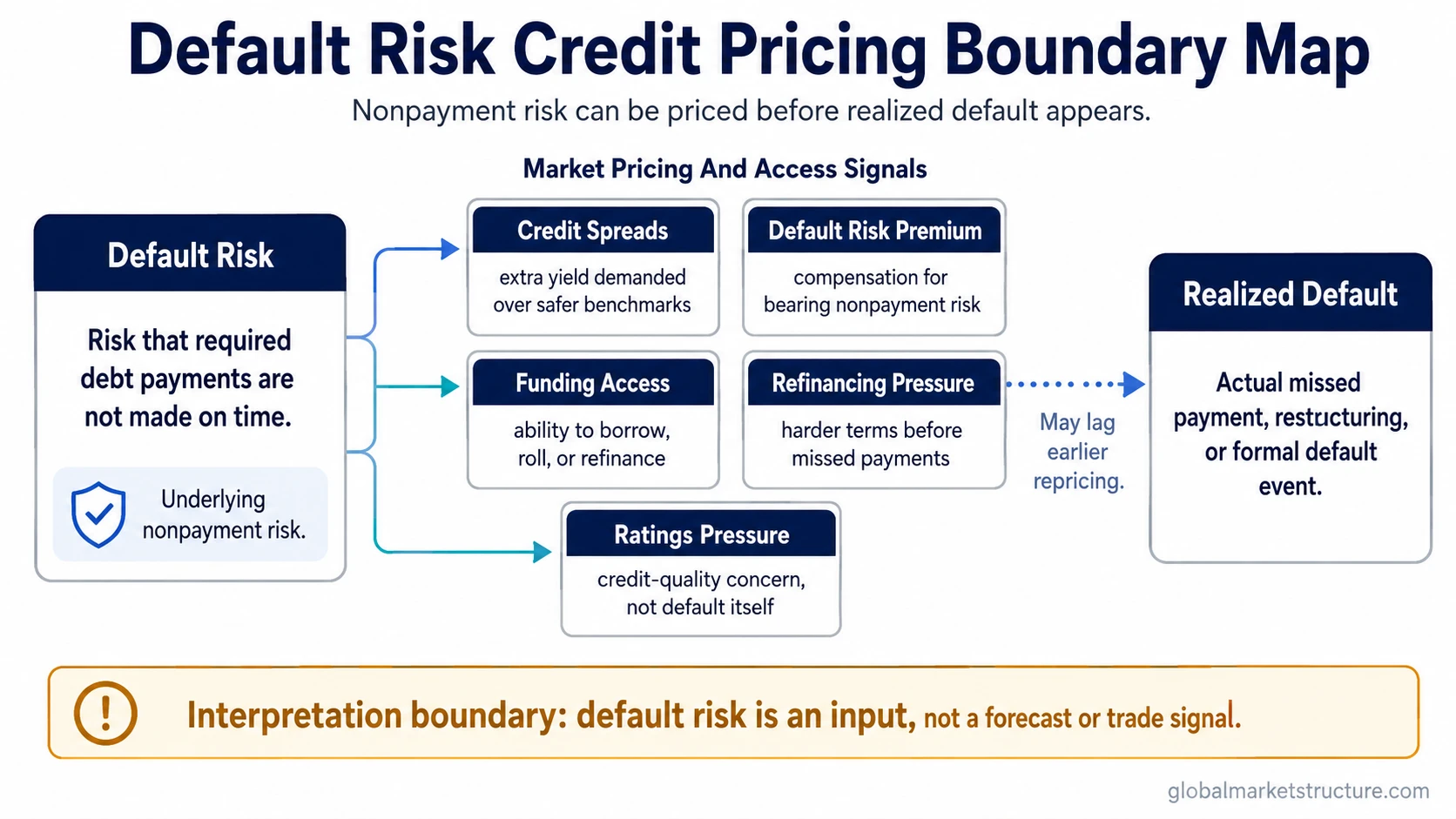

Default risk is the risk that a borrower, issuer, or obligor fails to make required debt payments, such as interest, principal, or another contractual payment.

For credit-market interpretation, default risk matters because markets can start repricing repayment risk before actual defaults appear. Spreads may widen, refinancing may become harder, ratings pressure may rise, and investors may demand more compensation for holding weaker credit exposure.

Default risk is not a standalone market forecast, recession call, or trading signal. It is one input in a broader credit and liquidity reading.

Default Risk Definition

Default risk means nonpayment risk. It refers to the possibility that a borrower or issuer does not meet required debt obligations on time and according to the agreed terms.

The obligation can involve interest, principal, coupon payments, loan payments, or other required debt-service commitments. The key issue is not whether the borrower looks weak in general, but whether payment capacity and willingness become uncertain enough for creditors to demand more compensation or restrict access to funding.

Why Default Risk Matters In Credit Markets

Credit markets are built around the pricing of repayment risk. When lenders or investors believe nonpayment risk is rising, they may demand higher yields, tighter terms, shorter maturities, more collateral, or greater protection against loss.

That repricing can appear before a default event is visible. A borrower may still be making payments while the market has already become less willing to refinance its debt at favorable terms.

