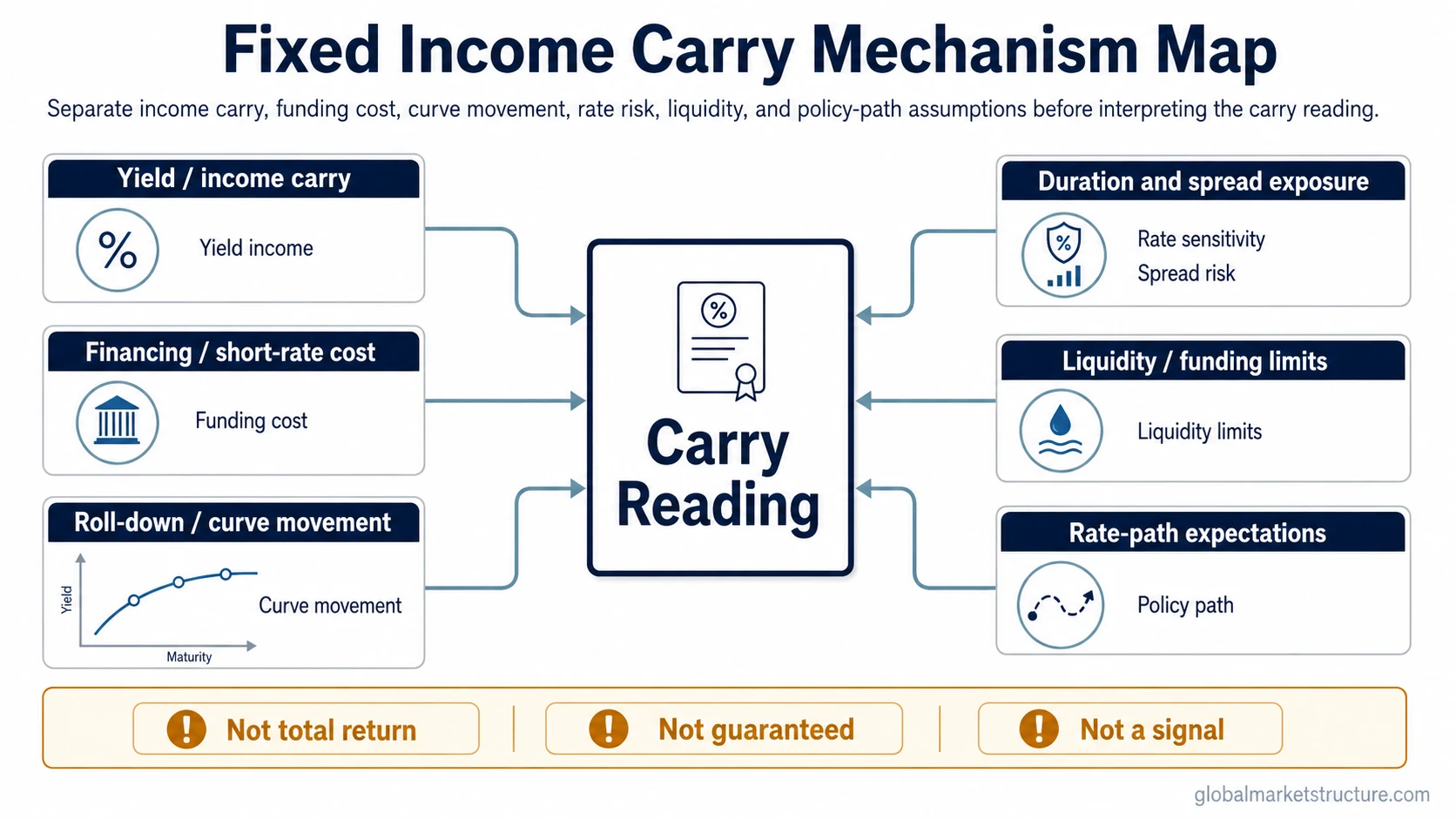

Fixed income carry is the income or expected-return component from holding a bond or fixed-income exposure before market-price changes are counted. It is shaped by yield, financing cost, curve movement, duration, and rate expectations, but it is not the same as total return, guaranteed return, or a standalone forecast.

Definition: Fixed income carry is the holding-period income component of a fixed-income position, usually assessed before the market value of the bond, swap, or rate exposure changes. It helps separate the income side of the position from the price effects created by yield changes, spread changes, liquidity conditions, and funding costs.

The core idea is simple: a fixed-income exposure may earn income or receive a fixed-rate leg, but that income is only one part of the full market result. A rate move, curve shift, spread widening, or funding squeeze can offset the carry component and change the interpretation.

Key Points

- Fixed income carry is one component of holding a bond, swap, or rate exposure, not the full return.

- Yield, coupon income, financing cost, and short-rate cost usually form the starting point.

- Roll-down is related because curve shape and maturity movement can affect the carry reading, but it is not identical to carry.

- Rate moves, spread changes, funding pressure, and liquidity conditions can overwhelm positive carry.

- Carry is market-structure evidence, not a guarantee, forecast, or instruction.

What Fixed Income Carry Includes

Fixed income carry usually begins with the income earned from holding the exposure. For a bond, that may include coupon or yield-based income. For a swap or rate exposure, the carry reading may involve the difference between fixed-rate receipt, floating-rate cost, and financing assumptions.

The cost side matters because carry is not only about income received. If financing costs rise, short rates reprice, or margin requirements become more expensive, the same exposure can have a weaker carry profile than the headline yield suggests.

Curve shape can also matter. When a bond moves along the yield curve over time, part of the expected holding-period economics may come from bond roll-down. That curve effect should be separated from the income component so the reading does not confuse yield carry with maturity movement.

