ

What are investment-grade credit spreads?

Investment-grade credit spreads are the extra yield compensation associated with higher-rated corporate bonds relative to a safer benchmark. They show how the market is pricing corporate credit risk inside the investment-grade universe.

What does it mean when investment-grade spreads widen?

Wider investment-grade spreads mean investors are demanding more compensation to hold higher-rated corporate credit. That can reflect tighter credit conditions, weaker risk appetite, liquidity pressure, or greater concern about corporate credit quality.

Are investment-grade spreads the same as high-yield spreads?

No. Investment-grade spreads focus on higher-rated corporate debt. High-yield spreads focus on speculative-grade debt, where default sensitivity and risk-appetite swings are usually stronger.

Do investment-grade credit spreads predict defaults?

They do not predict defaults by themselves. They can reflect changing compensation for credit risk before realized defaults appear, but they need confirmation from other credit, liquidity, and macro signals.

Are options credit spreads related to investment-grade credit spreads?

No. Options credit spreads are options strategies. Investment-grade credit spreads are bond-market measures of extra yield compensation on higher-rated corporate debt relative to safer benchmarks.