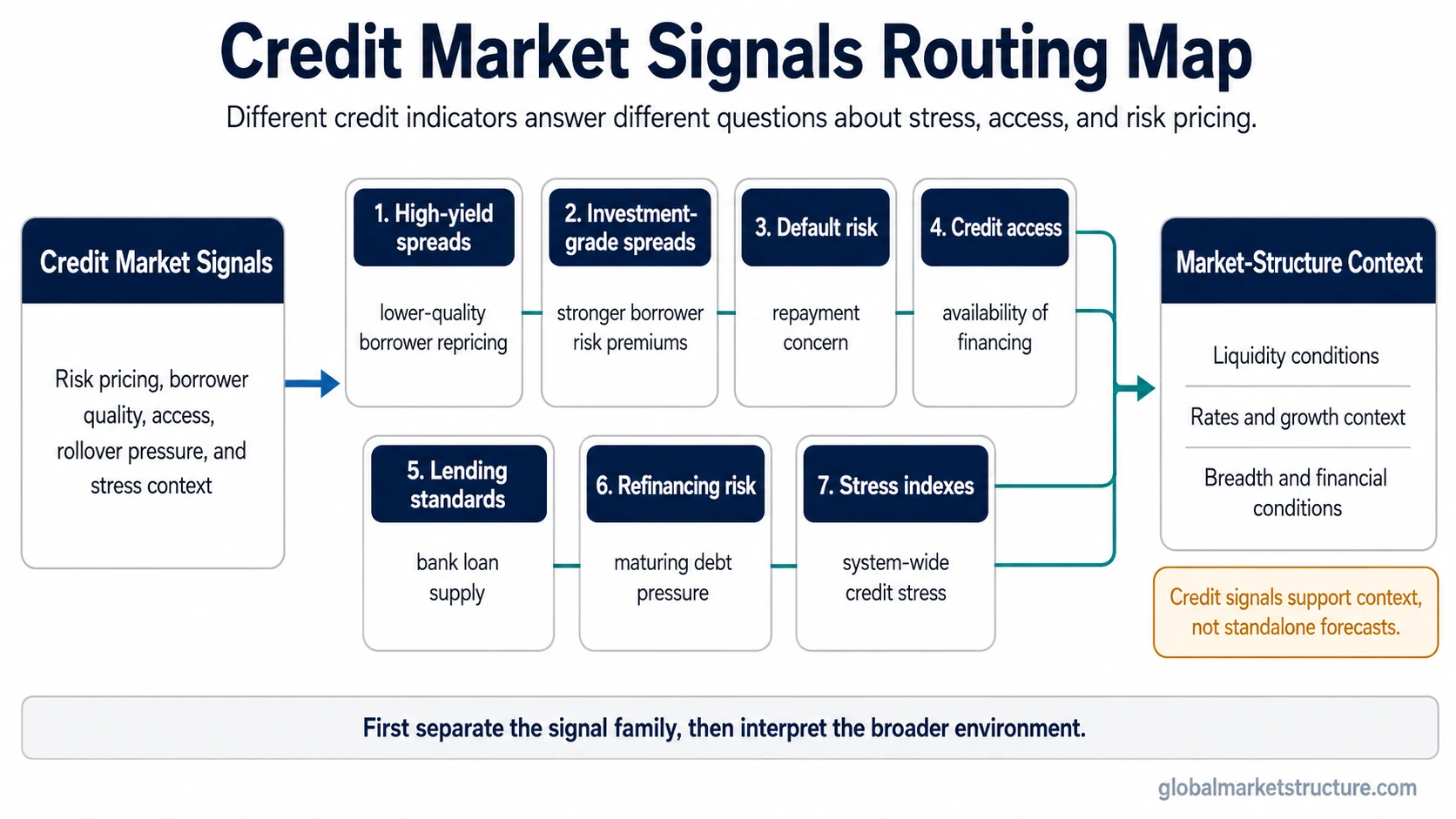

Credit market signals are credit-side indicators used to read credit-risk pricing, borrower funding access, default concern, refinancing pressure, and broader financial stress. They are not one signal: high-yield spreads, investment-grade spreads, default risk, lending standards, refinancing pressure, and stress indexes each answer a different question about credit conditions.

The useful first step is to identify which credit signal family is moving before interpreting the broader market environment. Credit deterioration can support a risk-environment view, but it is not a standalone recession forecast, equity-market signal, or trade instruction.

