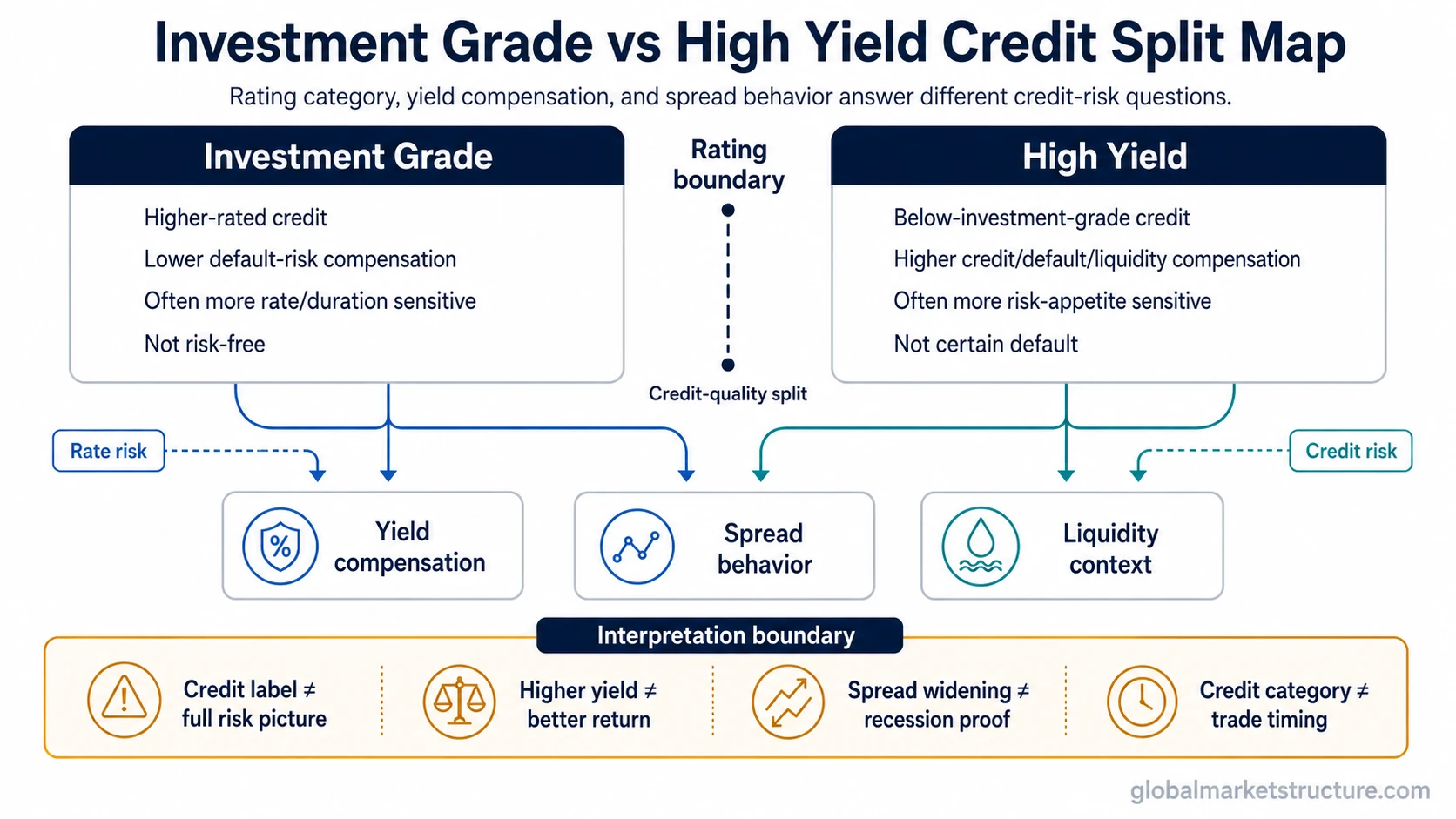

Investment grade vs high yield separates higher-rated credit from below-investment-grade credit. Investment grade usually carries lower default-risk compensation and lower yield because issuer credit quality is stronger. High yield usually pays more because investors demand compensation for default risk, liquidity risk, and risk-appetite sensitivity. Neither label alone proves safety, default, recession risk, equity direction, or trade timing.

Key points

- Investment grade refers to higher-rated credit, usually associated with stronger issuer credit quality.

- High yield refers to below-investment-grade credit, often called speculative-grade or junk credit.

- Higher yield is compensation for risk, not proof of better return.

- Credit spreads need rate, liquidity, default-risk, and risk-appetite context before broader interpretation.

- Investment grade is not risk-free, and high yield does not mean default is certain.

What separates investment grade from high yield?

