Carry and roll-down is a fixed-income and rates concept that combines carry from income, coupon, accrual, or financing effects with roll-down from an exposure moving along the yield curve as time passes. It is an assumption-based measure, not a guaranteed return or standalone forecast, because curve shifts, spread moves, funding costs, and holding constraints can change the result.

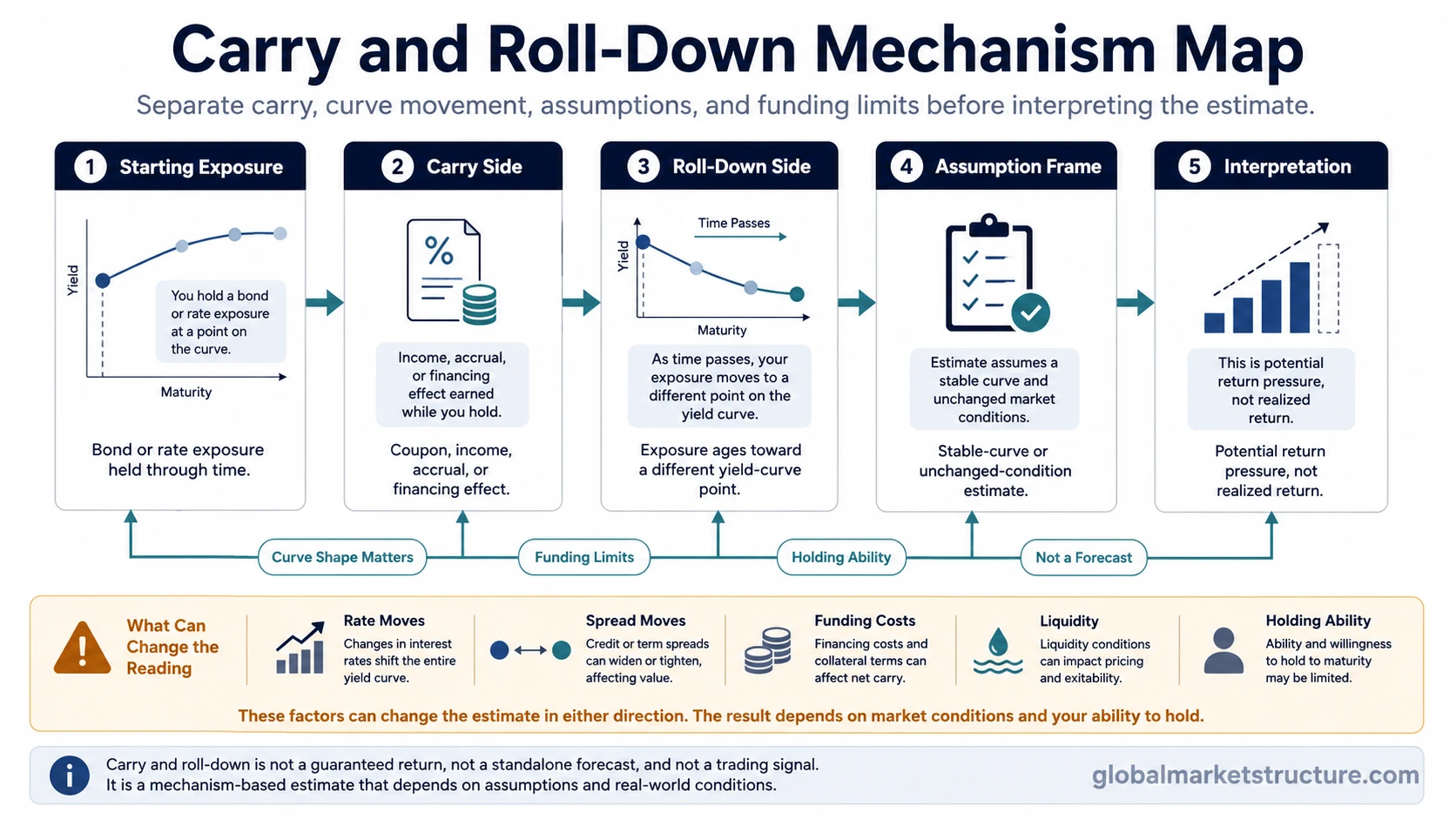

Core definition: Carry and roll-down estimates how much a fixed-income or rate exposure may benefit or suffer from two linked effects: the carry earned or paid while holding it, and the value effect created as the exposure ages toward a different point on the yield curve.

