Bond roll-down is a fixed-income yield-curve effect where a bond can gain price support as it ages into a shorter maturity point on the curve, if the curve shape and yield conditions remain favorable. It is conditional, not guaranteed, and it does not forecast future interest rates or realized bond returns.

Definition: Bond roll-down refers to the expected price or return component that can arise when a bond’s remaining maturity shortens and the bond is compared with a different point on the yield curve.

Key Points

- Bond roll-down is a yield-curve and maturity-aging effect, not coupon income.

- The simplest positive case usually depends on a stable, upward-sloping curve.

- Expected roll-down is different from realized return because rates, spreads, costs, liquidity, duration, and convexity can change the outcome.

- Roll-down can help interpret fixed-income positioning, but it is not a standalone market signal.

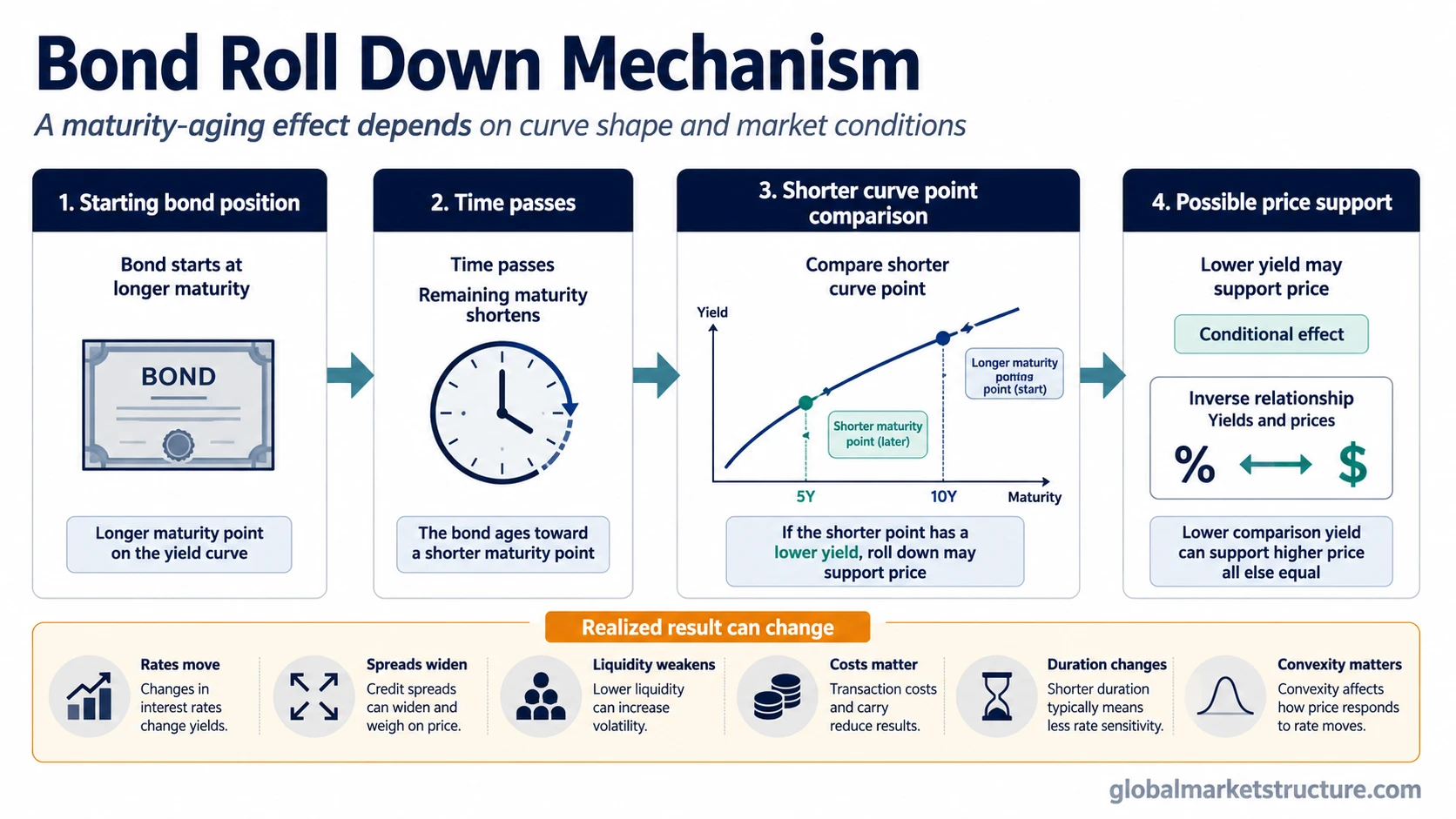

What Bond Roll Down Means

Bond roll-down describes how the value of a bond may change as time passes and the bond moves closer to maturity. If the yield curve is upward sloping, a bond that originally sat at a longer maturity point may later be valued closer to a shorter maturity point with a lower yield. Because bond prices and yields move inversely, that lower comparison yield can create a positive price effect.

The important condition is that the curve does not move against the position. A bond can have expected roll-down at the start of a holding period and still produce a weaker realized result if the overall yield curve shifts higher, credit spreads widen, liquidity deteriorates, or transaction costs absorb the expected effect.

What Bond Roll Down Is and Is Not

The cleanest way to understand bond roll-down is to separate the maturity-aging effect from nearby concepts that can be confused with it.

| Concept | Correct interpretation | Why the distinction matters |

|---|---|---|

| Bond roll-down | A conditional price or return component from moving along the yield curve as maturity shortens. | It depends on curve shape, yield movement, spreads, costs, and holding-period behavior. |

| Coupon income | Cash interest paid by the bond according to its coupon terms. | Coupon income can exist even when roll-down is weak or negative. |