The core difference is credit quality. Investment-grade issuers are generally viewed as having stronger capacity to meet debt obligations. High-yield issuers sit below the investment-grade boundary and therefore require higher compensation because the market attaches more credit risk, refinancing risk, liquidity risk, or default-risk sensitivity to the debt.

| Category | Investment grade | High yield | Interpretation boundary |

|---|---|---|---|

| Credit quality | Higher-rated corporate or sovereign credit | Below-investment-grade credit | Classification does not remove risk or guarantee outcome. |

| Rating boundary | Usually at or above the lower investment-grade threshold | Usually below the investment-grade threshold | Exact rating symbols depend on the agency scale. |

| Yield compensation | Lower compensation for credit risk | Higher compensation for credit, default, and liquidity risk | Higher yield is not automatically better return. |

| Default-risk sensitivity | Usually lower, but not zero | Usually higher, but not certain default | Default risk must be interpreted with issuer, cycle, and funding context. |

| Spread behavior | Often moves with credit quality, liquidity, and rate conditions | Often moves more sharply with default-risk compensation and risk appetite | Spread movement is a pricing signal, not a standalone forecast. |

| Rate sensitivity | Can be more exposed to duration and interest-rate repricing | Can be more exposed to credit and refinancing pressure | The dominant risk changes with maturity, issuer quality, and market regime. |

| Liquidity and risk appetite | Usually deeper and more resilient, but still vulnerable in stress | Usually more sensitive to liquidity withdrawal and risk-off behavior | Liquidity conditions can change the meaning of the same credit label. |

| False reading | Not the same as risk-free debt | Not the same as inevitable default | The label is an input, not a complete market conclusion. |

Rating boundary and default-risk compensation

Investment grade and high yield are rating-based credit categories. A common shorthand is that investment grade sits at or above the lower investment-grade threshold, while high yield sits below it. The exact symbols vary by rating-agency scale, so the useful point is the boundary itself: one side is classified as higher-quality credit, and the other side is classified as below investment grade.

That boundary matters because credit investors require compensation for the possibility that an issuer may fail to pay interest, repay principal, refinance debt, or maintain market access under pressure. High-yield credit usually carries a higher yield because the market demands more compensation for those risks.

Classification is not a forecast

A credit rating category summarizes relative credit quality. It does not forecast a precise default date, recession, equity-market direction, or trade outcome. A higher-rated issuer can still weaken, and a below-investment-grade issuer can still meet obligations if cash flow, refinancing access, and market conditions remain supportive.

Why high yield usually pays more

High-yield debt usually pays more because investors require a wider compensation margin. That compensation can reflect weaker balance sheets, less stable cash flows, higher leverage, shorter refinancing windows, lower liquidity, or greater sensitivity to risk appetite. The extra yield is the price of bearing more uncertainty.

The mistake is treating the higher yield as a simple reward. A higher coupon or yield can be offset by spread widening, downgrade risk, liquidity pressure, or default loss. For market-structure interpretation, the question is not only which category yields more. The better question is what risk the yield is compensating for.

Yield, spreads, and stress sensitivity

Yield describes the return compensation embedded in the debt price. A spread describes the extra yield over a reference rate or benchmark. Credit spreads are often more useful for market interpretation because they help separate risk compensation from the general level of interest rates.

Investment-grade spreads usually help interpret how higher-quality credit is being repriced relative to safer benchmarks. They can widen when liquidity deteriorates, when risk premiums rise, or when investors demand more compensation even from stronger issuers.

High-yield spreads often carry a stronger risk-appetite and default-risk component. When high-yield spreads widen sharply, the market may be demanding more compensation for refinancing pressure, expected downgrade risk, weaker liquidity, or rising concern about issuer stress.

Classification versus pricing signal

Investment grade and high yield are credit categories. Spreads are market-pricing expressions. The category tells the reader where the issuer sits in the credit-quality spectrum. The spread tells the reader how the market is currently pricing risk compensation around that category.

Rate risk versus credit risk

Investment-grade debt can be more sensitive to interest-rate and duration conditions, especially when maturity is longer and credit risk is not the main driver. If benchmark yields rise, an investment-grade bond can still lose value even when the issuer remains financially sound.

High-yield debt is often more sensitive to credit risk, refinancing risk, liquidity, and risk appetite. Its price can react strongly when investors become less willing to hold lower-quality credit, even if benchmark yields are not the only driver. In risk-off conditions, high-yield repricing can reflect both higher required compensation and weaker confidence in issuer resilience.

| Risk lens | Why it matters | Typical interpretation mistake |

|---|---|---|

| Interest-rate risk | Bond prices can fall when benchmark yields rise, especially when duration is longer. | Assuming higher-rated credit cannot lose value. |

| Credit risk | Issuer weakness can require higher compensation or reduce market access. | Assuming higher yield is only extra income. |

| Liquidity risk | Harder trading conditions can increase price gaps and spread pressure. | Assuming the quoted yield is easy to realize under stress. |

| Risk-appetite risk | Lower-quality credit can reprice quickly when investors reduce risk exposure. | Assuming the credit label alone explains the whole move. |

Same market stress, different interpretation

A credit-stress episode can affect both categories at the same time, but the interpretation is not identical. Investment-grade weakness may reflect spread widening, duration pressure, or broader risk-premium repricing while the issuer base remains comparatively stronger. High-yield weakness more often points to rising compensation for default risk, refinancing pressure, liquidity strain, or weaker risk appetite.