Credit signal families

Credit signals become clearer when they are separated by the question they answer. A spread signal is not the same as a default-risk signal, and restricted credit access is not the same as refinancing pressure.

| Signal family | Question it answers | Relevant credit concept |

|---|---|---|

| Lower-quality corporate credit | Are riskier borrowers being repriced more aggressively? | High-yield spreads |

| Higher-quality corporate credit | Are stronger corporate borrowers also facing wider risk premiums? | Investment-grade spreads |

| Repayment concern | Is the market becoming more concerned about missed payments or borrower failure? | Default risk |

| Credit availability | Are borrowers losing access to credit rather than only paying a higher spread? | Credit crunch |

| Broad spread behavior | Is the market demanding more compensation for credit risk across borrowers? | Credit spreads |

| Loan supply and bank behavior | Are lenders becoming more restrictive in how they extend credit? | Bank lending standards |

| Rollover pressure | Are borrowers facing more difficulty replacing maturing debt? | Refinancing risk |

| System-wide stress | Is credit stress broad enough to appear in wider financial-stress conditions? | Financial stress index |

How to choose the right credit signal

Different credit indicators can move at the same time, but they do not carry the same meaning. The practical distinction is whether the pressure is showing up in market pricing, borrower quality, credit access, debt rollover, or system-wide stress.

| Reader question | Best starting point | Interpretation boundary |

|---|---|---|

| Are lower-quality borrowers under pressure first? | High-yield spread behavior | Useful for risk appetite, but not a complete market forecast. |

| Is pressure spreading into stronger corporate credit? | Investment-grade spread behavior | More relevant when the concern is broader credit repricing. |

| Is repayment risk the main issue? | Default-risk indicators | Default concern is different from temporary spread volatility. |

| Are borrowers losing access to financing? | Credit-access and lending-standard signals | Access to credit can tighten even before a default cycle becomes obvious. |

| Is debt rollover becoming harder? | Refinancing pressure | Rollover risk matters most when maturing debt meets higher funding costs. |

| Is the signal broad enough to affect the market environment? | Financial stress and broader financial conditions | Credit signals become more meaningful when confirmed across related conditions. |

When several credit signals move together

A widening high-yield spread, tighter lending standards, and rising refinancing pressure can all point toward weaker credit conditions, but they do not describe the same mechanism. High-yield spreads show risk repricing in lower-quality credit. Lending standards show whether lenders are restricting access. Refinancing risk shows whether borrowers may struggle to replace maturing debt.

The interpretation becomes stronger when several families point in the same direction and the broader backdrop also shows tighter liquidity, weaker breadth, or deteriorating risk appetite. The interpretation weakens when one credit indicator moves alone while other credit, liquidity, and market-structure signals remain stable.

What credit signals do not prove by themselves

Credit market signals are interpretation inputs, not mechanical forecasts. Wider spreads, tighter lending standards, or a higher stress reading can warn that credit conditions are becoming less supportive, but one signal does not prove a recession, a risk-off regime, or an equity-market outcome.

- A credit-spread move does not automatically mean a recession is coming.

- A financial-stress reading is not a trading signal.

- A credit crunch is not the same thing as default risk.

- High-yield and investment-grade signals should be separated because they represent different borrower-quality segments.

- Credit signals need confirmation from liquidity, rates, market breadth, risk appetite, and broader financial conditions.

Credit market signals versus nearby concepts

Credit market signals describe the credit side of the macro environment. They overlap with broader market-structure analysis, but they should not replace the concepts that explain each mechanism in more detail.

| Concept | How it differs | Use it when |

|---|---|---|

| Investment grade vs high yield | Investment grade vs high yield separates stronger borrower credit from lower-quality borrower credit. | The question is whether stress is concentrated in riskier credit or spreading into higher-quality credit. |

| Financial conditions | Financial conditions combine credit, rates, liquidity, volatility, and market pricing into a broader environment view. | The question is whether credit deterioration is part of a wider tightening in market conditions. |

| Credit crunch | Credit crunch focuses on access to credit, not only the price of credit. | The question is whether lenders are reducing availability or borrowers are being shut out of financing. |

| Financial stress index | A stress index combines multiple stress measures instead of isolating one spread or borrower segment. | The question is whether stress appears broad enough to affect the financial system rather than one narrow credit segment. |

Credit Market Signals FAQ

Are credit market signals the same as credit spreads?

No. Credit spreads are one major credit-market signal, but the broader group also includes default risk, lending standards, refinancing pressure, credit availability, and stress indicators.

Do credit market signals predict recessions?

Credit signals can show that risk pricing, financing access, or borrower stress is deteriorating, but they do not predict recessions by themselves. They need confirmation from broader liquidity, rates, growth, breadth, and financial-condition evidence.

Why separate high-yield and investment-grade spreads?

High-yield spreads focus on lower-quality borrowers, while investment-grade spreads focus on stronger corporate borrowers. The difference matters because stress often appears unevenly across borrower-quality segments.