| Fixed-income carry | The income or accrual component associated with holding a fixed-income position. | Carry and roll-down can interact, but they are not the same return component. |

| Rate forecast | A view about where yields may move in the future. | Roll-down uses a curve assumption. It does not predict the future path of yields. |

| Guaranteed capital gain | A certain increase in bond price. | Roll-down can be offset or reversed by market changes. |

| Full bond strategy | A complete decision process for selecting, sizing, and managing bonds. | Bond roll-down is one mechanism inside fixed-income analysis, not a complete allocation process. |

How Bond Roll Down Works

The mechanism starts with the relationship between maturity and the yield curve. A bond does not stay at the same maturity point forever. As time passes, its remaining maturity shortens, and the market may compare it with a different part of the curve.

Mechanism sequence:

- A bond begins with a given remaining maturity, such as several years.

- Time passes, so the bond has a shorter remaining maturity.

- The bond is increasingly compared with the yield available at that shorter maturity point.

- If the shorter maturity point has a lower yield, the bond may receive price support.

- If the curve shifts, spreads widen, liquidity worsens, or costs matter, realized return can differ from the expected roll-down effect.

The mechanism is easiest to see on an upward-sloping curve. Longer-maturity yields are higher than shorter-maturity yields, so a bond aging toward the shorter point may be associated with a lower yield comparison. The inverse price-yield relationship is what turns that lower yield comparison into possible price support.

Bond Roll Down vs Fixed-Income Carry

Bond roll-down and carry are related, but they answer different questions. Roll-down asks how a bond may be affected by moving along the yield curve as maturity shortens. Fixed-income carry focuses on the income or accrual side of holding a fixed-income position.

A bond can have positive carry and weak roll-down. It can also have expected roll-down that is overwhelmed by rising yields, wider credit spreads, or poor liquidity. Separating the two helps prevent a common mistake: treating one expected return component as if it described the full holding-period result.