Main limitation: The estimate depends on assumptions. A favorable carry and roll-down profile can be offset if yields move against the position, credit spreads widen, financing costs rise, or the position cannot be held long enough for the expected effect to matter.

What Carry and Roll-Down Means

Carry and roll-down is most often used in fixed income, rates, and yield-curve analysis. It helps separate the return pressure that comes from holding an exposure from the return pressure that comes from the passage of time along a curve.

Carry is the income, accrual, coupon, or financing side of the position. Roll-down is the change in value that can occur when a bond or rate exposure moves toward a shorter maturity point on the yield curve. The combined measure is useful because many fixed-income positions are affected by both at the same time.

The concept is not the same as a realized return. It is usually read under a stable-curve or unchanged-condition assumption. That assumption is only a modeling frame. It does not mean the curve will stay unchanged.

Carry vs Roll-Down

Carry and roll-down becomes clearer when the two parts are separated first.

| Part | What it describes | What can change the reading |

|---|---|---|

| Carry | Income, coupon, accrual, or financing effect from holding the exposure. | Funding cost, repo cost, hedge cost, coupon level, and position structure. |

| Roll-down | Value effect from the exposure moving along the yield curve as time passes. | Curve shape, curve steepness, maturity point, and whether the curve shifts before the expected roll-down is realized. |

| Carry and roll-down | The combined assumption-based effect from holding the exposure and moving along the curve. | Rate moves, spread moves, funding pressure, margin pressure, and the ability to keep the position open. |

For a narrower curve-only discussion, bond roll-down focuses on the price and yield effect of a bond aging toward a shorter maturity point. Carry and roll-down is broader because it combines that curve effect with the income or financing side of the exposure.

How the Mechanism Works

The mechanism starts with time. As time passes, a fixed-income exposure becomes closer to maturity or moves toward a different point on the curve. If the yield curve is upward sloping, downward sloping, or unevenly shaped, that movement can change the value implied by the curve.

At the same time, the position may earn income or pay financing. A bond may earn coupon income. A rate exposure may have accrual or funding effects. A hedged or financed position may depend on the cost of carrying the exposure.

The combined estimate isolates one holding-period path: income or funding effects plus the curve movement expected as time passes. That makes carry and roll-down useful for scenario comparison, but weak as a standalone forecast.

The Assumption Stack

Time passes: the exposure ages or moves toward a shorter maturity point.

Income or funding accrues: carry is earned, paid, or reduced by financing and hedging costs.

The curve shape matters: roll-down depends on where the exposure sits on the yield curve and where it is expected to move.

The curve may shift: the stable-curve assumption can fail if rates move, the curve steepens, flattens, or reprices abruptly.

The position must be holdable: margin, financing, liquidity, and risk limits can affect whether the expected carry and roll-down can be realized.

What Drives the Carry and Roll-Down Estimate

| Component | What it measures | Main assumption | Interpretation risk |

|---|---|---|---|

| Carry | Income, coupon, accrual, or financing effect during the holding period. | The stated income or financing conditions remain close enough to the estimate. | Rising financing costs can reduce or reverse the apparent benefit. |

| Roll-down | Value effect from moving along the curve as maturity shortens. | The curve shape remains stable enough for the roll-down estimate to matter. | A curve shift can overwhelm the expected roll-down effect. |

| Spread behavior | Change in credit, liquidity, or instrument-specific spread over the holding period. | Spreads do not move sharply against the exposure. | Spread widening can dominate both carry and curve roll-down. |

| Funding condition | Ability to finance, hedge, margin, and hold the exposure. | Funding remains available on workable terms. | Funding stress can force adjustment before the expected effect plays out. |

Bond and Swap Context

In bond analysis, carry and roll-down often connects coupon income with the price effect of moving along the yield curve. A bond that ages from one maturity point toward another can look more attractive if the curve shape creates favorable roll-down and the income side is positive.