The same stress environment can therefore carry different information across the credit spectrum. Investment-grade repricing may show that investors want more compensation even from stronger issuers. High-yield repricing may show that the market is becoming less willing to finance lower-rated borrowers on easy terms.

The interpretation still needs confirmation. Widening spreads alone do not prove that a recession has started, that equities must fall, or that a timing decision is clear. The signal becomes more meaningful when it aligns with liquidity conditions, funding stress, market breadth, yield-curve behavior, and broader risk appetite.

Common false readings

- Investment grade does not mean risk-free. Higher-rated debt can still lose value because of rate moves, spread widening, downgrades, or issuer deterioration.

- High yield does not mean default is certain. Below-investment-grade credit carries higher compensation for risk, but many issuers can still service debt through supportive conditions.

- Yield alone is not enough. A higher yield may reflect higher expected compensation, but it may also reflect weaker liquidity, refinancing pressure, or deteriorating credit quality.

- Spread widening needs context. Credit spreads can widen because of default-risk concern, liquidity withdrawal, rate volatility, or broad risk-premium repricing.

- The comparison is not an allocation rule. The useful distinction is credit-market interpretation, not a direct instruction to prefer one category over the other.

Fallen angels and rising stars

The boundary between investment grade and high yield is not permanent. A fallen angel is an issuer that moves from investment grade into high yield after a downgrade. A rising star moves from high yield into investment grade after credit quality improves. These boundary changes can matter because some investors are restricted by rating category, and forced buying or selling can affect liquidity and spreads.

The broader point is that the rating label, the issuer’s fundamentals, and the market price do not always move at the same speed. A market can begin demanding more compensation before a formal downgrade appears. It can also price improvement before a formal upgrade is confirmed.

How to read the comparison in market context

The strongest reading comes from separating category, pricing, and confirmation. The category identifies credit quality. The yield and spread show compensation. The surrounding market context explains whether the move is mainly about rates, liquidity, credit stress, or risk appetite.

| Question | What to check | Why it matters |

|---|---|---|

| Is the move rating-category specific? | Compare higher-quality and lower-quality credit behavior. | Helps separate broad rate repricing from credit-quality stress. |

| Is the spread move broad or concentrated? | Check whether pressure is visible across categories or mainly in high yield. | Broad widening can signal general risk-premium repricing, while high-yield-led pressure can point more toward credit-cycle concern. |

| Is liquidity weakening? | Watch whether trading conditions and funding access appear more strained. | Liquidity stress can amplify spread moves even before default outcomes appear. |

| Are rates driving the move? | Separate benchmark-yield changes from credit-spread changes. | Investment-grade price weakness can come from duration pressure, not only issuer credit deterioration. |

| Is risk appetite changing? | Compare credit behavior with broader risk assets and market breadth. | High-yield stress often becomes more meaningful when it aligns with wider risk-off behavior. |

Related credit-market concepts

Investment-grade and high-yield categories become more useful when paired with spread behavior. The category explains the credit-quality bucket. The spread explains how the market is pricing compensation for risk inside that bucket.

- Use investment-grade spread behavior to understand risk compensation in higher-quality corporate credit.

- Use high-yield spread behavior to understand risk compensation in speculative-grade credit.

- Compare both only after separating rate pressure, credit risk, liquidity conditions, and broader risk appetite.

FAQ

Does investment grade mean risk-free?

No. Investment grade means the issuer is classified as higher credit quality than below-investment-grade issuers. It does not remove interest-rate risk, downgrade risk, liquidity risk, spread-widening risk, or issuer-specific deterioration.

Does high yield mean default is likely?

No. High yield means the issuer sits below the investment-grade boundary and usually requires higher compensation for risk. That does not mean default is certain. Default probability depends on issuer fundamentals, refinancing access, cash flow, maturity schedule, and market conditions.

Is high yield the same as junk bonds?

High yield and junk bonds usually refer to the same broad category: below-investment-grade debt. “High yield” describes the compensation side, while “junk” is an informal label for the lower credit-quality category.

Which is more sensitive to interest rates?

Investment-grade debt can be more sensitive to interest rates when duration is longer and credit stress is not dominant. High-yield debt can be more sensitive to credit risk and risk appetite. The answer depends on maturity, issuer quality, spread level, and market regime.

Can credit labels predict recessions or equity direction?

No. Credit labels are classification inputs. Spread behavior can provide useful risk-context information, but neither investment grade nor high yield alone predicts recession timing, equity direction, or a trade decision.