Boundary: Fixed income carry describes a component of the expected holding economics. Total return also includes market-price change, yield movement, spread movement, currency effects where relevant, transaction costs, and liquidity conditions.

Carry, Roll-Down, and Total Return Are Different

Fixed income carry, roll-down, and total return are often discussed together because they all affect holding-period interpretation. They answer different questions.

| Concept | What it focuses on | Why the distinction matters |

|---|---|---|

| Fixed income carry | Income or expected-return component from holding fixed-income exposure | It isolates the income side before market-price changes are fully counted. |

| Roll-down | Effect of a bond moving along the yield curve as time passes | It depends on curve shape and can change if the curve steepens, flattens, or inverts. |

| Total return | Full realized result from income plus price movement and other effects | It can be positive or negative even when the carry component looks favorable. |

| Duration exposure | Price sensitivity to yield changes | A large rate move can dominate the carry component. |

| Credit spread exposure | Sensitivity to changes in compensation for credit risk | Spread widening can offset income and weaken the carry reading. |

| Funding cost | Cost of financing or floating-rate funding leg | Rising funding cost can reduce or reverse the carry advantage. |

The useful distinction is that carry starts the decomposition, while total return finishes it. Carry can be positive and still fail to protect the position from adverse rate, spread, liquidity, or funding changes.

How Fixed Income Carry Is Interpreted

A clean carry reading separates the income source from the conditions that can change it. The same headline yield can mean different things depending on financing cost, curve shape, duration exposure, credit spread risk, and liquidity depth.

| Component | What it captures | What can change the interpretation |

|---|---|---|

| Yield / income carry | Income expected from holding the fixed-income exposure | Yield changes, spread moves, default risk, and liquidity risk |

| Financing / short-rate cost | Cost of funding the exposure or paying a floating-rate leg | Policy-rate repricing, funding pressure, margin cost, and collateral constraints |

| Roll-down | Potential effect of moving along the yield curve over the holding period | Curve steepening, flattening, inversion, and changes in the expected holding period |

| Duration exposure | Price sensitivity to changes in yields | Large rate moves can dominate the income component |

| Credit and liquidity conditions | Compensation for credit risk and the ability to trade without major price impact | Spread widening, weaker market depth, forced selling, or more constrained market intermediation |

| Rate-path expectations | Whether the carry assumption remains consistent with the expected policy and yield path | Policy repricing, inflation surprises, growth surprises, or a change in central-bank reaction expectations |

When Fixed Income Carry Can Mislead

Carry can look attractive when income exceeds the immediate funding cost. That reading becomes incomplete if the market reprices the rate path, if credit spreads widen, or if financing terms become harder to maintain.

Limitation: Positive fixed income carry does not remove exposure to rate movement, spread movement, liquidity deterioration, currency effects where relevant, or funding pressure. It only describes one part of the holding-period economics.

The interpretation also depends on why carry exists. Higher yield may reflect income, but it may also reflect higher credit risk, lower liquidity, inflation uncertainty, or a larger duration burden. A carry reading is stronger when the income component, funding cost, curve shape, and risk conditions are separated instead of treated as one number.

Rate-path expectations are especially important. If the carry assumption depends on stable or declining funding costs, a policy repricing can change the economics quickly. If the carry assumption depends on a stable curve, a curve shift can weaken the original reading even when the income component remains visible.

Fixed Income Carry in a Market-Structure Scenario

A bond or swap exposure may show positive carry when income or fixed-rate receipt is above the financing or floating-rate cost. The reading can still weaken if yields move against the exposure, if funding costs rise, if liquidity deteriorates, or if credit spreads widen enough to offset the income component.

In that scenario, carry is useful because it identifies the income side of the exposure. It is not enough to complete the market-structure reading. The next step is to compare the carry component with duration sensitivity, curve behavior, credit conditions, funding cost, and the policy path implied by the rates market.

The same positive carry can therefore mean different things in different regimes. In a calm funding environment with stable spreads, it may be easier to interpret as income support. In a tightening or stress environment, the same carry can be offset by higher financing cost, weaker liquidity, or faster repricing in yields.

Fixed Income Carry and Related Carry Concepts

Fixed income carry belongs inside the broader family of carry, basis, and funding concepts, but it should not be collapsed into every carry structure. A cash-and-carry trade links a spot or cash exposure with a related futures or derivative position, so the mechanics are different from the income and financing decomposition used in fixed income carry.

Bond roll-down is the closest neighbor because curve shape and maturity movement can affect fixed-income holding economics. The distinction matters because a roll-down gain can disappear if the curve changes, while the carry component can also change if financing cost, credit spread, liquidity, or policy expectations shift.

For market-structure interpretation, the carry component is most useful when it is read beside funding cost, curve behavior, rate sensitivity, credit conditions, and liquidity depth.

FAQ

What is fixed income carry?

Fixed income carry is the income or expected-return component from holding a bond, swap, or other fixed-income exposure before market-price changes are fully counted.

Is fixed income carry the same as total return?

No. Total return includes income plus price changes and other effects. Carry is only one component, and it can be offset by rate moves, spread changes, liquidity pressure, or funding costs.

How is fixed income carry different from roll-down?

Carry focuses on the income and financing side of the exposure. Roll-down focuses on the effect of moving along the yield curve as time passes. The two can interact, but they are not the same concept.

Can positive carry still lead to a weak result?

Yes. Positive carry can be outweighed by adverse yield moves, spread widening, higher funding costs, weaker liquidity, or a policy path that changes the original carry assumption.