In swaps and other rate exposures, the same broad idea can appear through accrual, forward rates, curve shape, and the expected movement of the exposure through time. The exact formulas can differ by instrument, but the interpretation problem stays similar: carry and roll-down is conditional on the curve, funding, and position assumptions.

The concept should therefore be read as a decomposition tool rather than a complete return model. It helps explain one part of the expected holding-period pressure, not every risk that can affect the position.

Observed Input vs Interpretation

A cleaner reading separates what can be observed or estimated from what is being inferred.

| Layer | Examples | How to read it |

|---|---|---|

| Observed or estimated input | Yield curve shape, maturity point, coupon, accrual, financing cost, spread level. | These inputs describe the starting condition for the carry and roll-down estimate. |

| Interpretation | Potential return cushion, holding pressure, or relative attractiveness under stated assumptions. | This is a conditional reading, not proof that the exposure will perform well. |

| Limitation | Rate shocks, curve shifts, spread widening, funding pressure, margin calls, or liquidity constraints. | These can overwhelm the estimate or prevent the position from being held long enough. |

Why It Matters for Market-Structure Interpretation

Carry and roll-down matters because it can influence how fixed-income and rates participants compare exposures across maturities, curves, and funding conditions. When many participants prefer positions with favorable carry and roll-down, positioning can become sensitive to rate-path assumptions and financing conditions.

That does not make the measure a signal by itself. It is more useful as context for how certain positions may be supported under stable conditions and how that support can weaken when the rate path, curve shape, or funding backdrop changes.

The broader carry trade context can include currencies, funding spreads, volatility, and cross-asset carry structures. Carry and roll-down is narrower than that broader carry universe because it focuses on fixed-income or rates exposure moving through time along a curve.

Why Positive Carry and Roll-Down Can Mislead

Positive carry and roll-down is not a guaranteed profit. It can show that the starting assumptions look favorable, but it does not remove mark-to-market risk, spread risk, funding risk, or liquidity risk.

A stable-curve assumption is not a prediction. It is a way to isolate one part of the return pressure. If the curve reprices sharply, the realized result can look very different from the estimate.

Holding ability matters. A position with attractive projected carry and roll-down can still become difficult to hold if financing terms deteriorate, margin needs rise, or liquidity disappears.

A common mistake is to read favorable carry and roll-down as if the position is already protected. The stronger interpretation is more conditional: the measure can show a potential cushion under certain assumptions, while the surrounding market structure decides how durable that cushion may be.

Illustrative Scenario

A five-year fixed-income exposure may show positive carry and favorable roll-down if the curve shape implies a lower yield point as the exposure ages. That means the income or financing side and the expected movement along the curve appear supportive at the start of the holding period.

The reading changes if yields move higher before enough time passes, if spreads widen, or if financing costs rise. In that case, the original estimate still described the starting assumptions, but the market environment changed the realized path.

Carry and Roll-Down vs Nearby Concepts

| Concept | Main focus | Boundary |

|---|---|---|

| Carry and roll-down | Combined carry, curve movement, and position assumptions. | Combines the income, curve-movement, and position-assumption layers in one fixed-income or rates reading. |

| Bond roll-down | Price and yield effect of a bond aging along the curve. | Narrower than the combined carry and roll-down measure. |

| Fixed-income carry | Income or holding-return side of fixed-income exposure. | Does not fully capture curve movement or roll-down by itself. |

| Carry trade | Broader carry positioning across funding, currencies, rates, volatility, or assets. | Wider than fixed-income carry and roll-down. |

| Funding stress | Pressure on financing, margin, liquidity, and ability to hold exposure. | Explains why attractive carry structures can unwind or become unstable. |

FAQ

Does positive carry and roll-down guarantee profit?

No. Positive carry and roll-down means the starting assumptions may look favorable, but realized performance can still be hurt by rate moves, spread moves, higher funding costs, liquidity pressure, or an inability to hold the exposure.

Is carry and roll-down the same as bond roll-down?

No. Bond roll-down is narrower and focuses on the value effect of a bond moving along the yield curve as it ages. Carry and roll-down is broader because it combines the roll-down effect with income, financing, and position-specific assumptions.