This is why default risk belongs inside credit-market-signal interpretation. It helps explain why credit can become more expensive, why lower-quality borrowers can lose market access, and why stress can spread from individual credit concerns into broader funding conditions.

What Default Risk Is And Is Not

Default risk is narrower than many related credit terms. It is the underlying risk of missed or failed payment, not every market price, spread movement, or broad credit stress condition that may appear around it.

| Concept | Meaning | Boundary |

|---|---|---|

| Default risk | Risk that a borrower, issuer, or obligor fails to make required debt payments. | Underlying nonpayment risk. |

| Credit risk | Broader risk that credit quality deteriorates or payment terms are not met. | Wider category than default risk. |

| Credit spreads | Extra yield investors demand over safer benchmarks. | Market pricing expression, not the default itself. |

| Default risk premium | Compensation investors require for bearing default risk. | Pricing component, not the risk event. |

| Realized default | Actual missed payment, restructuring, or formal default event. | Outcome that can lag earlier market stress. |

| Credit crunch | Broad tightening in credit availability. | System condition, not the same as default risk. |

How Markets Can Price Default Risk

Markets do not wait only for actual missed payments. They can adjust when investors believe future payment capacity has weakened.

A basic credit-market sequence can look like this: repayment risk rises, credit assessment weakens, investors demand more compensation, spreads widen, refinancing becomes less favorable, and funding access can deteriorate if stress persists.

In that sequence, investment-grade spreads can help show how higher-quality credit is being priced relative to safer benchmarks. Wider spreads do not prove default is coming, but they can show that investors are demanding more compensation for credit exposure.

Ratings pressure can also matter. A downgrade risk or negative credit review can affect how investors classify the borrower, how much yield they require, and whether certain buyers are still allowed or willing to hold the debt.

Default Probability, Loss Severity, And Pricing

Default risk is often discussed through two related questions: how likely nonpayment is, and how severe the loss could be if nonpayment occurs.

A borrower with a higher probability of default may require greater compensation. A borrower with weak recovery value may also require greater compensation because investors may expect larger losses if default occurs.

Credit pricing can therefore reflect both probability and severity. The market may demand a higher yield because default seems more likely, because potential recovery looks weaker, or because liquidity conditions make investors less willing to hold risky credit.

Why Realized Defaults Can Lag Credit Stress

Realized defaults are often late-stage evidence. A borrower may face rising funding costs, reduced market access, covenant pressure, or refinancing difficulty before an actual default appears.

That timing gap matters for market interpretation. Credit stress can build while reported defaults still look contained. The absence of realized defaults does not always mean repayment risk is unchanged, and rising default risk does not guarantee that defaults are imminent.

A practical scenario is a borrower that still meets current payments but can no longer refinance maturing debt at acceptable terms. The market may price higher risk before any missed payment occurs because future funding access has become less certain.

The concern becomes more useful as a credit-market signal when refinancing pressure appears alongside wider spreads and weaker funding access, and less useful when the stress remains isolated to one borrower.

What Default Risk Does Not Tell You By Itself

Default risk does not produce a complete market view on its own. It should not be treated as a direct recession forecast, market-timing tool, or buy/sell signal.

The same rise in perceived default risk can have different meanings depending on the surrounding environment. It may reflect borrower-specific weakness, sector stress, tighter liquidity, higher refinancing costs, weaker collateral values, or broader risk aversion.

The interpretation becomes stronger when default-risk concerns align with other credit and liquidity signals, such as wider spreads, weaker funding access, reduced market depth, or broader tightening in credit availability.

Common Mistakes When Reading Default Risk

Mistake 1: Treating spread widening as proof of default. Wider spreads can reflect higher perceived credit risk, liquidity pressure, or investor risk aversion. They do not prove that a default will occur.

Mistake 2: Treating realized defaults as the first signal. Actual defaults may appear after markets have already repriced weaker credit conditions.

Mistake 3: Confusing default risk with a credit crunch. Default risk is about nonpayment risk. A credit crunch is a broader tightening of credit availability that can affect many borrowers at once.

Mistake 4: Turning default risk into a trading rule. Default-risk interpretation needs context from spreads, funding conditions, liquidity, ratings pressure, and broader market structure.

Related Credit-Market Signals

Default risk is one part of the credit-market signal set. Spread behavior helps show how markets price compensation for credit exposure, while credit availability helps show whether borrowers can still access funding.

Useful adjacent concepts include investment-grade spread behavior, credit crunch conditions, refinancing pressure, realized defaults, and default risk premium. These concepts should remain separate because each answers a different question about credit stress.

FAQ

What is default risk?

Default risk is the risk that a borrower, issuer, or obligor fails to make required debt payments, such as interest or principal.

Is default risk the same as credit risk?

No. Default risk is a narrower form of credit risk focused on nonpayment. Credit risk is broader and can include credit-quality deterioration, downgrade risk, spread repricing, and other credit-related losses.

Is default risk the same as credit spreads?

No. Default risk is the underlying risk of nonpayment. Credit spreads are one way markets may price credit risk through extra yield over safer benchmarks.

Does default risk predict a recession?

No. Rising default risk can be one warning input inside credit-market interpretation, but it does not predict recession by itself and should not be treated as a standalone forecast.