Why the Yield Curve Shape Matters

The yield curve shape controls whether roll-down is likely to be a tailwind, a small factor, or a possible headwind. The starting curve matters, but the path of the curve during the holding period matters as well.

| Curve condition | Roll-down implication | Main limitation |

|---|---|---|

| Upward-sloping curve | Often the clearest positive expected roll-down setup, because shorter maturity yields may be lower. | The benefit can disappear if the curve shifts higher or spreads widen. |

| Flat curve | Expected roll-down may be small because nearby maturity points have similar yields. | Small yield differences can be absorbed by costs or ordinary yield movement. |

| Inverted curve | Roll-down can be weak or negative if the bond ages toward a higher-yielding shorter point. | The curve may normalize or shift in ways that change the expected effect. |

| Flattening or shifting curve | The original roll-down estimate can become unreliable. | Realized return depends on the new curve, not only the starting curve. |

When Bond Roll Down Can Fail

Expected roll-down is not the same as realized return. The expected component can be useful, but it sits inside a larger rate, spread, liquidity, and cost environment.

Main failure modes:

- Curve flattening: the shorter maturity point no longer offers the lower yield assumed at the start.

- Curve inversion: the bond may age toward a higher-yielding point instead of a lower-yielding point.

- Parallel yield rise: the whole curve can move higher, reducing or overwhelming the roll-down effect.

- Spread widening: credit or risk spreads can widen even if the government yield curve behaves favorably.

- Liquidity friction: poor market depth can reduce the practical value of the expected effect.

- Trading costs: bid-ask spreads, execution costs, and rebalancing costs can absorb small expected gains.

- Duration and convexity: price sensitivity can change as yields move and as the bond approaches maturity.

- Policy surprises: central-bank repricing can shift the curve faster than the original assumption allowed.

Simple Bond Roll Down Scenario

A bond has several years left to maturity, and the yield curve is upward sloping. As time passes, the bond moves closer to a shorter maturity point where the market yield is lower than the original longer-maturity yield. If the curve remains broadly stable, that lower comparison yield can support the bond’s price.

Scenario reading: The expected roll-down effect is only one part of the outcome. If yields rise across the curve during the holding period, or if credit spreads widen, the realized return can be lower than the initial roll-down estimate. If liquidity is poor or transaction costs are large, the practical result can also differ from the clean curve example.

The useful distinction is between the clean curve effect and the full holding-period result. Bond roll-down can be a useful fixed-income concept, but it becomes misleading when treated as a guaranteed price effect.

How to Estimate Bond Roll Down Conceptually

A simple roll-down estimate usually compares the bond’s current value with the value implied by a shorter maturity point after time passes, while making explicit assumptions about the curve, spreads, costs, and holding period. The exact calculation can vary by bond type, pricing model, yield convention, coupon structure, and holding period.

The safer takeaway is that roll-down is a curve-based expected return component. A precise calculation should define the bond cash flows, the starting curve, the future maturity point, the assumed curve path, spread assumptions, and costs.

How Bond Roll Down Fits Carry and Roll-Down Analysis

Roll-down becomes more useful when it is evaluated beside carry rather than in isolation. Carry and roll-down analysis separates income or accrual effects from maturity movement along the curve, then compares both with the risks that can change the realized result.

For market-structure interpretation, bond roll-down can help explain why fixed-income positioning may favor certain maturity areas under specific curve conditions. The concept remains conditional. Rate-path expectations, curve shape, credit spreads, liquidity, and transaction costs still decide whether the expected component survives in practice.

FAQ

Is bond roll-down guaranteed?

No. Bond roll-down is conditional. It depends on curve shape, curve stability, rate movement, spread behavior, liquidity, costs, duration, convexity, and the holding period.

Is bond roll-down the same as carry?

No. Carry usually refers to income or accrual from holding a fixed-income position. Bond roll-down refers to the possible price or return effect from moving along the yield curve as maturity shortens.

Does bond roll-down require an upward-sloping yield curve?

An upward-sloping curve is the clearest positive expected case, but the realized result still depends on how the curve, spreads, liquidity, and costs change during the holding period.

Is there a bond roll-down formula?

A roll-down estimate usually compares the bond’s current value with the value implied by the shorter maturity point after time passes, under stated curve and spread assumptions. The exact formula depends on the pricing method and bond structure.